So, you want to build an investment portfolio. It's not about memorizing stock tickers or chasing the latest hot trend. It really comes down to a simple, disciplined process: figuring out your goals, knowing how much risk you can stomach, picking the right assets, and then mixing them up to smooth out the ride.

This is how you build a real plan that connects your financial dreams to what you actually do with your money.

Your Framework for Building an Investment Portfolio

Jumping into building an investment portfolio is your first real move toward financial independence. Forget about what the talking heads on TV are shouting about. This is about creating a methodical, personalized blueprint for creating wealth—one that’s built for your life.

This guide will give you a practical framework for the whole process. We'll start with the stuff you absolutely need to understand before you invest a single dollar. With this foundation, you'll see that building a portfolio that actually grows over time is something anyone can do if they're willing to learn the basics.

Connecting Goals to Strategy

First things first: you need to turn those vague financial dreams into solid, time-based targets. Are you saving for retirement in 30 years? A down payment on a house in five? Your kid’s college tuition in 15? Your timeline is the single most important piece of the puzzle. It dictates everything else.

A long-term goal like retirement gives you the runway to take on more risk for potentially bigger returns. But if you’re saving for a car you want to buy next year, you need to be much more conservative to protect your cash. To get this right, you have to master the investment decision-making process, which is all about confidently prioritizing and executing your strategy.

Key Takeaway: A solid portfolio is built on clear, time-bound goals. You can't pick the right road if you don't know where you're going.

The Pillars of a Strong Investment Portfolio

Before you start picking individual stocks or funds, you need to get a handle on the core concepts that make a portfolio strong and resilient. Think of these as the bedrock of any smart investment strategy.

To really get started, you need to be familiar with a few key ideas. These are the fundamental components that every successful investor, from a beginner to a seasoned pro, relies on to build and manage their wealth.

The Pillars of a Strong Investment Portfolio

| Component | What It Is | Why It's Essential |

|---|---|---|

| Asset Classes | The main building blocks of any portfolio, like stocks, bonds, and real estate. | Each class behaves differently, offering a unique mix of risk and potential return. |

| Risk Tolerance | Your personal comfort level with the market's ups and downs. | It ensures your portfolio matches your emotional and financial ability to handle volatility. |

| Diversification | The old saying: "Don't put all your eggs in one basket." | Spreading investments around helps cushion the blow when one part of the market takes a hit. |

| Time Horizon | How long you have until you need to pull your money out. | A longer timeline generally lets you be more aggressive and aim for higher growth. |

Grasping these pillars is what turns investing from a pure gamble into a calculated plan. It's the difference between just randomly buying things and strategically assembling the right tools to build the financial future you want.

Defining Your Goals and Personal Risk Profile

Before you even think about looking at a stock or a bond, the most important work happens right between your ears. You have to get brutally honest about why you're investing in the first place and how much risk you can actually stomach.

Getting this groundwork right is what separates disciplined investors from those who panic and sell at the first sign of trouble. We need to move beyond vague ideas like "I want to get rich" and get specific. Your timeline, more than anything else, will dictate your entire investment strategy.

Clarifying Your Financial Goals

Think of your goals as destinations on a road trip. A quick drive across town needs a very different plan—and a different vehicle—than a six-month, cross-country adventure. Your investing approach has to match the journey.

Let's look at two real-world examples:

- Scenario A: The Future Homeowner. Sarah is 29 and has her sights set on buying a house. Her target is a $70,000 down payment, and she wants to have it in the next five years. Because her timeline is short, protecting the money she has is just as crucial as growing it.

- Scenario B: The Retirement Planner. David is 40 and is laser-focused on building a nest egg for retirement, which is still 25 years away. With decades on his side, he can afford to take on more market risk for the shot at much greater long-term growth.

Sarah’s portfolio needs to be more conservative, probably leaning heavily on less volatile assets like bonds. David, on the other hand, can build a portfolio dominated by stocks, which have historically delivered much higher returns over long stretches. If you want to dive deeper into this mindset, it's worth understanding what long-term investing truly means and how it uses time as your greatest ally.

Your investment timeline is your most valuable asset. A longer timeline allows you to ride out market downturns and benefit from the power of compounding, while a shorter timeline demands a more cautious approach to protect your principal.

Assessing Your Personal Risk Profile

Once you know your destination, you need to figure out what kind of driver you are. This isn't just a simple quiz; it's a gut check that combines two critical pieces: your risk capacity and your risk tolerance.

- Risk Capacity: This is the financial side of the coin—your actual ability to absorb a loss without derailing your life. It's objective. Someone with a stable, high-paying job and no debt has a much higher capacity for risk than someone working an unstable job with a mountain of financial commitments.

- Risk Tolerance: This is the emotional side. It’s completely subjective. How would you feel if you saw your portfolio drop by 20% in a single month? Would you see it as a buying opportunity, or would you be fighting the urge to hit the sell button?

Be honest with yourself here. It’s easy to call yourself an aggressive investor when the market is hitting all-time highs. Your true tolerance only shows up when things get ugly. Imagine logging into your account and seeing your hard-earned $50,000 suddenly worth $40,000. Your gut reaction to that scenario is a pretty powerful indicator of your real risk tolerance.

Finding Your Investor Type

Based on your goals and your honest risk assessment, you can start to see where you land on the investor spectrum. This isn't about putting you in a box; it's about creating a framework to keep you on track.

Common Investor Profiles

| Investor Type | Typical Time Horizon | Risk Tolerance | Potential Portfolio Mix |

|---|---|---|---|

| Conservative | 1-5 years | Low | 80% Bonds / 20% Stocks |

| Moderate | 5-15 years | Medium | 60% Stocks / 40% Bonds |

| Aggressive | 15+ years | High | 80% Stocks / 20% Bonds |

Pinpointing your profile creates the discipline you need to build a portfolio you can actually live with. Nailing this down is the secret to staying the course when the markets inevitably get choppy, ensuring you don't get sidetracked on the way to your financial destination.

Understanding the Building Blocks of Your Portfolio

Alright, you've got your financial goals mapped out. Now it's time to get familiar with the tools you'll use to get there. Think of building a portfolio like building a house. You wouldn't use just one material for the whole thing, right? You need a solid foundation, some flexible framing, and a roof that protects you from the elements.

In the investing world, we call these materials asset classes. Each one has a specific job to do. Mixing them the right way is how you build a portfolio that can handle market storms while still growing your wealth.

Let's break down the core building blocks you'll be working with.

Stocks: The Engine of Growth

When you buy a stock, also called an equity, you're buying a tiny piece of a company. If that company crushes it—grows its profits, expands its market—the value of your piece can go up. A lot.

For most people, stocks are the main engine for long-term growth. History shows they've beaten most other asset classes over long stretches, which is why they're crucial for big goals like retirement.

Of course, that potential for high returns comes with higher risk. Stock prices can swing wildly based on everything from a bad earnings report to a tweet. That volatility is exactly why they’re best for investors who have time on their side and can stomach the ups and downs without panicking. Digging into stock valuation methods can help you understand what separates a potentially great company from a dud.

Bonds: The Stabilizer

If stocks are your portfolio's engine, think of bonds as the suspension and brakes. When you buy a bond, you're lending money to a government or a corporation. They promise to pay you interest along the way and give you your original investment back on a specific date. Simple as that.

Bonds, or fixed-income securities, play a huge role in keeping your portfolio steady.

- Steady Income: They generate a predictable stream of cash from interest payments.

- Less Volatility: Bond prices are generally much less jumpy than stock prices.

- Diversification Power: This is the big one. Bonds often zig when stocks zag. During a recession, for example, investors tend to rush into the safety of government bonds, which can push their prices up just as stock prices are tanking. This balancing act is a cornerstone of smart investing.

Cash and Equivalents: The Safety Net

This is the most basic asset class. It’s the cash in your savings account, CDs, or a money market fund. The main purpose of cash isn't to make you rich; it’s about safety and liquidity.

You need cash for two key reasons: to have an emergency fund for life's curveballs, and to have "dry powder" ready to jump on investment opportunities when they pop up. Sure, cash won't grow much and will get eaten away by inflation over time, but it’s your ultimate source of stability.

I've found that each asset class plays a psychological role, too. Stocks give you the optimism for growth. Bonds give you the peace of mind to not sell everything in a panic. And cash gives you the security to make rational decisions instead of fearful ones.

Alternative Investments: The Wild Cards

Once you've covered the basics, there's a whole world of alternative investments. These can be a great way to diversify even further because their performance often has little to do with what the stock and bond markets are doing.

Some common alternatives include:

- Real Estate: This could be owning a rental property or investing in Real Estate Investment Trusts (REITs).

- Commodities: Think raw materials like gold, oil, or even coffee. Gold, for instance, has long been a go-to for investors worried about inflation or a weakening dollar.

- Private Equity: This means investing in companies before they go public on a stock exchange.

These assets can be more complicated and harder to sell quickly, but they can offer returns that you just can't get from traditional stocks and bonds. The trick is to really understand what you're getting into and how it fits with the rest of your strategy.

At the end of the day, a disciplined, diversified approach is what helps investors ride out the market's mood swings. The data backs this up. UBS's Global Investment Returns Yearbook, which crunches market data going back 125 years, consistently shows that a strategic mix of assets is the key to managing risk and boosting long-term returns. Investors who stick to a plan almost always do better than those who try to make big, speculative bets. You can see more on how these long-term trends shape wealth in the full 2025 yearbook analysis.

Designing Your Portfolio and Diversifying Smartly

Alright, you've figured out your goals and know how much risk you can stomach. Now for the fun part—this is where we move from planning to doing. We're going to tackle asset allocation, which is just a fancy way of saying "how you split up your money."

Honestly, this single decision will have more impact on your long-term results than trying to pick the next hot stock. It's all about deciding how much of your money goes into different buckets: stocks, bonds, and maybe some alternatives.

Constructing Your Core Portfolio

The right mix of assets is a direct reflection of your timeline and your comfort with market swings. A classic, battle-tested starting point is the 60/40 portfolio. That's 60% in stocks for growth and 40% in bonds for a bit of a safety net. For many, it's been a solid balance of growth and stability over the years.

But your personal situation is what really matters here. If you're young with decades to go until retirement, you might feel comfortable with an 80/20 or even a 90/10 split, leaning heavily into stocks for maximum growth. On the flip side, if you're getting close to retirement, you might flip that to something like a 30/70 mix, where protecting your capital is the top priority.

Think of these as templates, not rigid rules:

- Conservative (Short-Term Goals):

- 20% Stocks (just a little something for growth)

- 70% Bonds (for stability and reliable income)

- 10% Cash (for emergencies and quick access)

- Moderate (Medium-Term Goals):

- 60% Stocks (for balanced, steady growth)

- 40% Bonds (to protect against the worst of the market dips)

- Aggressive (Long-Term Goals):

- 80% Stocks (aiming for the highest possible growth)

- 20% Bonds (enough to smooth out the really rough patches)

The real key? Pick a mix that lets you sleep at night. You need to be able to stick with the plan, even when the market gets choppy, to see it through to your goals.

Diversifying Within Each Asset Class

Real diversification isn't just about owning some stocks and some bonds. That's just the first layer. To build a truly resilient portfolio, you need to diversify within each of those buckets. Buying just one company's stock and one type of bond still leaves you dangerously exposed if something goes wrong with either.

Let’s break it down. For your stock portion, you want to spread your money across different corners of the market:

- Large-Cap Stocks: These are the big, established players like Apple or Microsoft. They tend to be less volatile.

- Small-Cap Stocks: Shares in smaller, up-and-coming companies. They've got more room to grow but come with bigger price swings.

- International Stocks: Investing in companies outside of your home country is crucial. It helps protect you if your local economy hits a rough patch that doesn't affect the rest of the world.

The same logic goes for bonds. You can create a more robust bond holding by mixing ultra-safe government bonds with corporate bonds (which offer higher yields for a bit more risk) and international bonds.

Pro Tip: Look, the easiest way to do this without buying dozens of individual securities is through low-cost index funds or Exchange-Traded Funds (ETFs). For example, a single S&P 500 ETF instantly gives you a piece of 500 of the largest companies in the U.S. It's diversification in a box.

Exploring Private Markets for Enhanced Diversification

For those who want to take their diversification to the next level, the private markets are a compelling place to look. For a long time, this world was only open to big institutions, but it's becoming more accessible to individual investors. The big draw? Potential returns that aren't tied to the daily drama of the stock market.

This means investing in things like private companies, real estate deals, or infrastructure projects that aren't traded on an exchange. And it's not just a niche strategy anymore. A global survey from Adams Street Partners found that a whopping 88% of institutional investors plan to put up to 20% of their portfolios into private market co-investments. They're chasing higher potential returns and unique growth opportunities you just can't find in public stocks. You can get more details on this shift by checking out the 2025 global investor survey.

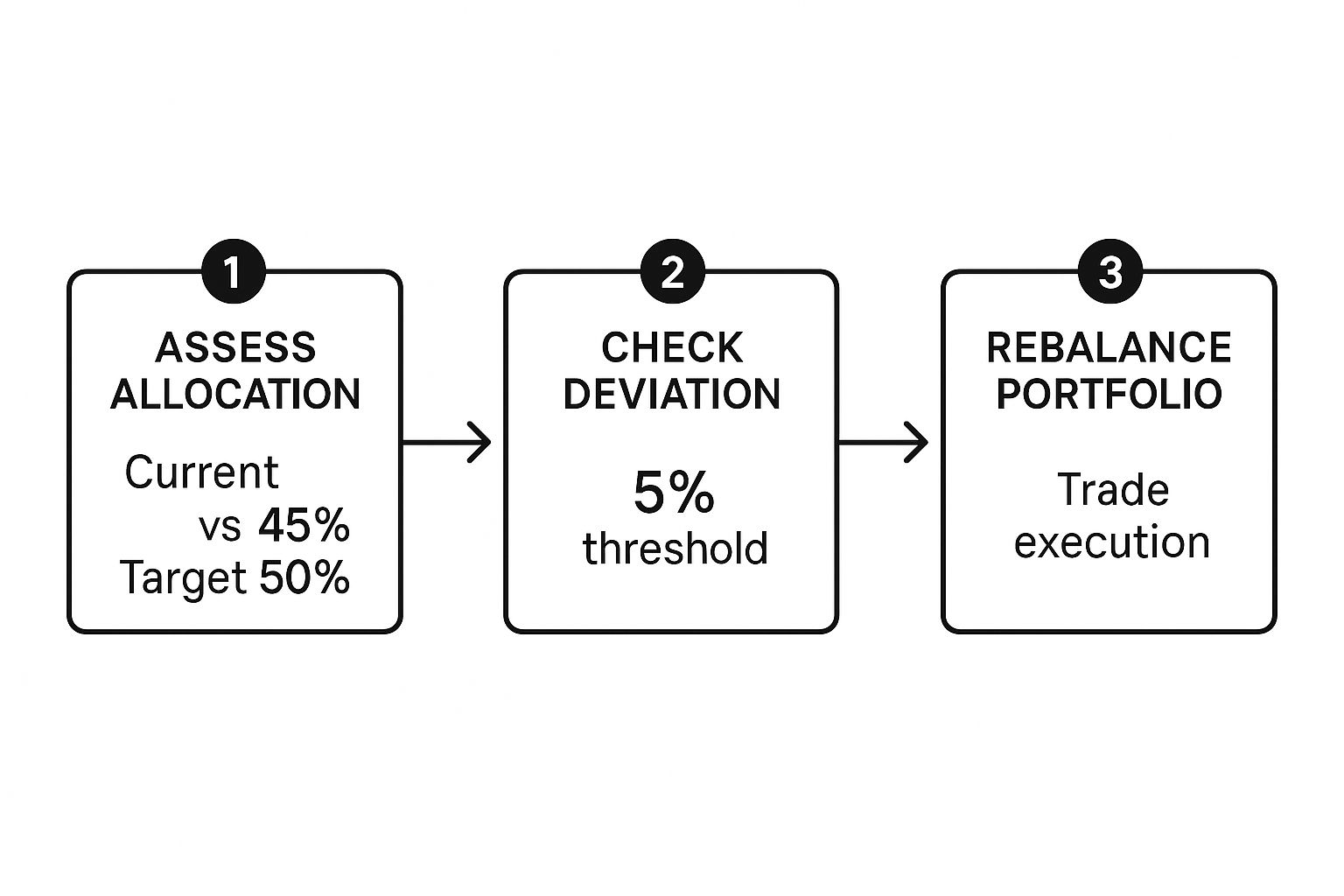

The Rebalancing Imperative

Once you've built your portfolio, the job isn't done. Your portfolio won't stay in perfect balance on its own. Some investments will grow faster than others, causing your carefully chosen allocations to drift. This is where rebalancing saves the day.

This simple infographic sums up the process perfectly.

It’s all about a disciplined cycle: check your portfolio regularly, see if any asset class has strayed too far from your target (say, by more than 5%), and then make the trades to bring it back into line. This process naturally forces you to do what every successful investor aims for: sell high and buy low.

How to Manage and Rebalance Your Portfolio

Building your portfolio is just the first step. The real work—and where long-term success is forged—is in the ongoing management. Your portfolio isn't a trophy to put on a shelf; it’s more like a garden that needs regular tending to actually produce a harvest.

This is where a lot of investors stumble. They either get glued to their screens, reacting to every market hiccup, or they completely forget about their investments for years on end. Neither approach works.

The secret is finding that sweet spot in the middle. It’s about monitoring your progress without letting the daily noise knock you off course. And, most importantly, it involves the discipline of rebalancing—a simple but incredibly powerful tool for keeping your portfolio aligned with your actual goals.

The Art of Monitoring Without Micromanaging

Once your portfolio is live, the urge to check it daily, or even hourly, can be overwhelming. This is a surefire way to make emotional, and likely poor, decisions. The goal isn't to react to every breaking news story but to make sure your overall strategy is still sound.

For most of us with a long-term view, a quarterly check-in is plenty. This schedule is frequent enough to spot if any part of your portfolio has drifted way off target, but not so frequent that you're tempted to make knee-jerk moves based on normal market volatility. It gives you a clear picture without drowning you in data.

Why Rebalancing Is Your Secret Weapon

Over time, your portfolio's original mix will naturally change. Let's say stocks have a fantastic year. Their value grows, and suddenly they make up a much larger slice of your portfolio pie than you intended. Your carefully planned 60/40 stock-to-bond portfolio might have morphed into a riskier 70/30 mix without you doing a thing.

This "portfolio drift" quietly cranks up your risk exposure. Rebalancing is the process of steering your portfolio back to its original target. It means selling a bit of your outperforming assets and using that cash to buy more of the assets that have been lagging.

It can feel totally counterintuitive. Why on earth would you sell your winners? Because rebalancing automatically enforces the oldest rule in the investing playbook: sell high and buy low. It’s a disciplined, systematic way to lock in some profits and reinvest them into assets that are temporarily on sale.

This simple act of trimming your winners is what separates a real strategy from just crossing your fingers and hoping for the best. It’s the engine that keeps your risk level right where you want it.

Choosing Your Rebalancing Strategy

There's no single "best" way to rebalance. The right method is simply the one you'll actually stick to. The two most common approaches are based on either time or a predetermined trigger.

- Calendar-Based Rebalancing: This is as straightforward as it gets. You pick a date on the calendar—quarterly, semi-annually, or annually—and you rebalance on that day, period. For example, you might decide that every January 1st, you'll get your portfolio back in line.

- Threshold-Based Rebalancing: This method is a bit more dynamic. You set a trigger point, usually a 5% band around your targets. If any single asset class drifts outside that band, it's time to rebalance. So, if your target for U.S. stocks is 40%, you’d rebalance whenever it hits 45% or dips to 35%.

Many savvy investors use a hybrid model. They check their portfolio on a set calendar (like quarterly) but only rebalance if an asset class has breached their 5% threshold. This approach avoids pointless trading costs while still making sure your risk never gets too far out of whack.

Adapting to Life and Market Changes

Your portfolio isn't set in stone; it should evolve as your life does. The aggressive strategy that made sense in your 20s probably isn't the right fit for your 50s. Major life events are a natural time to review your entire strategy. As you get closer to retirement, for instance, it's wise to gradually shift toward a more conservative allocation with a higher concentration in bonds.

It’s also smart to keep an eye on the bigger picture. Major economic and geopolitical shifts have a real impact on risk and returns. For example, JPMorgan’s recent Global Asset Allocation Views noted that even with a spike in volatility, global stocks gained over 9% in the third quarter. In that kind of environment, advisors were suggesting a moderate risk profile, focusing on specific winners like U.S. tech while also having a preference for certain types of bonds. This shows how a high-level economic view can help you make smarter tweaks to your own portfolio.

Ultimately, managing your portfolio is a marathon, not a sprint. It’s an ongoing process of small, gentle course corrections, not dramatic, panicked overhauls. By monitoring thoughtfully, rebalancing with discipline, and adapting when life calls for it, you can ensure the portfolio you worked so hard to build will continue to serve you well for years to come.

Common Investing Questions Answered

Even with a solid plan, it's completely normal to feel a little intimidated when you're just starting out. I've seen so many new investors get tripped up by the same few questions before they even make their first move. Getting some straight, no-nonsense answers is the key to pushing past that initial hesitation and actually getting your money to work.

Let's break down some of the most common hurdles I see people face.

How Much Money Do I Really Need to Start?

This is probably the biggest myth in all of investing. You can start with so much less than you think. Years ago, you might have needed a few thousand dollars to get a broker to even talk to you, but those days are long gone. Today, tons of modern brokerage platforms have no account minimums.

Seriously. You can open an account with whatever you're comfortable with, whether that's $1,000 or just $25. Thanks to fantastic tools like fractional shares, you can even own a piece of a powerhouse stock like Amazon or Apple for just a handful of dollars.

The most important thing isn't the dollar amount you start with; it’s the habit of consistent investing. An investor who puts in $50 every month without fail will almost always end up in a better position than someone who waits years to start with a large lump sum.

Consistency is what builds real wealth, not a big one-time deposit. Start small, get the hang of it, and build your momentum from there.

ETFs vs. Mutual Funds: What's the Difference?

Both Exchange-Traded Funds (ETFs) and mutual funds are incredible inventions for getting instant diversification. At their core, they both bundle hundreds or even thousands of individual stocks or bonds into a single investment you can buy easily. But, they have some key differences in how they operate and what they cost you.

Here’s a quick rundown of what you need to know:

| Feature | ETFs (Exchange-Traded Funds) | Mutual Funds |

|---|---|---|

| Trading | Trade like a stock throughout the day at changing prices. | Priced only once at the end of the trading day. |

| Fees | Generally have lower expense ratios (annual fees). | Often have higher expense ratios and may include sales loads. |

| Transparency | Holdings are typically disclosed daily, so you know what you own. | Holdings are usually disclosed quarterly or semi-annually. |

| Minimums | Can be bought for the price of a single share, even via fractional shares. | Often require a minimum initial investment (e.g., $1,000 or more). |

For most people getting started today, I find the lower costs, greater flexibility, and day-to-day transparency of ETFs make them a much more practical choice for building an investment portfolio from the ground up.

How Often Should I Check My Investments?

This is a big one. Compulsively checking your portfolio is a surefire recipe for anxiety and making bad, emotional decisions. The stock market’s daily swings are mostly noise, and reacting to that noise will almost certainly hurt your returns in the long run. You have to remember: you're a long-term investor, not a day trader.

For most of us who are building wealth over years or decades, a quarterly check-in is plenty. This is frequent enough to see if your portfolio has drifted and needs rebalancing, but infrequent enough to keep you from panicking during a totally normal market dip.

The goal is to let your well-designed strategy do the heavy lifting, not to second-guess it every time there's a scary headline.

At Investogy, we show you exactly how this looks in practice with our own real-money portfolio. Subscribe to our free weekly newsletter to see the "why" behind every decision we make. Join us at Investogy and start building your investing conviction.

Leave a Reply