Starting your investment journey can feel like navigating a maze. With countless options popping up on the Apple App Store and Google Play Store, the first crucial step is selecting the right tool for your specific needs. The best investing apps for beginners aren't just about offering low-cost trades; they are about providing educational resources, an intuitive user interface, and features designed to help you build solid, long-term financial habits. This guide cuts through the marketing noise to deliver a detailed, side-by-side comparison of the top platforms, from established brokerages like Fidelity and Vanguard to innovative newcomers like M1 and Public.

We'll move beyond generic feature lists to analyze each app's real-world usability, pinpoint its ideal user profile, and honestly assess its limitations. This ensures you can make a choice that aligns directly with your financial goals and confidence level. Before diving into the market, it's wise to ensure your financial foundation is secure. Understanding how to start an emergency fund provides a critical safety net, allowing you to invest with greater peace of mind.

This resource is a practical roadmap. Below, you'll find in-depth reviews, screenshots, and direct links for each app, empowering you to start investing with clarity, not confusion.

1. Apple App Store (iOS)

The Apple App Store is the essential starting point for any iPhone or iPad user looking to enter the world of investing. It’s not an investing app itself, but rather the primary, secure marketplace where you’ll discover, compare, and download the tools that fit your financial goals. For beginners, its curated environment and strict security protocols provide a trusted gateway, ensuring the apps you download are legitimate and have been vetted by Apple.

This platform excels in transparency, making it one of the best investing apps for beginners to find their perfect match. Apple’s "privacy nutrition labels" clearly show how an app uses your data before you even download it. User ratings, detailed reviews, and curated editorial lists like "Apps We Love" often highlight user-friendly finance apps, helping you sidestep overly complex platforms.

Key Details & Features

- Access: Free to use on all iOS devices (iPhone, iPad). App prices vary, but most major brokerage apps are free to download.

- Unique Feature: The Family Sharing system is a standout, enabling parents to manage and approve downloads for teen-focused accounts like Fidelity Youth, creating a safe learning environment.

- Pros: Robust security, transparent privacy labels, and a centralized system for updates and management.

- Cons: Exclusive to the Apple ecosystem; some investing platforms may offer more powerful features on their desktop web versions compared to their iOS app.

Website: https://apps.apple.com

2. Google Play Store (Android)

For Android users, the Google Play Store is the definitive hub for discovering a vast array of investing tools. Much like its Apple counterpart, it is not an investing app itself, but rather the central, secure marketplace for downloading the services that will power your financial journey. It serves as a crucial first step, offering a massive selection of vetted applications, from established brokerages like E*TRADE and Fidelity to innovative platforms like Acorns and M1 Finance.

The platform's strength lies in its extensive choice and user-driven feedback system. It provides one of the best investing apps for beginners discovery experiences by showcasing detailed user reviews, star ratings, and download counts, which help gauge an app’s popularity and reliability. Before installing, Google clearly outlines the permissions an app requires, giving you control over your data. Editorial collections and finance categories also simplify the process of finding a well-regarded, user-friendly app.

Key Details & Features

- Access: Free to use on all certified Android devices. While the store is free, individual app costs vary, though most top investing apps are free to download.

- Unique Feature: Its open nature means a wider variety of niche and upcoming investing apps are often available, giving beginners more options to find a perfect fit for their specific goals.

- Pros: The broadest selection of investing apps for Android users, transparent app permission requests, and a flexible ecosystem.

- Cons: App quality can be more varied; it's important for users to check publisher details and reviews to ensure an app's authenticity.

Website: https://play.google.com

3. Fidelity Investments

Fidelity is a powerhouse brokerage that excels in offering a comprehensive yet accessible investing experience, making it a top contender for newcomers eager to learn and grow. It’s not just an app but a full-service platform known for its robust educational resources, zero-commission online U.S. stock and ETF trades, and customer-centric features. For those just starting, Fidelity removes many traditional barriers to entry, offering an environment where you can start small and expand your knowledge with trusted tools.

The platform stands out with features like "Stocks by the Slice," allowing you to buy fractional shares of your favorite companies for as little as $1. This makes it one of the best investing apps for beginners who want to build a diversified portfolio without a large initial investment. Fidelity’s commitment to education, from in-depth articles to webinars, ensures you have the support needed to make informed decisions as your confidence grows.

Key Details & Features

- Access: Free to download and use; no account minimums to open a brokerage account.

- Unique Feature: The Fidelity Youth Account is a standout, providing teens (13-17) a hands-on way to learn about saving, spending, and investing with parental oversight, fostering early financial literacy.

- Pros: Extensive research and educational materials, exceptional customer support, and a wide array of account types, including IRAs and HSAs.

- Cons: The sheer volume of tools and data on its platform can feel overwhelming for absolute beginners compared to more simplified apps.

Website: https://www.fidelity.com

4. Charles Schwab

Charles Schwab is a full-service brokerage titan that has successfully tailored its offerings to be incredibly approachable for newcomers. It combines the power of a large, established institution with features designed to lower the barrier to entry, such as $0 commission online trades for U.S. stocks and ETFs. For beginners who value robust educational resources and the option of in-person branch support, Schwab provides a comprehensive and trusted ecosystem.

This platform stands out by making sophisticated investing tools accessible, making it one of the best investing apps for beginners who want room to grow. Its standout feature, Schwab Stock Slices, allows you to buy fractional shares of any S&P 500 company for as little as $5, simplifying diversification even with a small starting budget. For those interested in deeper analysis, the platform also offers powerful stock market research tools to help you make informed decisions.

Key Details & Features

- Access: Free to open an account with a $0 minimum deposit. Trades for U.S. stocks and ETFs are $0 online.

- Unique Feature: Schwab Stock Slices lets you purchase fractional shares of S&P 500 stocks, making it easy to own a piece of major companies without buying a full share.

- Pros: Extensive investor education, robust research tools, physical branch support, and fractional shares for easy diversification.

- Cons: Fractional shares are limited to S&P 500 stocks only, and standard expense ratios apply to mutual funds and ETFs.

Website: https://www.schwab.com

5. Vanguard

Vanguard is synonymous with low-cost, long-term investing, making it an exceptional choice for beginners who want to adopt a passive, set-it-and-forget-it strategy. The platform is built on the philosophy that keeping costs down is the key to maximizing returns over time. It's not designed for hyperactive day trading but rather for patiently building wealth through diversified, low-fee funds.

This focus on affordability and simplicity makes it one of the best investing apps for beginners who might feel overwhelmed by more complex platforms. Vanguard excels at guiding users toward goal-based investing with comprehensive educational resources. If you're interested in understanding the core differences between investment types, you can explore their insights on ETFs vs. mutual funds on investogy.com. Their entire ecosystem is geared toward helping you invest for retirement or other major life goals, not for chasing short-term market hype.

Key Details & Features

- Access: Free to download the app and open an account. No account minimums for most brokerage accounts.

- Unique Feature: Its reputation is built on industry-leading low average fund fees, with an average expense ratio that is a fraction of the industry average. They also offer $0 commissions on online Vanguard ETF and stock trades.

- Pros: Extremely low costs, a trusted and established brand for index funds and ETFs, and a strong focus on long-term financial education.

- Cons: The platform's interface is more functional than flashy, and its options trading fees (around $1 per contract) are generally higher than competitors.

Website: https://investor.vanguard.com

6. E*TRADE from Morgan Stanley

E*TRADE bridges the gap between a beginner-friendly interface and the powerful tools of a traditional brokerage, making it an excellent long-term choice. It offers a well-rounded platform where new investors can start simple with prebuilt portfolios or individual stocks and ETFs, and later grow into more advanced strategies like options trading. With $0 commission on U.S. stock and ETF trades, it removes a common barrier to entry for those just starting out.

The platform is backed by the resources of Morgan Stanley, which translates into robust research tools and extensive educational content. This makes it one of the best investing apps for beginners who want to learn as they go. Its mobile app is highly rated and provides a seamless experience for trading and account management, ensuring you can confidently manage your portfolio from anywhere. Frequent promotions for new accounts also provide an extra incentive to get started.

Key Details & Features

- Access: Free to download on iOS and Android. No account minimums for standard brokerage accounts.

- Unique Feature: Offers prebuilt portfolios of mutual funds and ETFs, which are professionally managed. This allows beginners to start with a diversified investment without needing to pick individual securities themselves.

- Pros: User-friendly platform with strong mobile apps, extensive research tools, and competitive pricing for active options traders.

- Cons: The fee structure for things outside of standard stock trades can be more complex than what you'd find at newer, app-first brokers.

Website: https://us.etrade.com

7. Robinhood

Robinhood pioneered commission-free trading, establishing itself as an app-first brokerage that demystifies the market for newcomers. Its streamlined interface and simple onboarding process make it exceptionally easy to start buying and selling stocks, ETFs, and even cryptocurrencies without facing intimidating fees or complex tools. For those just starting their financial journey, Robinhood's user experience removes many of the traditional barriers to entry.

The platform is one of the best investing apps for beginners because it prioritizes cost-effectiveness and accessibility. It offers $0 commission on stock and ETF trades and even extends this to equity options contracts, which is rare in the industry. For those looking ahead, Robinhood provides retirement IRAs with an impressive matching contribution incentive, directly boosting your savings. If you want to understand the basics of getting started, you can learn more about how to start investing with Robinhood.

Key Details & Features

- Access: Free to download and use; no account minimums. Robinhood Gold subscription offers additional features for a monthly fee.

- Unique Feature: The IRA with a 1% match (or 3% for Gold members) on all eligible contributions is a powerful incentive, effectively giving you free money for your retirement savings.

- Pros: Extremely low trading costs, a famously easy-to-use mobile experience, and strong retirement incentives through its IRA match program.

- Cons: The platform's research tools and desktop interface are less comprehensive than what traditional full-service brokers offer.

Website: https://robinhood.com

8. SoFi Invest

SoFi Invest offers a versatile, two-pronged approach perfect for newcomers who are unsure whether they want to be hands-on or hands-off. You can start with Active Investing, which allows you to buy and sell stocks and ETFs with $0 commissions, or use their automated investing service (robo-advisor) for a professionally managed portfolio. This flexibility makes it a powerful platform for evolving your investment strategy over time.

What truly sets SoFi apart is its integration into a broader financial ecosystem, including banking and loans, creating a one-stop-shop for your money. For those seeking guidance, access to Certified Financial Planners (CFPs) provides a layer of expert support often missing from other beginner platforms. This makes it one of the best investing apps for beginners who want both digital convenience and human advice.

Key Details & Features

- Access: Free to download the app. Active Investing has $0 commissions. Automated Investing has a 0.25% annual advisory fee.

- Unique Feature: The ability to access Certified Financial Planners at no extra cost provides personalized, professional guidance that is exceptionally rare for a low-cost investing platform.

- Pros: Dual active and automated investing options, integrated financial services, and portfolio themes that include alternative investments.

- Cons: The robo-advisor service is no longer free, and some users have noted the introduction of inactivity fees and certain account minimums.

Website: https://www.sofi.com/invest

9. Acorns

Acorns pioneered the concept of micro-investing, making it effortless for anyone to start building wealth with spare change. The platform automatically rounds up your everyday purchases to the nearest dollar and invests the difference into a diversified portfolio of ETFs. This "set-it-and-forget-it" approach removes the intimidation factor of lump-sum investing, making it one of the best investing apps for beginners who want to build a habit without thinking about it.

The app's strength lies in its simplicity and all-in-one financial wellness ecosystem. Beyond basic investing, Acorns offers bundled subscription tiers that include retirement accounts (Acorns Later) and checking accounts (Acorns Banking). This integration helps users manage their saving, spending, and investing within a single, streamlined interface, reinforcing positive financial behaviors at every turn.

Key Details & Features

- Access: Subscription-based. Plans start at $3/month for a Personal account (investing, retirement, checking), with higher tiers offering more features.

- Unique Feature: The Round-Ups feature is its signature offering, automatically investing spare change from linked bank accounts and credit cards. Users can also set recurring investments or use the "Paycheck Split" to divert a portion of their income directly to investments.

- Pros: Extremely beginner-friendly with its automated 'set-and-forget' style, and an all-in-one platform for banking, investing, and retirement.

- Cons: The flat monthly subscription fee can be disproportionately high for accounts with very small balances, potentially eroding early returns.

Website: https://www.acorns.com

10. Stash

Stash is designed for individuals who want to start investing but feel overwhelmed by traditional brokerage platforms. It simplifies the process by combining investing, banking, and saving into a single subscription-based service, making it an excellent all-in-one financial tool. The platform guides users through creating a diversified portfolio with fractional shares, allowing you to invest in well-known companies with as little as one dollar.

More than just a trading app, Stash acts as a financial coach with its educational content and automated tools. It’s one of the best investing apps for beginners because it actively encourages good financial habits. The Smart Portfolio feature automatically builds and rebalances a portfolio based on your risk tolerance, taking the guesswork out of investing.

Key Details & Features

- Access: Subscription-based model with plans at $3/month (Stash Growth) and $9/month (Stash+). Both plans include a personal brokerage account, retirement account access (Roth or Traditional IRA), and a banking account.

- Unique Feature: The Stock-Back® Card is a standout, rewarding you with fractional shares of stock from the companies you shop at, turning everyday spending into an investment opportunity.

- Pros: Strong emphasis on education and guidance, combines investing with budgeting tools, and the Stock-Back® feature provides a novel way to build a portfolio.

- Cons: The flat monthly subscription fee can be costly for users with very small account balances, potentially eroding investment returns.

Website: https://www.stash.com

11. M1

M1 offers a unique, hybrid approach that blends automated investing with individual stock and ETF selection. Instead of just buying assets, you create "Pies," which are visual, customizable portfolios where you set a target percentage for each slice (stock or ETF). This system is fantastic for beginners who want to build a specific portfolio and then automate their contributions without constant manual adjustments.

The platform automatically invests your deposits according to your Pie's targets and rebalances your portfolio, making it one of the best investing apps for beginners focused on disciplined, long-term wealth building. It perfectly suits those who embrace dollar-cost averaging and want a "set it and forget it" strategy that they still control. The platform fee is a key consideration, but it's waived for accounts with at least $10,000 in assets or other qualifying activities.

Key Details & Features

- Access: Free to download. A $3 per month platform fee applies unless you have a total M1 asset value of $10,000 or more, or meet other waiver criteria.

- Unique Feature: The "Pie" based investing system allows you to visually construct, fund, and automate a portfolio of up to 100 stocks and ETFs. M1’s dynamic rebalancing automatically directs new funds to underweight slices.

- Pros: Excellent for long-term automation and disciplined investing, highly customizable portfolio allocations, and commission-free trades.

- Cons: The $3 monthly fee can be a drawback for small accounts, and it offers limited intraday trading windows, making it unsuitable for active traders.

Website: https://www.m1.com

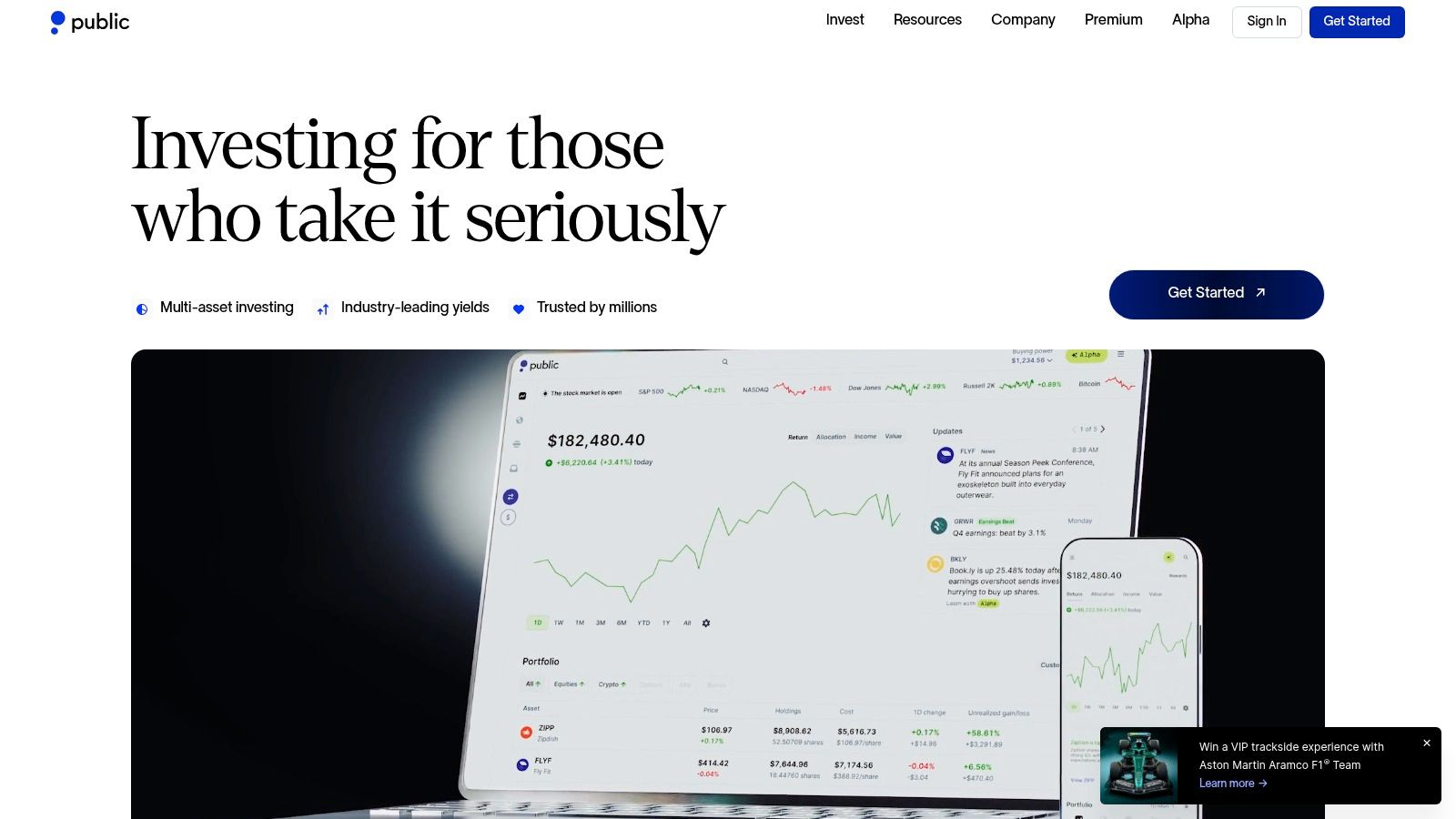

12. Public

Public merges the world of investing with social media, creating a unique platform where beginners can trade assets while learning from a community of fellow investors. The app allows users to follow experienced traders, view their portfolios (if made public), and join group chats focused on specific stocks or market trends. This transparent, community-driven approach helps demystify investing by making it a shared experience rather than a solitary one.

With commission-free trading, fractional shares, and access to alternative assets like U.S. Treasuries, Public is one of the best investing apps for beginners looking for more than just a trading tool. Its intuitive design simplifies the process of buying your first stock or ETF, while the social feed provides a constant stream of insights and discussions to help you build confidence and knowledge.

Key Details & Features

- Access: Free to download and use the base platform. Public Premium subscription is available for a monthly fee, unlocking advanced features.

- Unique Feature: The social investing feed is its core differentiator, allowing users to see what others are trading and discuss investment strategies in a collaborative environment.

- Pros: Beginner-friendly interface with strong community features, and a flexible range of investment products including alternatives.

- Cons: Key advanced features like in-depth analytics and extended-hours trading are locked behind the Premium subscription.

Website: https://public.com

Top 12 Investing Apps Feature Comparison

| Platform/App | Core Features/Characteristics | User Experience/Quality ★★★★☆ | Value Proposition 💰 | Target Audience 👥 | Unique Selling Points ✨ | Price Points 💰 |

|---|---|---|---|---|---|---|

| Apple App Store (iOS) | Curated apps, privacy labels, family controls | ★★★★☆ Secure vetting & easy updates | Free marketplace, curated apps | iPhone/iPad users, beginners | Editorial lists, app transparency | Free app downloads |

| Google Play Store (Android) | Large app selection, categories, reviews | ★★★☆☆ Broad choice, varying quality | Free marketplace, wide variety | Android users, diverse investors | Extensive selection, refund policy | Free app downloads |

| Fidelity Investments | $0 commissions, fractional shares, youth account | ★★★★★ Robust tools & education | Full-service brokerage | Beginners to advanced investors | Fractional shares, strong research | $0 commissions; options $0.65/contract |

| Charles Schwab | $0 commissions, fractional S&P 500 shares | ★★★★★ Strong education & support | Beginner-friendly, diversified | New and seasoned retail investors | Branch support, fractional shares | $0 commissions; options $0.65/contract |

| Vanguard | Low-cost ETFs, goal-based tools | ★★★★★ Trusted & cost-efficient | Passive, long-term investors | Passive investors, index fund fans | Industry-low fund fees, planning tools | $0 commissions; options ~$1/contract |

| E*TRADE from Morgan Stanley | $0 commissions, active trader pricing | ★★★★☆ User-friendly, mobile apps | Beginner to active traders | Active traders & beginners | Competitive options pricing, promotions | $0 commissions; options $0.50-$0.65/contract |

| Robinhood | Commission-free trading, IRA match | ★★★☆☆ Simple mobile, less research | Low-cost, easy onboarding | Cost-conscious beginners | IRA match, no equity options fees | $0 commissions, free options trading |

| SoFi Invest | Robo advisory, $0 commissions, CFP access | ★★★★☆ Integrated finance & advice | Beginner to intermediate | Beginners needing advice | CFP access, alternative portfolios | $0 commissions; 0.25% AUM robo fee |

| Acorns | Round-ups, subscriptions, banking integration | ★★★☆☆ Set-and-forget micro-investing | First-time investors | Absolute beginners | Automated round-up investing, education | $1-$5/month subscription |

| Stash | Subscription plans, Stock-Back card, custodial | ★★★☆☆ Guided investing & saving | Beginners needing guidance | New investors & savers | Stock rewards on debit card, education | $3-$9/month subscription |

| M1 | Automated pies, fractional shares, rebalancing | ★★★★☆ Customizable automation | Hands-off disciplined investors | Long-term investors | Portfolio pies, commission-free trading | $3/month fee unless waived |

| Public | Commission-free, social investing, fractionals | ★★★☆☆ Social features & simple UI | Beginners wanting community | Social investors & beginners | Community investing, premium advanced data | Free basic; Premium subscription available |

Beyond the App: Building Conviction for the Long Haul

Navigating the landscape of modern investing has never been more accessible. We've explored a dozen powerful platforms, from established giants like Fidelity and Charles Schwab that offer comprehensive research tools, to innovative fintech solutions like M1 Finance and Acorns that automate the entire process. Each of these tools represents a gateway to building wealth, but simply downloading an application is just the first step on a much longer journey.

The true challenge, and where real long-term success is forged, lies in what you do after you’ve chosen your platform. The ultimate goal isn't just to pick one of the best investing apps for beginners; it's to cultivate the knowledge and discipline required to make informed decisions and stick with them through market cycles. Tapping the ‘buy’ button is easy. Holding that position with confidence when markets are turbulent is what truly defines a successful investor.

From Tools to Strategy: Your Actionable Next Steps

The critical transition from simply using an app to investing with a clear strategy involves a few key considerations. Before you commit your capital, take a moment to crystallize your personal investment philosophy based on the options we've discussed.

- Define Your "Why": Are you saving for retirement in 30 years, a house down payment in five, or simply growing your wealth? Your timeline dictates your risk tolerance. A long-term retirement investor might lean towards a low-cost, diversified Vanguard ETF, while someone with a shorter horizon might prefer the cash management features of a platform like SoFi.

- Match the Tool to Your Temperament: Be honest about your habits. If you know you'll be tempted to constantly tinker with your portfolio, a hands-off app like Acorns or a platform encouraging long-term holds like M1 Finance might be a better fit than a commission-free trading app like Robinhood, which can encourage frequent activity.

- Commit to Continuous Learning: The app is your vehicle, but financial literacy is the fuel. Your initial investment decisions should be just the beginning of your education. Understanding why you own a particular stock or fund is paramount. This knowledge is what gives you the conviction to hold steady during inevitable market downturns instead of panic selling at the worst possible time.

Expanding Your Investment Horizon

Once you've mastered the fundamentals of stocks and ETFs, you can begin to explore other asset classes. The world of investing is constantly evolving, with new opportunities emerging in digital assets. For instance, alternative investments like Sports NFTs are carving out a niche, representing a newer frontier where passionate collectors and forward-thinking investors converge. While these are higher-risk assets not typically suited for a beginner's core portfolio, understanding them is part of a broader financial education.

Ultimately, selecting the right app is a foundational milestone. It empowers you with the access and functionality needed to execute your plan. But the enduring value comes from building a bedrock of knowledge and a disciplined process. This is how you transform a simple app on your phone into a powerful engine for achieving your most ambitious financial goals.

Ready to move beyond the app and learn the why behind smart investment decisions? The Investogy newsletter offers a transparent, real-money portfolio, showing you the research and rationale behind every move. See how conviction is built in the real world and start your journey to becoming a more confident investor. Learn more at Investogy.