Navigating the stock market can feel overwhelming, with endless noise and conflicting advice pulling you in different directions. The key to long-term success isn't about chasing fleeting trends or timing market swings perfectly. Instead, it's about building a durable portfolio on a foundation of proven, timeless principles. This article cuts through the clutter to provide nine essential stock market investing tips designed for the modern retail investor. We will move beyond generic advice to deliver actionable strategies you can implement immediately.

Each tip is framed with practical steps and real-world scenarios to help you apply these concepts directly to your own portfolio. Forget vague theories; we will focus on the 'how' and 'why' behind each strategy, empowering you to make more informed and confident decisions. Whether you are just starting your investment journey or looking to refine an existing strategy, these insights will equip you with the tools to build lasting wealth more effectively. Let's explore the fundamental strategies that separate successful long-term investors from short-term speculators.

1. Master the Art of Consistency with Dollar-Cost Averaging

Dollar-Cost Averaging (DCA) is a powerful, systematic investment strategy that removes emotion from the equation. The concept is simple: you invest a fixed amount of money at regular intervals, such as monthly or bi-weekly, regardless of what the stock market is doing. This disciplined approach prevents the common pitfall of trying to "time the market," which is notoriously difficult even for seasoned professionals.

Instead of making one large, high-stakes investment, you spread your purchases over time. When the market is down, your fixed investment buys more shares; when it's up, it buys fewer. This mechanism is a key reason why DCA is one of the most reliable stock market investing tips for building long-term wealth.

How to Implement Dollar-Cost Averaging

Putting DCA into practice is straightforward. The core idea is automation and consistency.

- Corporate 401(k) Plans: If you contribute to a 401(k) through your employer, you're already using DCA. A set amount is automatically deducted from each paycheck and invested.

- Recurring Brokerage Investments: Most modern brokerage platforms allow you to set up automatic, recurring transfers from your bank account to purchase specific stocks or ETFs. For example, you could schedule a $500 investment into an S&P 500 index fund on the 1st of every month.

Actionable Tips for Success

To get the most out of this strategy, follow these guidelines:

- Automate Everything: Set up automatic transfers to your brokerage account to maintain consistency and avoid the temptation to skip a month.

- Choose Quality Assets: DCA works best with high-quality, long-term investments like broad-market index funds (e.g., VOO or SPY) or fundamentally sound blue-chip companies.

- Stay the Course: The true power of DCA is revealed during market downturns. Resist the urge to pause your contributions; these are the times your money works hardest, buying more shares at a discount.

2. Embrace Diversification to Manage Risk

Diversification is the time-tested principle of not putting all your eggs in one basket. It involves spreading your investments across various assets, sectors, industries, and even geographic regions to mitigate risk. The core idea, central to Modern Portfolio Theory, is that different investments react differently to the same economic event. When one part of your portfolio is down, another may be up, smoothing out your overall returns and protecting your capital from significant, concentrated losses.

This strategy is a cornerstone of sound investing and one of the most fundamental stock market investing tips for building a resilient portfolio. By combining assets that have low correlation with one another, you can reduce volatility without necessarily sacrificing long-term growth potential.

How to Implement Diversification

True diversification goes beyond simply owning a lot of different stocks. It requires a strategic allocation across distinct categories.

- Asset Class Diversification: A classic approach is a portfolio mix like 60% stocks, 30% bonds, and 10% real estate investment trusts (REITs). Each asset class behaves differently during various economic cycles.

- Sector and Geographic Diversification: Within your stock allocation, ensure you own companies across various sectors (e.g., technology, healthcare, financials) and regions. A common rule of thumb is to allocate 20-30% of your equity to international stocks.

- Index and Target-Date Funds: Exchange-Traded Funds (ETFs) and mutual funds offer instant diversification. An S&P 500 index fund gives you exposure to 500 large U.S. companies, while a target-date fund automatically diversifies and adjusts its asset mix based on your retirement timeline.

Actionable Tips for Success

To effectively diversify your portfolio, consider these practical steps:

- Aim for Broad Exposure: If investing in individual stocks, aim for 20-30 different companies across at least five different sectors to avoid over-concentration.

- Use ETFs for Simplicity: For most investors, using a few broad-market index funds (like a total U.S. stock market fund, an international fund, and a bond fund) is the most efficient way to achieve robust diversification.

- Rebalance Periodically: Over time, your best-performing assets will grow to represent a larger portion of your portfolio. Rebalance annually or semi-annually by selling some winners and buying more of your under-represented assets to maintain your target allocation.

3. Embrace the "Buy Low" Mentality with Value Investing

Value investing is a time-tested strategy centered on one core principle: buying stocks for less than their intrinsic, or true, worth. Popularized by legends like Benjamin Graham and Warren Buffett, this approach involves deep fundamental analysis to find high-quality companies that are temporarily out of favor with the market. It’s about finding a "dollar bill for 50 cents" and having the patience to wait for the market to recognize its true value.

This methodical search for bargains is one of the most reliable stock market investing tips for those with a long-term horizon. Value investors thrive during market pessimism, such as when they bought deeply discounted bank stocks after the 2008 financial crisis, knowing their underlying strength would eventually lead to a recovery.

How to Implement Value Investing

Applying value investing requires due diligence and a focus on financial health. It’s less about market trends and more about the business itself.

- Financial Statement Analysis: Dive into a company's balance sheet, income statement, and cash flow statement. You're looking for consistent earnings, healthy cash flow, and manageable debt levels.

- Intrinsic Value Calculation: The goal is to determine a company's worth independent of its current stock price. This often involves techniques like discounted cash flow (DCF) analysis. You can learn more about various stock valuation methods on investogy.com.

Actionable Tips for Success

To succeed as a value investor, discipline and analytical rigor are key:

- Look for a Margin of Safety: Only buy a stock when its market price is significantly below your calculated intrinsic value. This gap provides a "margin of safety" that protects against errors in judgment or unforeseen problems.

- Scrutinize Key Ratios: Use metrics like a low price-to-earnings (P/E), price-to-book (P/B), and price-to-sales (P/S) ratio to screen for potentially undervalued stocks.

- Be Patient: The market can take a long time to correct its pricing errors. Value investing is not a get-rich-quick scheme; it requires holding your positions for years, not months.

4. Embrace the Power of Long-Term Buy and Hold

The buy-and-hold strategy is the cornerstone of wealth creation, popularized by legendary investors like Warren Buffett. It involves purchasing stocks in quality companies with the intent to hold them for many years, often decades, ignoring the distracting noise of short-term market volatility. This patient approach allows investors to benefit from a company's fundamental growth and the immense power of compound returns over time.

This strategy is one of the most effective stock market investing tips because it aligns your portfolio with the long-term upward trend of the economy. Instead of reacting to daily news or price swings, you focus on the underlying business. The success stories are legendary, from early investors in Amazon who held through multiple crashes to Buffett's enduring stake in Coca-Cola. To learn more about this foundational strategy, you can explore the principles of what is long-term investing.

How to Implement a Buy-and-Hold Strategy

Executing a buy-and-hold strategy requires research upfront and discipline over the long haul. The goal is to identify businesses built to last.

- Focus on Fundamentals: Analyze companies with strong financial health, consistent earnings growth, and a durable competitive advantage, often called a "moat." This could be a powerful brand, proprietary technology, or significant network effects.

- Invest, Don't Speculate: Purchase shares as if you were buying a piece of the entire business, not just a ticker symbol you hope will go up. Think like an owner and commit to holding through market cycles.

Actionable Tips for Success

To succeed with buy-and-hold investing, your mindset is as important as your stock selections.

- Reinvest All Dividends: Automatically reinvesting dividends is crucial for turbocharging compound growth. This allows you to purchase more shares, which in turn generate more dividends.

- Conduct Annual Reviews: While you should avoid frequent trading, it's wise to review your holdings annually. Ensure the company's fundamental thesis is still intact and that its competitive advantage hasn't eroded.

- Stay Patient During Downturns: Market crashes are inevitable. A buy-and-hold investor sees these periods not as a crisis but as an opportunity to potentially add to their positions in great companies at discounted prices.

5. Research Before You Invest

One of the most foundational stock market investing tips championed by legends like Warren Buffett and Peter Lynch is to thoroughly research a company before buying its stock. This means going beyond the ticker symbol and a trending news headline. True due diligence involves a deep dive into the company's financial health, its position within its industry, and the quality of its leadership.

Investing without research is akin to gambling. By understanding what you own, you can make decisions based on business fundamentals rather than market noise. This analytical approach empowers you to hold confidently through volatility and identify genuine opportunities, separating them from speculative fads. It’s the difference between being a passive owner and an informed business partner.

How to Conduct Effective Research

Putting this principle into practice requires a systematic approach to gathering and analyzing information.

- Financial Statements: Start with the company's annual (10-K) and quarterly (10-Q) reports. These documents provide a wealth of information about revenue, profit margins, debt levels, and cash flow.

- Industry Analysis: Understand the competitive landscape. Who are the company’s main rivals? What are the broader trends affecting the industry, such as new regulations or technological shifts? A company like Tesla, for instance, must be evaluated against the entire evolving EV market.

Actionable Tips for Success

To make your research effective, focus on these key actions:

- Read the Reports: Don't just look at the numbers. Read the "Management's Discussion and Analysis" section in the 10-K to understand their perspective.

- Listen to Leadership: Tune into quarterly earnings calls. Hearing management answer questions from analysts provides invaluable insight into their strategy and confidence.

- Use Multiple Metrics: Avoid relying on a single metric like the P/E ratio. Use a combination of metrics like Price-to-Sales, Debt-to-Equity, and Return on Equity for a more complete picture.

- Verify Your Sources: Cross-reference information from reputable financial news outlets, independent analyst reports, and official company filings to form a well-rounded view.

6. Don't Try to Time the Market

One of the most persistent temptations in investing is the urge to "time the market"—selling before a downturn and buying right at the bottom. The reality, championed by investing legends like John Bogle and supported by decades of academic research, is that this is a fool's errand. Market timing requires two impossibly perfect decisions: when to get out and when to get back in.

Successful long-term investing hinges on "time in the market," not timing it. Staying invested through market cycles allows your portfolio to capture the powerful upward trend of the market over time. This principle is a cornerstone of sound financial strategy and one of the most critical stock market investing tips for building sustainable wealth while avoiding costly, emotion-driven mistakes.

How to Embrace "Time in the Market"

Adopting a long-term mindset involves trusting the process and focusing on what you can control, rather than trying to predict the unpredictable.

- Financial Crisis Example: Investors who panicked and sold during the 2008 financial crisis locked in massive losses. In contrast, those who stayed invested saw their portfolios fully recover by 2012 and go on to reach new all-time highs.

- The Cost of Missing Best Days: Data from J.P. Morgan shows the devastating impact of market timing. Missing just the 10 best days in the stock market over a 20-year period could cut your overall returns in half. These best days often occur in close proximity to the worst days, making it nearly impossible to selectively participate.

Actionable Tips for Success

To effectively resist the urge to time the market, build discipline into your investment process:

- Focus on Fundamentals: Instead of reacting to daily headlines, concentrate on the fundamental strength of your investments, such as a company's earnings, debt levels, and competitive advantages.

- Create an Investment Plan: Establish clear long-term goals and an investment strategy to match. A written plan serves as a rational guide during periods of market volatility.

- Tune Out the Noise: Ignore short-term market forecasts and "hot tips" from financial news or social media. These predictions are rarely accurate and designed to provoke emotional reactions.

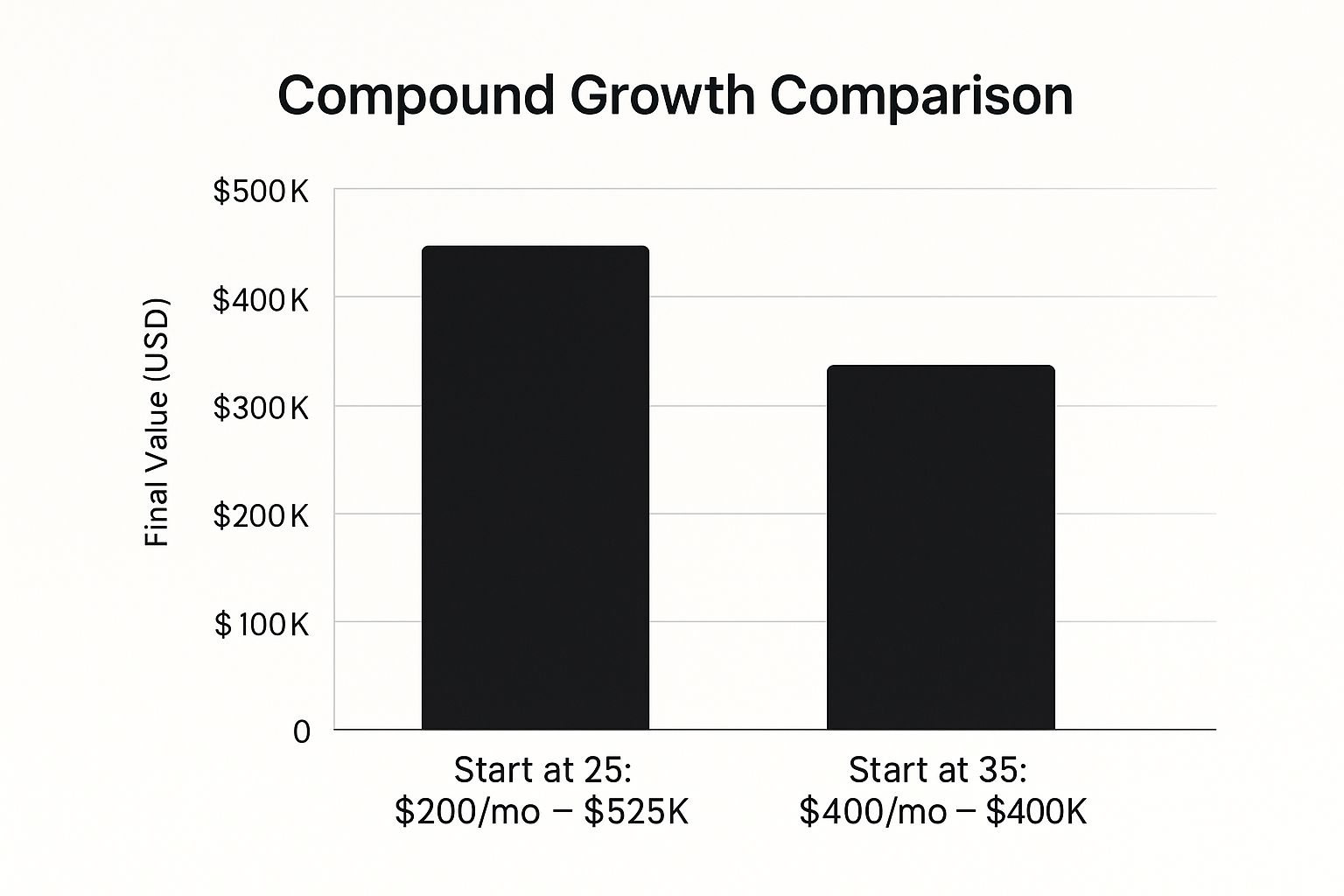

7. Start Early and Invest Regularly

The single most powerful force in your investment journey is time. Starting early and investing regularly allows you to harness the magic of compound interest, where your returns begin to generate their own returns. This principle is why even small, consistent investments made early in life can grow into a substantial nest egg, often surpassing larger investments made later.

This strategy isn't about picking winning stocks; it's about giving your money the longest possible runway to grow. By making regular contributions, you build a disciplined habit and smooth out your entry points into the market. This is one of the most fundamental stock market investing tips because it shifts the focus from timing the market to time in the market.

The bar chart below illustrates the dramatic impact of starting early, comparing two different investors who both end up contributing the same total amount over their careers but achieve vastly different outcomes.

The data clearly shows that the investor who started a decade earlier with smaller monthly contributions ended up with significantly more wealth due to the extended period of compounding.

How to Implement Early and Regular Investing

The key is to make investing a non-negotiable part of your budget from your very first paycheck.

- Open a Retirement Account Immediately: As soon as you start a new job, enroll in the 401(k) or equivalent retirement plan. If your employer offers a match, contribute at least enough to get the full amount; it’s free money.

- Establish a Roth IRA: Alongside a 401(k), a Roth IRA offers tax-free growth and withdrawals in retirement. You can set up automatic monthly contributions from your bank account.

- Custodial Accounts for Children: Parents can open custodial accounts (like an UGMA or UTMA) to give their children a multi-decade head start on investing.

Actionable Tips for Success

To maximize the advantage of time, apply these simple rules:

- Start Now, With Any Amount: Don't wait until you think you have "enough" money. Start with $50 or $100 a month. The habit is more important than the initial amount.

- Automate Your Contributions: Set up recurring investments to ensure you never miss a contribution. This removes willpower from the process.

- Increase Contributions Over Time: Every time you get a raise or a bonus, increase your automatic investment amount. This strategy, known as contribution rate escalation, accelerates your wealth building without impacting your lifestyle.

8. Understand Risk Tolerance

Understanding your risk tolerance is the bedrock of a sound investment strategy. It involves an honest assessment of both your financial ability and your emotional comfort with market volatility and potential losses. This critical self-awareness guides every decision you make, from asset allocation to the specific securities you choose, ensuring your portfolio aligns with your personal circumstances and long-term goals.

Many investors overestimate their tolerance for risk during bull markets, only to panic and sell at the worst possible time during a downturn. By defining your risk profile upfront, you create a personalized framework that helps you stay disciplined. This is one of the most fundamental stock market investing tips because it prevents emotion-driven mistakes and keeps your strategy grounded in reality, whether the market is soaring or correcting.

How to Implement Risk Tolerance Assessment

Applying this concept means translating self-knowledge into portfolio structure. Your risk profile isn't just a feeling; it's an actionable guide.

- Age and Time Horizon: A younger investor with a 30-year horizon can afford to take on more risk, perhaps with a portfolio of 90% stocks and 10% bonds, knowing they have time to recover from downturns.

- Life Stage Adjustments: An investor nearing retirement might shift to a more conservative allocation, such as 60% stocks and 40% bonds, to protect accumulated capital.

- Investment Style: A conservative investor might prefer stable, dividend-paying blue-chip stocks over speculative high-growth stocks, aligning their choices with their comfort level.

Actionable Tips for Success

To effectively gauge and apply your risk tolerance, follow these guidelines:

- Be Honest: Use risk tolerance questionnaires offered by brokerages, but answer with complete honesty, not with how you think you should feel.

- Consider Your Goals: Align your risk level with what's required to meet your financial goals. Being too conservative can be just as risky as being too aggressive if it means you fall short of your objectives.

- Reassess Periodically: Your financial situation, goals, and comfort with risk can change over time. Re-evaluate your tolerance every few years or after major life events.

- Stay Prepared: Knowing how to invest during a recession is a key part of managing risk. A solid plan for downturns can give you the confidence to stick with your strategy when it matters most. Learn more about how to invest in a recession on investogy.com.

9. Keep Costs Low

While finding winning stocks gets all the attention, one of the most powerful levers for boosting your long-term returns is something you have complete control over: minimizing costs. Investment fees, like expense ratios and trading commissions, may seem small, but they compound negatively over time, silently eroding your wealth. This is a foundational principle championed by investing legends like Vanguard founder John Bogle.

The logic is simple: every dollar you pay in fees is a dollar that isn't working for you. A 1% difference in annual fees can translate into tens or even hundreds of thousands of dollars less in your portfolio over a multi-decade investing career. This makes controlling expenses one of the most effective stock market investing tips for maximizing your net gains.

How to Implement a Low-Cost Strategy

Putting this into practice involves being a discerning consumer of financial products and services. The goal is to keep as much of your money invested as possible.

- Prioritize Low Expense Ratios: When choosing mutual funds or ETFs, the expense ratio is a critical number. For example, an S&P 500 index fund like the Vanguard 500 Index Fund ETF (VOO) has an expense ratio of just 0.03%, while some actively managed funds can charge 1.5% or more for similar exposure.

- Utilize Commission-Free Brokers: Most major brokerage firms like Fidelity, Charles Schwab, and Vanguard now offer commission-free trading for stocks and ETFs. This eliminates a significant cost, especially for investors who make regular contributions.

Actionable Tips for Success

To ensure costs don't undermine your investment growth, follow these guidelines:

- Compare Before You Buy: Always check the expense ratio and any other potential fees before investing in a fund. A tool like Morningstar or a brokerage's own research platform can help.

- Avoid Frequent Trading: Even on commission-free platforms, frequent trading can incur other costs, such as bid-ask spreads, and can create tax inefficiencies. Focus on long-term holding.

- Review Account Fees: Be aware of potential account maintenance fees, transfer fees, or inactivity fees. Choose a broker that aligns with your investing style and minimizes these charges.

9 Key Stock Market Investing Tips Comparison

| Strategy | Implementation Complexity 🔄 | Resource Requirements 🔄 | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Dollar-Cost Averaging | Low – automated, fixed schedule | Low – fixed amounts, minimal research | Reduces timing risk; lowers average cost basis | Regular investing in volatile markets | Reduces emotional decisions; disciplined approach |

| Diversification | Moderate – requires portfolio monitoring | Moderate – multiple assets and sectors | Reduces portfolio volatility; smooths returns | Risk management across assets and markets | Limits impact of failures; multiple return sources |

| Value Investing | High – extensive financial analysis required | High – deep research and valuation effort | Potential high returns; downside protection | Long-term investments in undervalued stocks | Focus on fundamentals; margin of safety |

| Long-Term Buy and Hold | Low – minimal trading, long commitment | Low – basic research on quality companies | Captures long-term growth; benefits compounding | Investors with patience for market cycles | Low costs; reduces emotional trading |

| Research Before You Invest | High – detailed analysis and due diligence | High – time-intensive and financial literacy | Improves investment success; risk reduction | For informed, confident investment decisions | Identifies red flags; builds conviction |

| Don't Try to Time the Market | Low – consistent, disciplined investment | Low – no market prediction needed | Avoids costly mistakes; more consistent returns | Long-term wealth building with market volatility | Reduces emotional stress; eliminates timing errors |

| Start Early and Invest Regularly | Low – habit formation and automatic investing | Low – small early contributions possible | Maximizes compounding; builds wealth steadily | Young investors or anyone building long-term wealth | Leverages compound interest; encourages discipline |

| Understand Risk Tolerance | Moderate – requires self-assessment | Moderate – use of tools/questionnaires | Aligns portfolio with personal risk appetite | Personalized investment allocation | Prevents panic selling; reduces stress |

| Keep Costs Low | Low to Moderate – focus on fees and expenses | Low – choose low-cost options | Higher net returns through cost savings | All investors focused on net performance | Significantly improves long-term wealth accumulation |

Your Blueprint for Smarter Investing

The path to building lasting wealth through the stock market isn't paved with complex algorithms or secret insider knowledge. Instead, it’s built upon a foundation of enduring principles, the very ones we’ve explored throughout this guide. The nine essential stock market investing tips detailed here, from the steady rhythm of dollar-cost averaging to the disciplined patience of a buy-and-hold strategy, form a comprehensive blueprint for your financial future. These aren't just isolated tactics; they are interconnected pillars designed to support a resilient and prosperous investment portfolio.

Think of it this way: embracing diversification protects you from the downfall of a single company, while diligent research ensures you’re selecting quality assets in the first place. Understanding your personal risk tolerance keeps you grounded during inevitable market storms, preventing the emotional decisions that so often lead to losses. By starting early and investing regularly, you harness the incredible power of compounding, turning small, consistent contributions into a substantial nest egg over time. These concepts work in concert, creating a powerful synergy that elevates your approach from speculative gambling to strategic wealth creation.

Weaving Theory into Action

The true value of these tips materializes when you translate them from concepts on a page to actions in your portfolio. The journey begins now, with a commitment to a disciplined, informed process. Your next steps are not to chase hot stock tips or try to predict the market’s next move. Instead, focus on these actionable pillars:

- Commit to Consistency: Automate your investments. Set up a recurring transfer to your brokerage account and an automatic investment into your chosen index funds or ETFs. This single action implements dollar-cost averaging and regular investing, removing emotion from the equation.

- Embrace a Learning Mindset: The work doesn't stop after you've made your first investment. Dedicate time each month to review your portfolio, read annual reports of the companies you own, and stay informed about broader economic trends. This isn't about market timing; it's about building conviction in your holdings.

- Prioritize Low Costs: Conduct a simple audit of your portfolio. Are you invested in high-fee mutual funds? Look for low-cost index fund or ETF alternatives. Minimizing fees is one of the few variables entirely within your control and has a massive impact on your long-term returns.

By internalizing and consistently applying these stock market investing tips, you shift from being a passive observer to an active architect of your financial destiny. You build a framework that is not only capable of weathering market volatility but is designed to capitalize on it over the long haul. The goal is to cultivate a process so robust that you can sleep soundly at night, confident that your financial plan is working for you, day in and day out.

Ready to see these principles in action? The Investogy newsletter offers a transparent, narrative-driven look into a real-money portfolio, applying the very stock market investing tips discussed here. Subscribe for free at Investogy to gain the practical insights and build the conviction needed to navigate your own investment journey with confidence.