Finding truly undervalued stocks is an art, a blend of hard numbers (quantitative analysis) and gut feeling (qualitative judgment). The whole point is to uncover fantastic companies that are trading for less than they're really worth. It's a game plan that champions long-term value over the flashy, short-term hype that dominates the headlines.

Searching for Value Beyond the Market Hype

It's way too easy to get swept up in the latest high-flying growth stock. But the real, lasting growth in your portfolio often comes from digging up those hidden gems. This is all about learning to see what everyone else is missing—spotting a great business whose stock price just hasn't caught up to its true potential yet.

This mindset is the absolute bedrock of value investing, the philosophy made famous by legends like Warren Buffett. At its core is one simple but incredibly powerful idea: the margin of safety.

The margin of safety is that critical gap between a stock's market price and what you calculate its intrinsic value to be. This buffer is your shield against bad luck, mistakes in your own analysis, or just a random market downturn.

Think of it as buying a dollar's worth of a business for fifty cents.

Now, this doesn't mean you just go out and buy "cheap" stocks. You're looking to buy wonderful businesses at a fair price. That distinction is everything. A stock might be cheap for a very good reason—terrible management, a dying industry, or a mountain of debt. An undervalued stock, on the other hand, is a solid company that the market has temporarily overlooked.

The Power of a Systematic Approach

To pull this off consistently, you need a repeatable process, something that marries the numbers with the story of the business. This guide lays out a clear framework to help you do just that. You'll learn how to:

- Dig into the financials: Go beyond the surface-level numbers to really get a feel for a company's health.

- Size up the soft stuff: Learn to evaluate things like competitive moats and the quality of the management team.

- Build real conviction: Develop the confidence to pull the trigger and invest when others are running for the exits.

This isn't about trying to time the market perfectly. It’s about patiently finding and investing in businesses built for the long haul.

And history is on our side with this strategy. In the United States, value stocks have historically beaten growth stocks by an average of about 4.4% annually since 1927. That's nearly a century of data showing a persistent value premium. You can learn more about this historical performance from the research at Dimensional Fund Advisors.

Mastering the Key Metrics for Stock Valuation

If you want to find genuinely undervalued stocks, you have to get comfortable with the numbers. Think of these key metrics as your financial compass—they help you cut through the market noise and see if a company's price tag actually matches its real worth.

Let's dive into the essential ratios that every serious investor needs to have in their toolkit. These are the bedrock of any solid valuation process.

Decoding the Price-to-Earnings Ratio

The Price-to-Earnings (P/E) ratio is probably the most famous valuation metric out there, and for good reason. It’s a quick-and-dirty way to see how much other investors are willing to shell out for every dollar of a company's profit. A lower P/E can be a flashing sign that a stock is on sale compared to its peers.

But—and this is a big but—context is everything. A low P/E ratio is never an automatic "buy" signal. You need to stack it up against two critical benchmarks:

- Its industry average: A P/E of 12 might look sky-high for a slow-and-steady utility company, but it could be an absolute steal for a high-growth tech firm.

- Its own history: If a company has consistently traded at a P/E of 25 for years and suddenly dips to 15, that’s your cue to start digging deeper.

As the image from Investopedia shows, the P/E gives you an initial read on valuation, but its true power is in comparison. It forces you to ask the right questions about whether the market's expectations are in line with the company's actual performance.

To help you get a handle on these foundational metrics, I've put together a quick reference table. It's a cheat sheet for what each ratio tells you and what to look for at a glance.

Essential Valuation Ratios at a Glance

| Metric | What It Measures | What to Look For | Investor Takeaway |

|---|---|---|---|

| Price-to-Earnings (P/E) | The market price per share relative to the company's annual earnings per share. | Lower than its industry and historical averages. | A low P/E can suggest a stock is undervalued, but always needs context. It's a starting point, not a conclusion. |

| Price-to-Book (P/B) | Compares a company's market value to its book value (net assets). | A ratio below 1.0 is a classic value investing signal. | Excellent for asset-heavy industries. It shows what you're paying for the company's tangible assets. |

| Debt-to-Equity (D/E) | A company’s total liabilities compared to its shareholder equity. | Generally, a ratio below 1.0 is considered healthy. | This is your financial stability check. High debt can sink a company in tough times. |

| Dividend Yield | The annual dividend per share as a percentage of the stock's current price. | A consistently high and sustainable yield. | A solid yield can indicate a mature, stable business that might be undervalued by the market. |

These are the tools of the trade. Getting familiar with them is the first step toward making smarter, more informed investment decisions instead of just following the herd.

Assessing Tangible Worth with Price-to-Book

Next on the list is the Price-to-Book (P/B) ratio. This one compares the company's market price to its book value—basically, what would be left for shareholders if the company sold off all its assets and paid every last one of its debts.

For value investors, a P/B ratio below 1.0 is often seen as a holy grail. It suggests you could be buying the company for less than its net assets are worth.

This metric really shines when you're looking at asset-heavy industries like banking, insurance, or manufacturing. It gives you a real sense of the hard, tangible value propping up your investment. On the flip side, it's not nearly as useful for businesses light on physical assets, like a software company whose main value is in its code and brand.

These numbers are all just different ways to get closer to a company's true worth, a concept we often call its intrinsic value. Understanding that core idea is what separates speculation from true investing.

Gauging Financial Health with Debt-to-Equity

A company's debt load can tell you a lot about its risk profile. The Debt-to-Equity (D/E) ratio is the metric for this job, measuring total liabilities against shareholder equity. In plain English, it shows you how much the business is running on borrowed money versus its own capital.

A high D/E ratio can be a major red flag. It might mean the company is leaning too heavily on debt to fund its growth, which ramps up the financial risk, especially when the economy hits a rough patch.

While the "right" D/E ratio can differ between industries, a figure below 1.0 is generally a good sign of financial prudence. A company with low debt has more breathing room to survive downturns and pounce on growth opportunities.

Finally, don't forget the Dividend Yield. You calculate it by dividing the annual dividend per share by the stock's price. A high, consistent yield can signal two positive things: the stock might be flying under the market's radar, and management is disciplined about returning cash to its owners. That’s often the mark of a well-run, mature business.

How to Use Stock Screeners to Find Opportunities

Trying to sort through thousands of publicly traded companies one by one is a fool's errand. It's an impossible task for any single investor, and honestly, a massive waste of time.

This is where a good stock screener becomes your secret weapon. Think of it as a powerful search engine for the entire market. It lets you apply a set of filters to sift through the noise and zero in on a manageable list of companies that actually meet your specific criteria.

Instead of hunting blindly, you can tell the screener exactly what you're looking for, building a list of businesses that already fit your value investing philosophy. This first pass lets you focus your real, deep-dive research efforts where they’ll have the most impact.

Setting Up Your First Value Screen

Getting started is pretty straightforward, especially with powerful and free tools like Finviz or Yahoo Finance. The goal here isn't to find the "perfect" company right out of the gate. It's to build a high-quality watchlist that deserves a closer look.

A great starting point for a classic value screen might include these three filters:

- Price-to-Earnings (P/E) Ratio: Set this to "Under 15." This helps find companies that aren't priced for perfection and have some room to grow.

- Price-to-Book (P/B) Ratio: Filter for "Under 1." This targets businesses potentially trading for less than the value of their net assets. It's a classic deep-value metric.

- Debt-to-Equity (D/E) Ratio: Use "Under 0.5." This weeds out companies that are drowning in debt, giving you a list with healthier balance sheets.

That simple combination immediately narrows your focus to profitable, asset-rich companies that aren't dangerously leveraged. A universe of over 8,000 stocks might shrink down to a focused list of just 50 or so companies to investigate. Now we're getting somewhere.

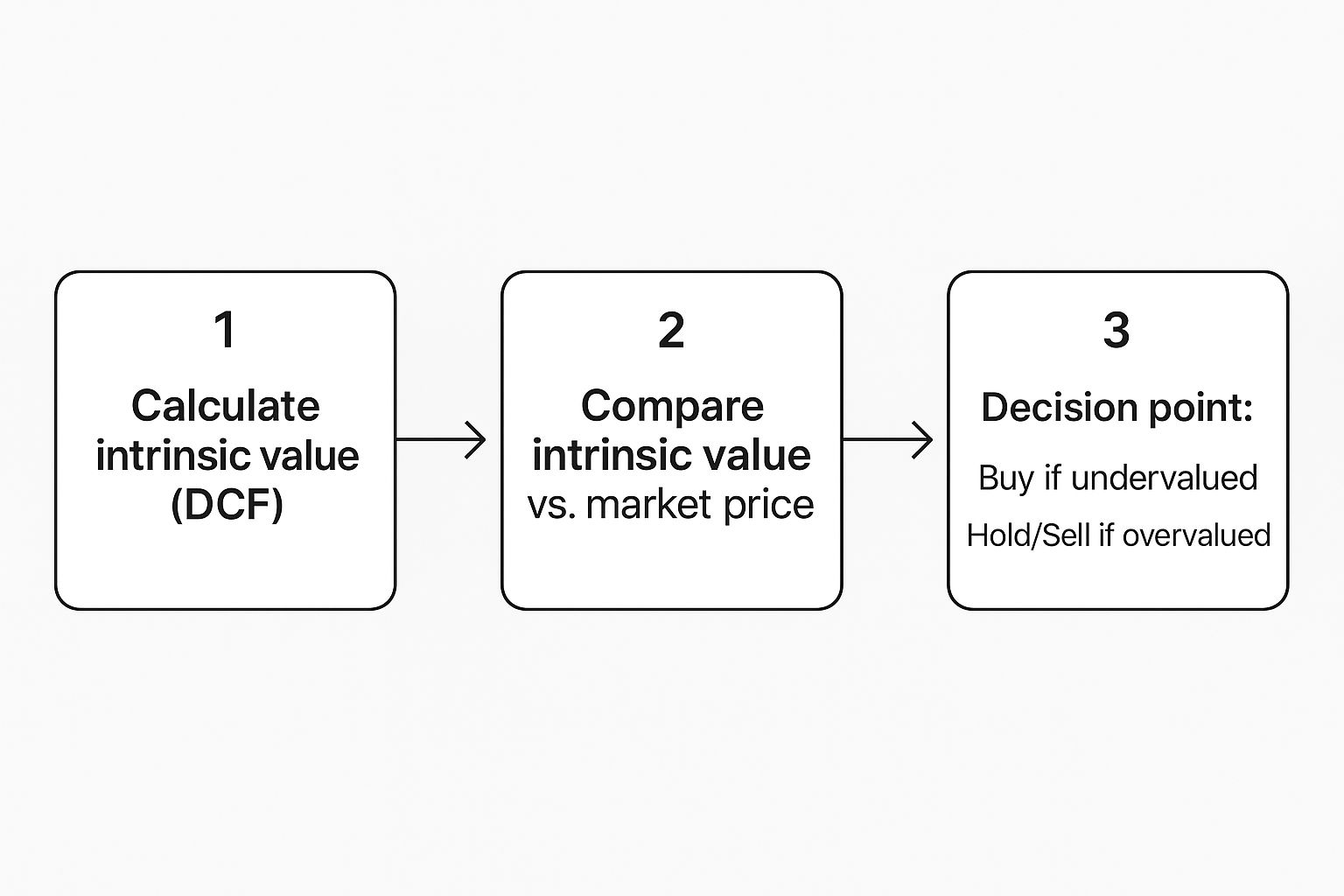

A stock screener is a starting point, not an oracle. Its job is to generate ideas for deeper research, not to give you a final buy list. The real work of analysis begins after the screen is complete.

This infographic lays out the decision-making process that comes next, turning a simple list of names into a potential investment.

As you can see, finding truly undervalued stocks is a systematic process. It involves calculation, comparison, and ultimately, a decisive action based on a solid margin of safety.

The Art of Screening Beyond the Basics

Be careful not to set your criteria in stone. A fantastic company might have a P/E of 16 and just barely miss your filter. Another might have a slightly higher D/E ratio because it's investing aggressively in a project with incredible returns.

The best approach I've found is to run several different screens.

Try one for "cheap" stocks like the one above. Then, run another for "high-quality" businesses with strong returns on equity. Maybe even create a third screen for "neglected" small-cap companies that the big funds ignore. Each one will unearth a different flavor of opportunity.

Ultimately, your screener results are just names on a page. The next, and most crucial, step is to take that curated list and begin the real work: the qualitative analysis. That means understanding the business model, its competitive advantages, and the quality of its management team. That’s how you separate the genuine bargains from the value traps.

Looking Beyond the Numbers with Qualitative Analysis

So, your stock screener spat out a tidy little list of potential investments. Great. But that was the easy part. The real work—the stuff that separates the savvy investors from the crowd—begins now.

Think of it this way: the numbers got you into the right neighborhood, but now you have to knock on some doors. You need to shift from being a data analyst to a business investigator, digging into the qualitative factors that truly define a company's staying power. This is where you find the difference between a genuine bargain and a classic value trap.

Your first and most important mission is to find the economic moat. It’s a term Warren Buffett coined, and it’s brilliant. He’s talking about a company’s sustainable competitive advantage—that invisible shield that protects its profits year after year from hungry competitors. Without a strong moat, even a great company is vulnerable.

This advantage can take a few different forms, and your job is to sniff it out. Maybe the company has a powerhouse brand that people are fiercely loyal to, like Coca-Cola. Or perhaps it's protected by unique intellectual property, like a crucial pharmaceutical patent or some piece of software that rivals simply can't copy. Sometimes, the moat is just a brutally efficient, low-cost production model that lets them consistently undercut everyone else on price.

Identifying a company's economic moat is central to understanding its long-term viability. A business without a durable advantage is like a castle without walls—it’s only a matter of time before it's overrun.

This deep dive into the business itself is the very essence of fundamental analysis. If you want to go deeper on this core investing discipline, you should check out our detailed guide on what is fundamental analysis.

Evaluating Management and Industry Position

A great business can be driven right into the ground by bad leadership. It happens all the time. That’s why your next move is to put the management team under the microscope. You're looking for leaders who aren't just experienced, but who genuinely act like owners with the shareholders' best interests at heart.

I always look for a few key traits:

- A history of smart capital allocation: How do they spend the company’s money? Do they reinvest profits wisely to generate killer returns, or do they blow cash on flashy, overpriced acquisitions that go nowhere?

- Transparency and honesty: Crack open some past annual reports and shareholder letters. Does the CEO speak candidly about both the wins and the losses? Or is it all corporate jargon and sunshine?

- Significant ownership stakes: This is a big one for me. When the executives own a huge chunk of the company's stock, their interests are perfectly aligned with yours. They feel the pain when the stock drops and celebrate when it rises.

Finally, you need to zoom out and look at the industry itself. A fantastic company in a shrinking pond is going to struggle, period. You want to find businesses that have a dominant position in an industry that is, at the very least, stable, if not growing.

The holy grail for an undervalued stock is often a great company dealing with a temporary, fixable problem—some issue that has spooked the market but doesn't actually damage the long-term health of the business.

Lessons from Market History

Looking at real-world examples can make this all click. Take Tesla's wild ride after its IPO back in June 2010. The stock debuted at $17 per share. But within about nine months, it had plummeted to roughly $4.

At that moment, based on its massive growth potential in the budding electric vehicle market, the stock was incredibly undervalued. Investors who did their homework and recognized Tesla's long-term vision had a golden opportunity to buy shares at a massive discount. Of course, hindsight is 20/20, but the signs were there for those willing to look past the short-term noise.

Ultimately, this qualitative digging adds the essential context to your numbers. It’s the art that completes the science. It’s how you build genuine conviction in an investment before you put your hard-earned money on the line.

Uncovering Value in Different Market Segments

True value isn't confined to a single corner of the market. It can pop up anywhere, from booming tech sectors to forgotten industrial giants, but you have to be willing to look where others aren't. Your job as a value investor is to get comfortable applying the same core principles to different market segments to find those hidden opportunities.

This means being just as ready to analyze a forgotten small-cap company as you are a blue-chip behemoth that has fallen on hard times. The key is adapting your lens to the specific landscape you're exploring. A low P/E ratio, for example, might be a screaming buy signal in one sector but completely normal in another. If you want to get a better handle on this, our guide on understanding the price-to-earnings ratio is a great place to start.

Hunting for Gems in Small-Cap Territory

The small-cap space is often fertile ground for finding mispriced assets. These smaller companies, typically with market capitalizations under $2 billion, fly completely under the radar of Wall Street analysts and large institutional funds. Their lower trading volume and lack of media coverage create the exact kind of market inefficiencies a diligent retail investor can exploit.

Think of it this way: a massive mutual fund often has rules that prevent it from buying tiny companies. This lack of big-money attention means prices can drift far from their intrinsic value, creating the margin of safety we’re always looking for.

Identifying Temporarily Unloved Sectors

Another powerful strategy is to hunt for entire industries that have fallen out of favor. This requires a bit of a contrarian streak. When the market sours on a whole sector—like financials during a recession or energy stocks during an oil glut—it often throws the good companies out with the bad.

This is your chance to pick up industry leaders at bargain-bin prices. The key questions to ask yourself are:

- Is the industry's downturn cyclical or structural? A temporary headwind is an opportunity; a dying industry is a value trap.

- Which companies have the strongest balance sheets to weather the storm? Look for low debt and healthy cash flow.

- What is the long-term outlook for the sector once the current pessimism fades?

One practical way to do this is by focusing on small-value stocks, which often trade at significant discounts. For instance, as of mid-2025, small-value stocks in the US market were trading roughly 25% below their fair value estimates, making them the most undervalued segment of the market. You can find more insights on these kinds of market segment valuations on Morningstar.com.

Adopting this flexible, segment-aware approach dramatically expands your hunting ground. It trains you to see value not just in individual stocks, but in broader market trends and overlooked corners where fear has temporarily trumped fundamentals.

Common Questions About Finding Undervalued Stocks

Once you start digging for value, a few questions always seem to pop up. Answering them now builds the conviction you'll need to stick with it, especially when the market gets choppy and tries to shake you out of a perfectly good position.

Let's tackle a few of the big ones.

How Long Should I Wait for an Undervalued Stock to Rebound?

This is the million-dollar question, isn't it? The only honest answer is: it depends. I’ve seen the market ignore a screaming bargain for months, and in some cases, years. There’s just no predictable timeline.

The legendary Benjamin Graham had a great way of putting it: in the short run, the market is a voting machine, but in the long run, it's a weighing machine. Sooner or later, a company's true weight—its fundamental value—will be recognized.

Your job isn't to stare at the calendar. It’s to keep your eyes on the business itself. Are things still on track?

- Is the company still executing its strategy and hitting its numbers?

- Has something fundamentally broken my original investment thesis?

- Are there new, scary risks threatening its competitive edge?

If the business is still solid, patience is your best friend. Value investing is a long game. If you're looking for a quick pop, you're in the wrong playground.

Is a Cheap Stock Always an Undervalued Stock?

No. And this is probably the most important lesson in value investing. A stock can be cheap for some very good reasons—profits are in a death spiral, the entire industry is becoming obsolete, or management is just plain awful. This is what we call a value trap, and it will burn your capital.

An undervalued stock is completely different. It’s a quality business that is temporarily on sale. The market might be panicking over a bad quarter, writing off an entire sector, or simply overlooking a solid but unsexy company.

The key difference between a value trap and a true bargain is a credible path forward. A genuinely undervalued company has a catalyst on the horizon that will force the market to re-evaluate its worth—maybe it's a new product launch, improving profit margins, or a change in leadership.

Always dig into why a stock is cheap. If you can't build a solid case for a rebound based on the quality of the business, walk away.

What If My Analysis Is Wrong?

You will be. I’ve been wrong plenty of times, and so has every great investor you can name. Nobody bats a thousand. This is exactly why the concept of a margin of safety is the absolute bedrock of this entire strategy.

When you buy a stock for much less than you think it's actually worth, you're building in a buffer against bad luck or your own mistakes. It's a cushion that protects you when your growth estimates are a little too rosy or the company hits an unexpected speed bump.

Think of it this way: if your analysis says a stock’s intrinsic value is $50 a share, buying it at $30 gives you a $20 margin of safety. If it turns out you were a bit optimistic and the company is really only worth $40, you’re still in a great position.

Getting comfortable with the fact that you won't always be right is part of becoming a better investor. A disciplined process and a healthy margin of safety are your best defenses against your own human error.

Ready to build conviction in your investment decisions? Investogy is a free weekly newsletter that shares the real-world research and strategy behind our public, real-money portfolio. See the "why" behind every trade and learn from our successes and mistakes. Subscribe for free at https://investogy.com.

Leave a Reply