As a rule of thumb, your ideal asset allocation tends to shift from aggressive (heavy on stocks) to conservative (heavy on bonds) as you move through life. For instance, a 25-year-old might be perfectly comfortable with a 90% stock and 10% bond portfolio. But fast forward to age 65, and that mix might look more like 40% stocks and 60% bonds to safeguard what they've built.

The whole point is to make sure your investment risk lines up with your time horizon.

Matching Your Investments to Your Life's Timeline

Think of your investment portfolio like a ship setting off on a long voyage. When you're young, with the destination far off in the distance, you can afford to build a faster, more aggressive vessel. This ship is designed to chase high growth, weathering the inevitable storms of market volatility because it has plenty of time to get back on course. The goal is to maximize your returns when you have decades to recover from any market downturns.

But as you get closer to retirement, your mission changes entirely. It’s no longer about speed; it's about arriving safely in the harbor with all your cargo intact. This is where capital preservation takes over, and your ship needs to be reconfigured to be steadier and more defensive.

Why Time Horizon Is Your Greatest Asset

The core idea behind age-based asset allocation isn’t about trying to time the market—that’s a fool’s errand. It’s about matching your portfolio's risk profile with the amount of time you have left to invest. This strategy hinges on one simple truth: the more time you have, the more risk you can comfortably take on.

- Growth Engines: Think of stocks (equities) as the powerful engines of your portfolio. They have the highest potential for long-term growth.

- Portfolio Stabilizers: Bonds (fixed income) are like the ballast in the ship's hull. They provide stability and predictable income to keep things steady during rough seas.

Getting the balance right between these two asset classes is the key to building a portfolio that serves you well at every stage of life. Of course, this is just one piece of the puzzle. To really build a resilient portfolio, check out our guide on /blog/how-to-diversify-investment-portfolio/.

The best asset allocation is the one that gives you the highest probability of hitting your financial goals. It's about finding that sweet spot where you aren't taking crazy risks when you can't afford to, but you also aren't being too conservative when you have decades of growth still ahead of you.

Ultimately, a recommended asset allocation based on age is a roadmap, not a rigid set of rules you have to follow blindly. Life is complicated, and knowing when and how to adjust your investments is crucial. It often helps to get expert advice on portfolio distribution and fund selection to make sure your financial plan is truly built for your own unique journey.

The Investor's Lifelong Balance of Risk and Reward

When it comes to investing, time is the most powerful asset you'll ever have. Period. When you're young, with decades stretching out in front of you, you can afford to play offense. Your portfolio can be built for speed—heavy on growth assets like stocks—because you have plenty of time to recover from the market’s inevitable punches. That long runway is what lets the magic of compounding really work its wonders.

Think about it this way: Sarah starts investing at 25, while Tom holds off until he's 40. Even if they sock away the same amount each year, Sarah has a massive 15-year head start. For her, a market dip in her 30s is just a temporary setback, maybe even a buying opportunity. For Tom, that same dip in his 50s is a code-red, sweat-inducing event.

Shifting from Aggression to Preservation

But as retirement looms on the horizon, the game completely changes. The high-risk, high-reward strategy that built your wealth can suddenly become your biggest liability. With only a few years until you need to start living off that nest egg, a major market crash could be catastrophic. There’s just not enough time left on the clock to wait for a recovery.

This is when you have to make the crucial pivot from offense to defense. Your focus shifts from aggressive growth to capital preservation. You're no longer trying to hit home runs; you’re protecting the lead you’ve spent a lifetime building. This is where more stable, reliable assets like bonds step up to the plate.

There's an old rule of thumb that gives a simple framework for this transition. A classic guideline suggests the percentage of stocks in your portfolio should be 100 minus your age. It’s a straightforward way to visualize a gradual shift out of equities and into bonds over time. Following this logic, a 30-year-old might keep 70% in stocks, while a 60-year-old would dial that back to around 40%. For a deeper dive into how this plays out for larger portfolios, you can check out more insights on asset allocation for high-net-worth individuals.

Why This Evolution Is Necessary

Pivoting your strategy isn't about getting scared—it's about getting smart. It's a natural and absolutely essential part of any successful long-term investment plan.

Your financial needs and risk tolerance simply aren't the same throughout your life. It makes sense that your portfolio reflects that.

- Young Investors (20s-30s): The goal is maximizing long-term returns. Market volatility isn’t a threat; it’s a chance to scoop up assets on sale.

- Mid-Career Investors (40s-50s): Time to start balancing that growth with a little more protection. You're gradually taking some chips off the table.

- Pre-Retirees (60s+): The number one priority is protecting your principal and generating a stable income stream.

The point isn't just to accumulate wealth. It's to make damn sure that wealth is there for you when you actually need it. Adjusting your asset allocation as you age ensures your portfolio evolves with you, protecting you from a devastating loss at the worst possible time.

This lifelong rebalancing act is the bedrock of turning years of market participation into lasting financial security.

Building Your Growth Engine in Your 20s and 30s

If you're in your 20s and 30s, your investing mission is pretty straightforward: go for growth. Hard. During these early career years, your single greatest asset isn't money—it's time.

With decades of compounding ahead of you, your portfolio can—and should—prioritize building a powerful wealth-creation engine. That means putting the pedal to the metal with a high allocation to stocks.

The classic recommendation for this stage of life is a portfolio with anywhere from 80% to 95% in equities. That aggressive stance is designed to squeeze every bit of potential return out of the market while your career earnings and investment timeline are at their peak. A market downturn might feel scary, but for you, it's just a chance to scoop up assets on sale, knowing you have plenty of time to recover.

Crafting a Growth-Focused Portfolio

So what does an "aggressive growth" portfolio actually look like? It's not about YOLO-ing into a handful of speculative stocks. It's about building a diversified foundation.

A typical setup for this age bracket is built around a core of broad-market index funds, giving you a piece of hundreds or thousands of companies all at once. From there, you can add other growth-oriented assets.

- U.S. Market Index Funds: This is your bedrock. Think funds that track the S&P 500 or the total U.S. stock market. They give you a slice of the American economy.

- International Stocks: You don't want all your eggs in one country's basket. Adding funds that cover developed and emerging markets outside the U.S. is a crucial diversification move. It spreads your risk across different economies.

- Growth-Focused Equities: This is where you can be a bit more targeted. You might put a smaller slice of your portfolio into individual stocks you believe in or sector-specific funds (like technology) that have higher growth potential—just remember they come with higher risk, too.

Let's look at how this might break down for a few different investor profiles.

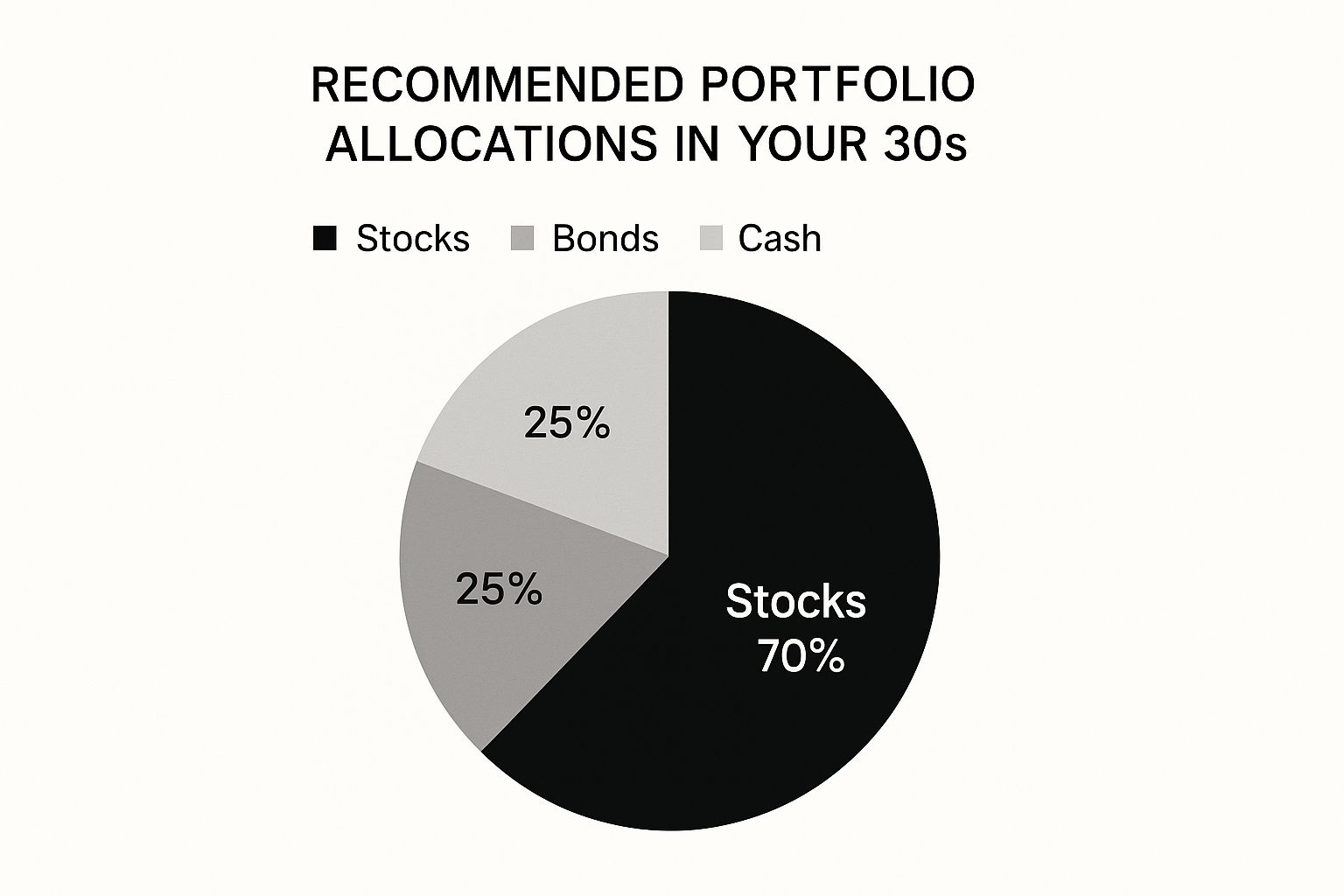

Sample Asset Allocation for Ages 20-39

The table below illustrates some typical portfolio breakdowns for investors in their early career stages. Notice how all three prioritize long-term growth by keeping stock allocations high.

| Investor Profile | Stocks (Equities) % | Bonds (Fixed Income) % | Cash/Alternatives % | Primary Goal |

|---|---|---|---|---|

| Aggressive Growth | 90% | 5% | 5% | Maximize capital appreciation |

| Growth | 80% | 15% | 5% | Strong growth with a small buffer |

| Moderate Growth | 70% | 25% | 5% | Substantial growth with more stability |

As you can see, even the more "moderate" approach for this age is still heavily weighted toward stocks. The small allocation to bonds and cash is there to provide a little stability without putting a major damper on your growth potential.

The infographic below paints a similar picture, showing a portfolio dominated by stocks.

Mastering the Psychology of Volatility

Committing to a portfolio that's nearly all stock means you have to get comfortable with volatility. Watching your account balance swing up and down can be tough on the nerves, but it's just part of the game. The real trick is learning to use those market dips to your advantage.

For a young investor, market volatility isn't the enemy; it's the price of admission for higher long-term returns. The biggest risk isn't a market crash, but rather the risk of being too conservative and letting inflation erode your future.

One of the most powerful ways to manage this is through dollar-cost averaging. It sounds complicated, but it's simple: you invest a fixed amount of money on a regular schedule, no matter what the market is doing.

When prices are high, your fixed amount buys fewer shares. But when prices drop? Your money automatically buys more shares.

This disciplined approach takes the emotion out of investing and turns market downturns from a crisis into an opportunity. By consistently buying in, you systematically lower your average cost per share over time and build a rock-solid foundation for the decades to come. It's the key to keeping your growth engine running at full throttle.

Balancing Growth and Protection in Your 40s and 50s

Once you hit your 40s and 50s, the game changes. These are usually your peak earning years, and retirement stops being some far-off, fuzzy idea. It’s a real destination you can see on the horizon. The goal shifts from pure, pedal-to-the-metal growth to a much more deliberate balance—growing your wealth while actively protecting what you've worked so hard to build.

This is the time to start gradually taking some risk off the table. That doesn't mean you ditch stocks entirely, but you do start beefing up your allocation to less volatile assets, like bonds. The idea is to smooth out the ride, making sure a sudden market correction doesn't derail years of disciplined saving. A portfolio that might have been 90% stocks in your 20s is probably better suited to a 60-70% stock allocation now.

This moderate strategy keeps your portfolio moving forward, still aiming to beat inflation. The bigger bond allocation, however, acts like a shock absorber. To really get a feel for how those market swings can rattle your accounts, check out our guide on what is market volatility. This is crucial stuff to understand as you start to prioritize protecting your capital.

The Growing Importance of Bonds

In your 40s and 50s, bonds go from being a minor player in your portfolio to a critical, stabilizing force. They provide a much-needed counterbalance to the gut-wrenching ups and downs of the stock market.

- Income Generation: A lot of bonds pay out regular interest (called coupon payments), which creates a predictable income stream. That predictability becomes incredibly valuable the closer you get to retirement.

- Lower Volatility: Bonds have historically been way less volatile than stocks. When the stock market tanks, high-quality bonds often hold their ground or even go up in value, cushioning the blow to your overall portfolio.

- Diversification: Because bonds and stocks often move in opposite directions, they give you true diversification. This is key to lowering your portfolio's overall risk.

This pivot toward fixed income is a classic move for investors in this age bracket. Data shows that investors with a 10-year horizon often land around a 60% stock, 35% bond, and 5% cash mix to find that sweet spot between growth and risk.

The goal in your 40s and 50s is simple: have a portfolio that can still grow but won’t give you a heart attack. You’re transitioning from building the engine to reinforcing the chassis for the final leg of your journey.

Rebalancing Becomes Non-Negotiable

As you dial in this new target allocation, the discipline of rebalancing becomes absolutely essential. It’s natural for your best-performing assets—usually stocks—to grow faster than everything else. If you don't pay attention, they can slowly take up a bigger and bigger slice of your portfolio, quietly cranking up your risk exposure without you even realizing it.

Rebalancing is just the simple act of periodically selling off some of your winners and using the cash to buy more of your underperforming assets. This brings you back to your target mix—say, back to that 60/40 stock-to-bond split. It’s a disciplined way to force yourself to sell high and buy low, keeping your portfolio perfectly aligned with your goals and making sure you stay on track for a secure retirement.

Securing Your Nest Egg for Retirement and Beyond

Once you hit your 60s and start eyeing retirement—or are already living it—the entire investment playbook gets flipped on its head. The lifelong mission of growing your wealth takes a backseat to a new, more critical priority: preserving what you’ve built and making it last.

It's a huge shift in mindset. You're no longer trying to hit home runs with your investments. Instead, your focus is on protecting the lead you've worked so hard to create, ensuring that your nest egg can support you for the next 20, 30, or even 40 years. This new game plan calls for a much more conservative portfolio.

Shifting Gears to Income and Stability

For most retirees, a smart age-based asset allocation means holding a significant chunk of your portfolio in bonds and cash—often somewhere between 50% to 70%. These assets become the bedrock of your financial security, providing the stability and predictable income you need when a regular paycheck is no longer part of the picture.

So, why not just go 100% into "safe" assets and call it a day?

Because your portfolio has a silent enemy: inflation. The smaller portion you keep in stocks, maybe 30% to 50%, is your primary weapon against the rising cost of living. This slice of equity gives your portfolio the growth it needs to ensure your purchasing power doesn't slowly evaporate over a long retirement.

Your portfolio's construction should emphasize assets that are built to generate a steady stream of cash, such as:

- Dividend-paying stocks: Think of established, blue-chip companies with a long history of rewarding shareholders. Their consistent dividends can act like a reliable income stream.

- Government and corporate bonds: These fixed-income workhorses offer regular interest payments and are generally far less volatile than the stock market.

While these are general principles, your specific situation matters. Federal employees, for instance, have unique options and should look into strategies for maximizing FERS benefits and TSP.

A conservative allocation is your primary defense against "sequencing risk"—the immense danger of a sharp market downturn occurring just as you begin making withdrawals. A big loss in the early years of retirement can be devastating with no new income to replenish the funds.

This strategy of de-risking isn’t just some personal finance tip; it’s standard practice for the biggest players in the game. The 2025 Global Pension Assets Study revealed that pension funds all over the world systematically reduce their stock exposure as their members age, shifting into bonds to lock in gains and protect capital.

This is a powerful lesson in how the pros secure retirement funds. By adopting a similar defensive posture, you can build a nest egg that’s truly built to last.

Sample Asset Allocation for Ages 60+

For investors over 60, there's no single "correct" portfolio. It really depends on your personal risk tolerance, income needs, and overall financial health. Some retirees might need more growth, while others will prioritize maximum stability above all else.

Below is a table showing a few sample portfolio models. Think of these as starting points to help you visualize what a retirement-focused allocation might look like.

| Investor Profile | Stocks (Equities) % | Bonds (Fixed Income) % | Cash/Alternatives % | Primary Goal |

|---|---|---|---|---|

| Growth-Oriented Retiree | 50% | 40% | 10% | Moderate growth to outpace inflation |

| Balanced Retiree | 40% | 50% | 10% | Income and stability with some growth |

| Conservative Retiree | 30% | 60% | 10% | Capital preservation and steady income |

| Very Conservative Retiree | 20% | 70% | 10% | Maximum stability, minimal volatility |

These models illustrate the trade-off between growth potential (stocks) and stability (bonds). As you move from a growth-oriented to a more conservative stance, you're dialing down risk in favor of protecting your principal and ensuring your income streams are as reliable as possible. The key is finding the right balance that lets you sleep well at night.

Moving Beyond Age to Personalize Your Strategy

The age-based rules of thumb we've covered are a fantastic starting point for mapping out your investment plan. Think of them as the standard blueprint for a house. It’s a solid, proven design that works well for most people.

But that blueprint doesn’t know anything about you. It doesn’t account for your specific needs, your personal taste, or the unique piece of land you’re building on. A truly effective financial plan has to be custom-fit.

Simple age-based guidelines just can't see the full picture. Take two 40-year-olds—they could have wildly different financial lives. One might be a high-earning doctor with a pension, aiming to retire at 55. The other could be a freelance artist with an income that swings month-to-month and a dream of buying a home. A generic recommended asset allocation based on age isn't going to serve them equally. Not even close.

Tailoring Your Portfolio to Your Life

To move beyond the blueprint, you have to bring your life into the equation. These are the factors that help you fine-tune your strategy, making sure it aligns perfectly with your real-world circumstances and what you’re actually trying to achieve.

Three personal factors, in particular, should shape your final allocation:

- Risk Tolerance: This is your gut-level ability to handle market swings. When the market dives, are you the type to panic-sell, or do you see it as a buying opportunity? An honest self-assessment here is absolutely critical.

- Financial Goals: Are you on the traditional path, saving for retirement at 65? Or do you have other big goals on the horizon, like paying for a child’s education or starting a business? Goals with a shorter timeline demand a more conservative touch.

- Overall Financial Health: Think about your job stability, your emergency savings, and any other income you have. Someone with a secure government job and a pension can afford to take on more risk than someone whose income is far less predictable.

Your portfolio should be a reflection of your entire financial life, not just your date of birth. The goal is to build a strategy that lets you sleep well at night, confident that your investments are working for you.

For instance, an investor who is comfortable with a bit more risk might decide to lean more heavily into specific market sectors. A great place to start exploring that is by understanding the key differences between growth vs. value stocks.

Ultimately, the smartest approach is to use the age-based models as your baseline and then adjust—sometimes significantly—for your personal situation. That’s how you build an investment portfolio that is both resilient and truly effective.

Answering Your Top Questions About Age-Based Investing

Okay, so you’ve got the core principles down. But when the rubber meets the road, practical questions always pop up. Getting these answers straight is what gives you the confidence to actually manage your money for the long haul, through every up and down the market throws at you.

One of the first things people ask is how often they should be tinkering with their portfolio. A good rule of thumb is to check in on your allocation at least once a year. Another trigger is if your mix gets seriously out of whack—say, by more than 5% from your target. If a monster bull market in stocks turns your 60/40 portfolio into a 67/33 split, that’s your cue. It’s time to sell some of those winning stocks and buy bonds to bring things back into balance.

Are Target-Date Funds a Good Shortcut?

You've probably seen Target-Date Funds (TDFs) offered in your 401(k). They're designed to be a "set it and forget it" solution, automatically shifting your investments to be more conservative as you get closer to retirement. For someone who just wants a hands-off strategy, they can be a fantastic option.

But here’s the catch: they’re a one-size-fits-all solution. A TDF has no idea about your personal stomach for risk, or if you have other big financial goals outside of retirement. They offer convenience, for sure, but they might not be the perfect fit for your specific financial life.

The biggest risk for many investors isn't necessarily a market crash, but the quiet, relentless erosion of purchasing power caused by inflation. Being too conservative, especially early on, can be just as damaging as being too aggressive.

What's the Real Danger of Being Too Conservative?

Look, protecting your nest egg is absolutely critical, especially as you near the finish line. But being too conservative comes with its own hidden risk. If you’re sitting on a pile of cash or low-yield bonds, you’re almost certainly losing ground to inflation.

Over 20 or 30 years, inflation is a silent killer for your savings, drastically cutting down what your money can actually buy. Any recommended asset allocation based on age has to walk that tightrope—balancing safety with enough growth to make sure your lifestyle isn't just maintained, but can thrive for decades to come.

Ready to build conviction in your investment strategy? The Investogy newsletter offers a transparent look into how a real-money portfolio is managed, sharing deep research and honest insights. Subscribe for free at https://investogy.com.

Leave a Reply