When you get down to it, the whole growth vs value investing debate is pretty simple: growth investors are willing to pay a premium for future potential, while value investors are on the hunt for a bargain today. Your choice really boils down to whether you're more comfortable betting on a company's exciting story about tomorrow or its solid, and often overlooked, value right now.

Understanding Core Investment Philosophies

At its heart, choosing between growth and value investing is about your perspective on what makes a stock a winner. These aren't just simple strategies; they are complete philosophies that dictate how you look at companies, think about risk, and ultimately try to build your wealth.

Growth investing is all about identifying companies that are on a trajectory for rapid expansion. You'll often find these businesses in fast-moving sectors like technology or biotech. They typically plow every dollar of profit back into the business to fuel more innovation and grab market share. As a growth investor, you're not too worried about the stock's current price; you're focused on the potential for explosive earnings growth down the line. You're buying into a compelling story about the future.

On the other hand, value investing is a discipline focused on finding diamonds in the rough. It's about seeking out solid, established companies that the market has, for one reason or another, decided to ignore or undervalue. These stocks often trade at a discount to what they're truly worth, maybe because of a short-term hiccup or just plain negative market sentiment. A value investor is betting that eventually, the market will wise up and recognize this underlying worth, pushing the stock price up to where it belongs.

Key Takeaway: I like to think of it this way: Growth investors buy a story about what a company could become. Value investors buy tangible assets and earnings for what they're worth right now. The first group accepts higher prices for that potential, while the second demands a discount as a margin of safety.

To make it more concrete, a growth investor might happily buy shares in a hot software company with a sky-high price-to-earnings (P/E) ratio, confident its future profits will make today's price look like a steal. A value investor, meanwhile, might scoop up stock in a 100-year-old industrial manufacturer with a low P/E ratio, believing its steady cash flow and hard assets are being unfairly ignored by a market chasing fads.

This fundamental difference in approach shapes everything, from the financial metrics you care about to how long you plan to hold an investment.

To give you a clearer picture, I've put together a table that breaks down these core distinctions.

Growth vs Value Investing At a Glance

Here’s a quick-and-dirty summary of the fundamental differences between these two investing styles. Think of it as a cheat sheet to see where they diverge on key attributes.

| Attribute | Growth Investing | Value Investing |

|---|---|---|

| Primary Goal | Capital appreciation from rapid earnings growth. | Capital appreciation from market price correcting to intrinsic value. |

| Company Profile | Young, innovative companies in high-growth industries. | Established, stable companies, often in mature industries. |

| Key Metrics | High revenue/earnings growth, Price-to-Earnings Growth (PEG) ratio. | Low Price-to-Earnings (P/E), low Price-to-Book (P/B) ratios. |

| Dividend Policy | Typically low or no dividends; profits are reinvested for growth. | Often pay consistent dividends, reflecting stable cash flow. |

| Risk Profile | Higher volatility; risk of overpaying if growth doesn't materialize. | Lower volatility; risk of "value traps" where a stock stays cheap. |

| Investor Mindset | "What could this company become?" | "What is this company worth right now?" |

As you can see, the mindset, goals, and even the type of company you focus on are worlds apart. Neither is inherently "better"—they are just different tools for different jobs and different types of investors.

How Market Cycles Influence Performance

The whole growth vs. value investing debate isn't just some stuffy academic exercise; its outcome swings wildly with the economic tides. Let me be clear: neither strategy is permanently better than the other. Instead, think of them as taking turns leading the market, pushed and pulled by big-picture macroeconomic forces that favor one style for years at a time.

If you want to be a savvy investor, you have to get a handle on this cyclical nature. The economy is never static. Things like interest rates, inflation, and even just the general mood of the market create distinct periods where either growth or value stocks are set up to win. A strategy that looks brilliant one decade can completely fall flat in the next.

Take low interest rates, for example. That's basically rocket fuel for growth stocks. When money is cheap to borrow, companies can go on an investing spree to fund expansion and future projects. At the same time, investors are much more willing to pay a high price today for the promise of those distant, future profits.

The Tug of War Through History

If you look back, the performance between growth and value has been a constant tug of war, and it's almost always tied to what's happening in the broader economy. Remember the dot-com boom of the 1990s? That was a classic growth run, fueled by pure investor mania for anything tech-related. But when that bubble popped, the market got a harsh reality check. Suddenly, investors cared about tangible things again—like actual profits and dividends—which let value stocks stage a huge comeback from 2001 to 2008.

Then the 2008 financial crisis hit, and the pendulum swung right back. Rock-bottom interest rates and the unstoppable rise of Big Tech gave growth stocks another decade-plus of stellar performance. This back-and-forth pattern shows that over the last 20 years, value stocks have actually come out on top in about 46% of months. The catch is that when growth stocks win, especially in a roaring bull market, they tend to win big. For a deeper dive into these historical cycles, check out this in-depth analysis from Hartford Funds.

This history lesson hammers home a core investing truth: market leadership is always temporary. What's working wonders today probably won't work forever, which is exactly why a long-term, balanced perspective is so critical.

Key Insight: The performance of growth and value isn't random; it's a direct reflection of the economy. Figuring out which cycle we're in gives you crucial context for your investment choices and can help you avoid the classic mistake of chasing last year's winners.

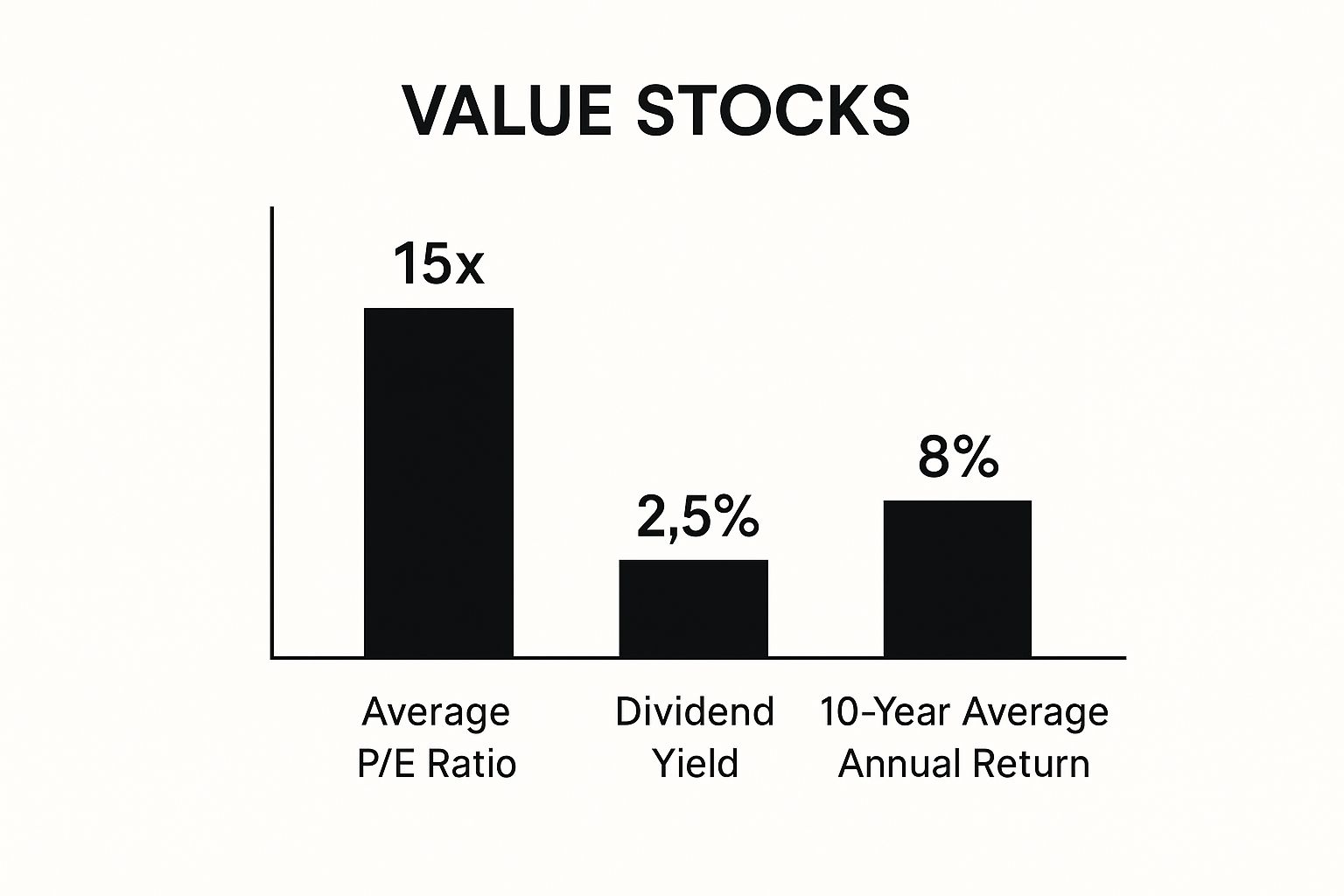

Visualizing Value Stock Fundamentals

To give you a better sense of what value investing is really about, this chart breaks down some of the classic metrics you'd look for in a typical value stock. It’s all about the fundamentals.

As you can see, value stocks aren't about explosive, headline-grabbing growth. They're defined by things like a reasonable valuation (like a P/E of 15x), a respectable dividend, and a track record of solid, long-term returns.

What Drives These Performance Cycles

So what are the economic gears turning behind the scenes? A few key indicators tend to signal whether growth or value is about to have its moment in the sun. If you understand these, you can start to anticipate potential shifts.

- Interest Rates: As I mentioned, low rates are great for growth stocks because they make the idea of future earnings more valuable right now. When rates start climbing, the opposite happens. Investors get impatient, and the steady, here-and-now cash flow from value stocks suddenly looks a lot more appealing.

- Inflation: High inflation is a major headache for growth stocks because it eats away at the real value of their projected future earnings. Value companies, often in old-school sectors like energy or consumer staples, tend to handle inflation better. They usually have more power to raise their own prices and pass those costs on to customers, protecting their profits.

- Economic Growth: When the economy is booming, optimism is high. Investors are feeling confident and are more willing to place bets on high-flying growth companies. But when the economy slows down and uncertainty creeps in, the stability and predictable profits of value stocks become a safe harbor.

At the end of the day, the historical record makes a very strong case for not putting all your eggs in one basket. The leadership baton between growth and value has been passed back and forth for decades, and there's no reason to think that's going to stop. This is why having a diversified approach—or at least being keenly aware of these market cycles—is a cornerstone of smart, long-term investing.

A Nuanced Comparison of Core Characteristics

To really get to the bottom of the growth vs. value investing debate, you have to push past the simple definitions and dig into the nitty-gritty. This means looking at the kind of companies each strategy targets, the specific financial metrics that matter, and the unique risks you're taking on. The difference isn't just a matter of numbers; it’s a fundamental split in how an investor sees a company's real worth.

Growth investors are almost always chasing the next big thing. They’re drawn to the disruptors and innovators—companies that are actively rewriting the rules of an industry. Think of a fast-scaling software-as-a-service (SaaS) business or a biotech company that’s on the verge of a major medical breakthrough. These are often young, dynamic companies laser-focused on one thing: scaling up.

On the other hand, value investors tend to prefer established players in mature industries. They might be analyzing a massive bank, an industrial manufacturing powerhouse, or a consumer goods giant that’s been a household name for decades. They’re hunting for stability, predictable cash flow, and a solid business model that they believe the market is currently undervaluing.

The Metrics That Matter Most

Because they’re looking at such fundamentally different businesses, growth and value investors rely on completely different sets of financial metrics. It's like a mechanic using a different set of tools for a sports car versus a semi-truck.

For a growth investor, it’s all about forward-looking potential:

- High Revenue Growth Rate: They want to see sales climbing fast, often at 20% or more year-over-year.

- Price-to-Sales (P/S) Ratio: Many growth companies aren't profitable yet, so this ratio helps put a valuation on the company based on its revenue stream.

- Future Earnings Potential: The analysis isn't about what the company is earning now, but what it could be earning years down the road.

Value investors, however, ground their decisions in what's tangible today. A crucial part of their analysis is understanding metrics like the price-to-book (P/B) ratio, which stacks up a company’s stock price against its net asset value. To get a better handle on this, it's worth learning more about how companies are valued relative to their book value.

They zero in on metrics that scream "bargain":

- Low Price-to-Earnings (P/E) Ratio: This is the classic signal that a stock might be cheap compared to its current earnings.

- Low Price-to-Book (P/B) Ratio: This suggests you aren't paying a huge premium for the company’s underlying assets.

- Healthy Dividend Yield: A steady dividend is often a sign of a financially sound company with management that cares about returning value to shareholders.

At its core, growth investing is about buying into a story of what a company could become. Value investing is about buying tangible assets for what they're worth right now. This philosophical divide is the most important distinction between the two.

Understanding the Inherent Risks

Neither approach is a free lunch; the risks just show up in different ways. The biggest risk with growth investing is high volatility and the very real possibility of overpaying for hype. If a company's ambitious growth story doesn't pan out, its stock can come crashing back to earth with frightening speed.

For value investors, the boogeyman is the dreaded “value trap.” This happens when a stock is cheap for a very good reason—maybe its entire industry is in a permanent state of decline, or the company has deep, unfixable operational problems. In a value trap, the stock never recovers to its "intrinsic value" and can even keep falling, locking up your capital in a losing position indefinitely.

Putting Growth and Value to Work in Your Portfolio

Okay, we've talked theory. Now for the real world. Knowing the difference between growth and value investing is one thing, but actually using that knowledge to build a portfolio is where the rubber meets the road.

There's no single "right" way to do this. The best approach for you comes down to your financial situation, how much volatility you can sleep through at night, and your timeline. Let's walk through three practical ways to build a portfolio, moving from theory to action.

Going All-In: Committing to a Single Style

The most direct path is to simply pick a side. Some investors are true believers and build their entire portfolio around either growth or value stocks. This isn't a casual decision; it demands strong conviction and a deep understanding of your own temperament as an investor.

- Who does this? A young investor with 30+ years until retirement might go all-in on growth. They have an ocean of time to recover from the inevitable market swoons and want to capture every ounce of potential from disruptive, high-flying companies.

- What's the catch? This purist approach can be a wild ride. A growth-only portfolio can get absolutely hammered during economic downturns. On the flip side, a value-only portfolio might lag for years, especially when innovation is firing on all cylinders and interest rates are low.

The Best of Both Worlds: The Core and Satellite Model

For those who don't want to put all their eggs in one basket, the core and satellite strategy is a fantastic, balanced approach. The idea is to build the "core" of your portfolio with something stable and diversified, like a broad-market index fund. Then, you use smaller "satellite" positions to make targeted bets on specific areas, like growth or value stocks.

This blended model offers a powerful middle ground. Your core provides a sturdy foundation, while your satellites let you strategically tilt your portfolio to capture specific opportunities without taking on excessive risk.

For example, you could put 70% of your portfolio—the core—into a simple S&P 500 ETF. Then you could dedicate 15% to a high-growth tech ETF and the remaining 15% to a value-focused fund that owns industrial and financial stocks. This gives you a solid base with some added spice. For a deeper dive into structuring your holdings, our guide on how to diversify an investment portfolio has you covered.

The Hybrid Approach: Growth at a Reasonable Price (GARP)

Finally, there's a group of investors who refuse to choose sides. They follow a hybrid philosophy known as "Growth at a Reasonable Price," or GARP. The goal here is simple: find the best of both worlds. GARP investors hunt for companies with strong, above-average growth that aren't yet trading at the nosebleed valuations of pure growth stocks.

These investors are looking for that sweet spot. They want exciting growth prospects but are disciplined about the price they'll pay. It’s a beautiful blend of a growth investor's forward-looking optimism with a value investor's skepticism on price.

To really nail this strategy, many investors use a stock value estimator to keep their analysis grounded. It's a fantastic way to gut-check your growth-oriented ideas with a dose of reality, helping you find fantastic companies without getting caught up in the hype and overpaying.

Making the Case for Long-Term Value

It's easy to get caught up in the hype. The financial news is constantly buzzing with stories of high-flying growth stocks. But when you step back and look at nearly a century of data, a powerful, almost counterintuitive truth emerges.

For investors with a bit of patience, value investing hasn't just kept pace—it has historically outperformed its more glamorous counterpart. This persistent edge even has a name: the "value premium."

This isn't some market anomaly or a fluke. The premium shows up again and again over decades, built on the simple but profound idea that buying solid companies for less than they're actually worth is a winning strategy. The historical evidence is hard to ignore and provides a strong anchor against the shifting tides of market sentiment.

The Decades-Long Data

Market history is littered with periods where growth stocks stole the show, but the long game tells a different story. Since 1928, U.S. value stocks have beaten growth stocks by an average of about 4.5% each year. That seemingly small gap compounds into a massive difference in wealth over an investing lifetime.

Of course, that long-term average smooths out some very rocky years. Think back to the dot-com bust in 2000. As the bubble popped, growth stocks cratered, falling a staggering 22.08%. Value stocks? They actually gained 6.08% that year, showing off their defensive strength when panic sets in.

So why does this happen? Academics and grizzled investors point to two main reasons. Some argue value stocks are just riskier—maybe they're in mature, less exciting industries—so investors naturally demand a higher return. Others chalk it up to pure behavioral finance: we humans love a good story and tend to overpay for exciting growth prospects while overreacting to bad news, creating bargain-bin prices for solid but unloved companies.

The Long-Term Perspective: The case for value investing is built on discipline and patience. It requires the conviction to buy what is unpopular and the nerve to hold on, trusting that the market will eventually recognize true worth.

Why Value Prevails Over Time

Value investing's resilience really shines after the market gets a little too frothy. When speculative bubbles burst, investors tend to scramble back to the safety of tangible assets and predictable cash flows. We saw it after the dot-com era, and we saw it again during the 2008 financial crisis, though both styles took a beating then.

Ultimately, the long-term success of value investing comes down to its core principle: buying an asset for less than its intrinsic worth. It's a cornerstone of the entire approach. For anyone looking to really master these fundamentals, our article on Warren Buffett's timeless investing principles is a fantastic place to start.

This disciplined strategy creates a "margin of safety" that helps protect your capital during downturns and delivers steady returns when the market finally comes to its senses.

The Future Outlook for Growth and Value

For the last decade, growth investing has been on an absolute tear, leaving many to wonder if value investing has permanently lost its magic. But this recent winning streak is a major break from the historical norm, and it was fueled by a pretty unique economic cocktail.

Think about it: we had historically low interest rates, the unstoppable rise of mega-cap tech companies, and a wave of globalization. That mix created a perfect storm for growth stocks. In an environment like that, future potential naturally looks a lot more exciting than boring old present-day value. Over the last decade, U.S. growth stocks beat their value counterparts by an average of 7.8% per year. That's a remarkable run, and you can dig into the full analysis of this performance divergence to see what was driving it.

Is a Reversal on the Horizon?

This long run of growth dominance has kicked off a fierce debate around a core market idea called mean reversion. This is the theory that, given enough time, asset prices and returns tend to snap back to their long-term averages. Plenty of market analysts are betting that growth's incredible outperformance can't last forever and that a shift back toward value isn't just possible—it's probable.

The real question for investors today isn't just "which one is better?" but "what's coming next?" The answer lies in recognizing that market leadership runs in cycles, and the very forces that powered growth's big decade are already changing.

The case for a value comeback usually points to rising inflation and interest rates. Those conditions tend to punish high-flying growth stocks because they make distant future earnings less valuable in today's dollars. At the same time, the steady, predictable cash flows from value companies suddenly look a lot more attractive.

This potential shift shows why having a rigid, "set-it-and-forget-it" view could be a mistake. The growth vs. value debate is constantly evolving, and the winning strategy in the years ahead will almost certainly depend on the economic climate. Making smart moves means keeping a forward-looking perspective, which is a must-have for anyone serious about what is long-term investing. The key isn't to declare one style dead, but to understand the conditions where each one is most likely to shine.

A Few Final Questions

As you get ready to put these ideas into practice, a few common questions usually pop up. Let's tackle them head-on to clear up any lingering confusion and get you investing with confidence.

Do I Have to Pick Just One? Should I Use Both Growth and Value Strategies?

Absolutely not. In fact, for most people, picking a side is a mistake. The smartest approach is usually to blend both styles. Think of it like building a well-rounded team—you want your flashy high-scorers (growth) and your solid, reliable defenders (value).

Having a mix lets you cash in on the exciting upside from innovative sectors while also grounding your portfolio with the steady, long-term potential of value stocks. This balance is your best bet for smoother returns and less stress, no matter what the market is doing.

The real debate isn't growth vs. value. It’s about how to thoughtfully combine the strengths of both philosophies to build a resilient, all-weather portfolio.

Which Is Better if I'm Just Starting Out?

Neither one is "better" in a vacuum, but if you're new to the game, the logic behind value investing can be easier to wrap your head around. It’s all about tangible numbers you can find on a balance sheet, like a company's current profits and assets. It feels more concrete.

However, an even simpler and often more effective starting point is a broad-market index fund or ETF. These funds automatically give you a piece of the whole pie—hundreds of companies, including both growth and value names—without you having to pick a single stock.

How Do I Actually Find These Stocks?

Most brokerage platforms have a stock screener tool that makes this surprisingly easy. You just set the filters for what you're looking for.

- To find growth stocks: You’d screen for things like high revenue growth or earnings growth over the past few years.

- For value stocks: You’d look for companies with a low price-to-earnings (P/E) or price-to-book (P/B) ratio.

Want an even easier path? Just invest in ETFs built specifically to track these styles. Funds like VUG focus on growth stocks, while others like VTV concentrate on value stocks. The fund does all the heavy lifting for you.

At Investogy, we're all about moving from theory to action. We don't just talk about these principles; we apply them in our own public portfolio. To see how we navigate the growth vs. value debate with real money, subscribe to our free weekly newsletter. Join for free at Investogy.com.

Leave a Reply