When you boil it all down, the fundamental difference is this: ETFs trade like stocks with real-time pricing, giving you flexibility and better tax efficiency. On the other hand, mutual funds are priced just once per day, which often suits hands-off, long-term investors just fine.

Your choice really hinges on a simple question: Do you value hands-on trading control, or do you prefer a simplified, set-it-and-forget-it approach?

ETF vs. Mutual Funds: The Key Differences

It’s easy to get lost in the weeds when comparing ETFs and mutual funds. But honestly, the most critical distinctions are pretty straightforward and they directly impact how you manage your money. The real heart of the matter is their trading structure—when you can actually buy or sell them.

This one operational difference creates a ripple effect, influencing everything from your costs to your tax bill. Think about it. For an active investor who wants to react to market news right now, being able to trade an ETF at 11:00 AM is a massive advantage. But for someone making automatic monthly contributions to their 401(k), a mutual fund's end-of-day price works perfectly.

ETF vs. Mutual Fund At a Glance

To put things in perspective, let's start with a high-level summary. This table cuts through the noise and highlights the main characteristics that separate these two hugely popular investment vehicles.

| Feature | Exchange-Traded Funds (ETFs) | Mutual Funds |

|---|---|---|

| Trading | Throughout the day on an exchange, like a stock | Once per day at the Net Asset Value (NAV) |

| Pricing | Real-time market price that fluctuates | End-of-day NAV price, set after market close |

| Typical Cost | Lower expense ratios, plus brokerage commissions | Higher expense ratios, may have sales loads |

| Tax Efficiency | Generally higher (fewer capital gains passed on) | Generally lower (can distribute capital gains) |

| Best For | Active traders, tax-conscious investors | Hands-off investors, 401(k) and retirement plans |

This table gives you a solid starting point, but the real-world implications of these differences are where things get interesting. Let’s dig a little deeper.

Liquidity and Flexibility in Action

Liquidity—or how easily you can buy or sell an asset—is a huge differentiator here. We saw a powerful real-world test of this during the extreme volatility of the COVID-19 pandemic.

As markets went on a rollercoaster ride, ETFs provided continuous price discovery and liquidity. This allowed investors to trade exactly when they felt they needed to. In contrast, many mutual funds were stuck, only able to execute trades at the day's closing price—a significant handicap during such fast-moving market chaos. You can find more analysis on this kind of event over at Ultimus Fund Solutions.

How Fund Structure Impacts Your Bottom Line

When you're picking between an ETF and a mutual fund, what's happening behind the curtain is just as critical as the fund's name. The internal plumbing—how these funds are built and traded—has a direct impact on your costs, your tax bill, and ultimately, how much money you actually make. It’s a textbook case of function following form.

The real divergence is in how shares get created and redeemed. This process is the secret sauce that often gives ETFs a huge structural advantage, especially when it comes to tax efficiency. When you buy or sell an ETF, you're usually just trading with another investor on the stock market, plain and simple.

That peer-to-peer trading is clean. But for big institutional players, it's a different game. They use a special "creation and redemption" mechanism, letting them swap a whole basket of the underlying stocks directly for new ETF shares, or vice-versa. This "in-kind" swap is a non-taxable event, which is a massive win. It lets the ETF sidestep realizing capital gains that it would otherwise have to pass down to you.

Mutual Funds and Shared Tax Burdens

Mutual funds don't work that way. When investors decide to sell their shares, the fund manager often has to sell some of the fund's underlying stocks to get the cash to pay them out. This selling activity can trigger capital gains for the entire fund.

Here's the kicker: even if you haven't sold a single share yourself, you could get hit with a capital gains distribution—and a surprise tax bill—just because a bunch of other investors decided to cash out. This "shared tax burden" is a fundamental, and frankly annoying, drawback of the mutual fund structure if you're investing in a regular taxable account.

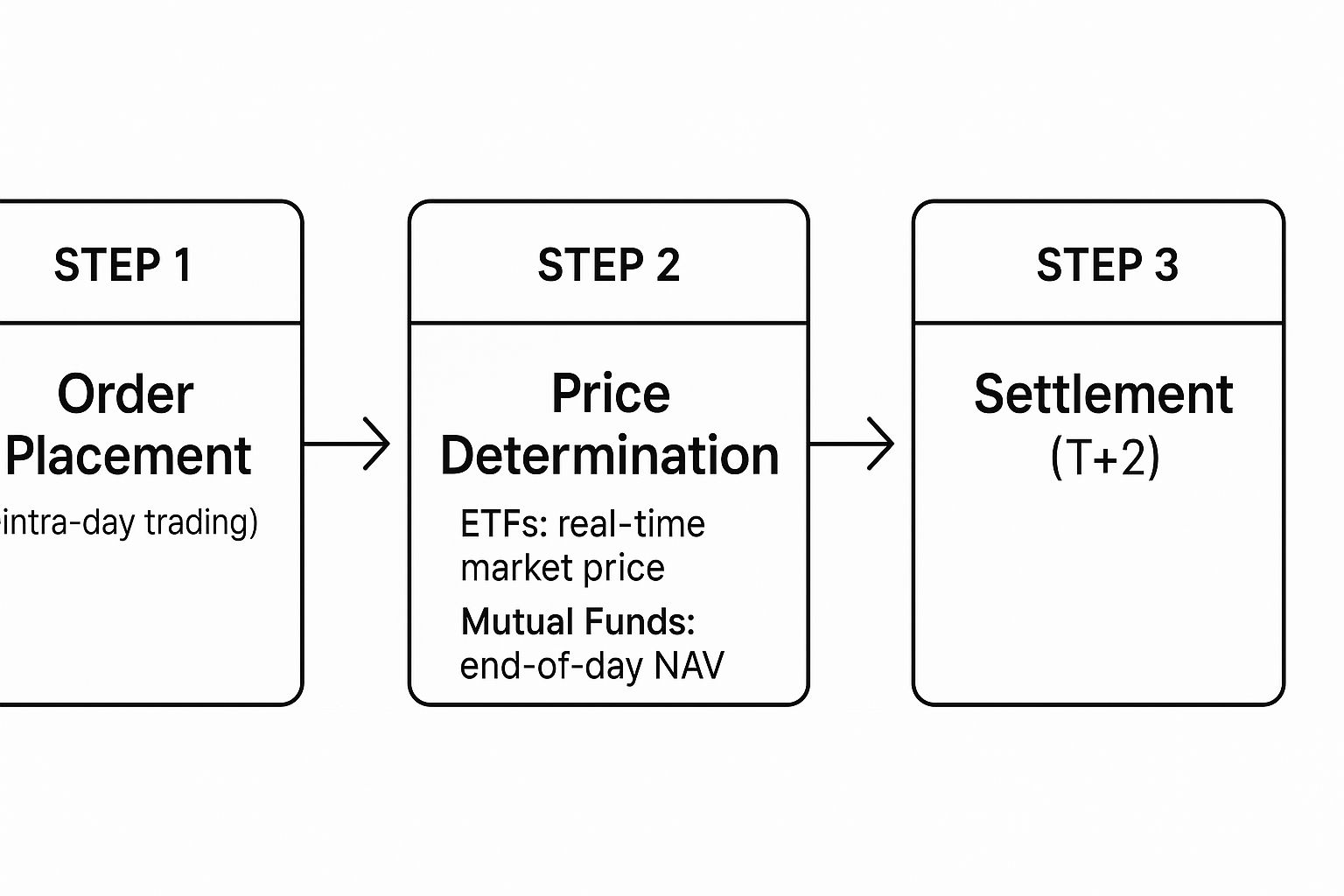

This infographic breaks down how the trading process differs, which affects when your order actually gets priced and completed.

As you can see, ETF pricing is live and dynamic throughout the day, just like a stock. Mutual funds? They're priced just once, at the end of the trading day.

Why This Matters for Your Portfolio

So, what's the real-world takeaway from all this technical jargon? The ETF structure essentially gives you a protective shield from the trading decisions of other investors. You get much more control over when you realize your own capital gains—which is typically only when you decide to sell your ETF shares.

Let's play out a scenario:

- In an ETF: You buy shares and hold them for five years. You won't owe a dime in capital gains tax until the day you sell.

- In a mutual fund: You buy and hold. But if the fund sees a wave of redemptions one year, the manager might be forced to sell appreciated stocks. This triggers a capital gains distribution that lands on your lap, and you'll owe taxes on it even though you did nothing.

This single structural difference is a core reason so many long-term investors now lean heavily toward ETFs in their taxable brokerage accounts. Over decades, minimizing these tax drags can compound into a significant amount of extra money in your pocket, not the government's.

Comparing the True Cost of Investing

When you get into the ETF vs. mutual fund debate, the conversation almost always lands on one simple assumption: ETFs are cheaper. And while that’s generally true on the surface, the "true cost" of investing is a lot more nuanced than a single number on a fact sheet. The real answer often comes down to your personal investing habits.

The most obvious fee is the expense ratio—that annual percentage skimmed off the top to cover a fund’s operating costs. ETFs, especially the big passive index trackers, almost always win this fight with rock-bottom fees. But that’s just where the cost story begins.

The Hidden Costs of Trading

For ETFs, trading costs can quietly pile up, particularly if you’re an active investor. Every time you buy or sell an ETF, you can run into a couple of costs that mutual fund investors don't have to worry about:

- Brokerage Commissions: A lot of brokers now offer commission-free trading for many ETFs, but it's not a universal guarantee. If you're trading frequently on a platform that still charges commissions, those little fees can take a serious bite out of your returns over time.

- The Bid-Ask Spread: This is the tiny gap between the highest price a buyer is willing to pay (the bid) and the lowest price a seller will take (the ask). For a super-popular ETF like SPY, this spread is practically zero. But for less-traded, niche funds, it can be a meaningful hidden cost on every single trade.

Mutual funds, on the other hand, have their own set of potential landmines. You have to watch out for sales loads, which are nasty commissions paid to a broker that can be as high as 5% or more. Then there are 12b-1 fees, which are baked in to cover marketing expenses. The trick here is to stick to no-load mutual funds, which completely sidestep that big upfront sales commission.

So, Who Wins on Cost?

It really depends on your strategy. An active trader jumping in and out of ETFs dozens of times a year might see their costs climb from spreads and commissions. At the same time, a long-term investor who unknowingly buys a mutual fund with a high sales load could end up paying way more than they should.

The most cost-effective path is often determined by your behavior. A long-term, buy-and-hold investor in a no-load, low-cost index mutual fund could face nearly identical costs to someone holding a similar ETF, making the choice less about fees and more about structure and convenience.

Research backs this up. While ETFs do tend to have lower expense ratios, that doesn't automatically translate to better net performance once all costs are considered. One study found that after accounting for all fees, ETFs still produced a net annualized CAPM alpha of about -0.75%, which wasn't drastically better than the -1.13% for actively managed mutual funds.

The big takeaway? Neither vehicle is a magic bullet for beating the market after costs. It reinforces the simple truth that you need to be vigilant about minimizing every single fee you have control over. To sharpen your strategy further, check out our guide on essential stock market investing tips.

Understanding Tax Efficiency in Your Portfolio

Taxes are one of those silent killers in your portfolio. If you’re not careful, they can slowly eat away at your hard-earned returns over decades. When you put an ETF and a mutual fund side-by-side, tax efficiency is often where ETFs pull ahead—but this advantage isn't a given in every situation. It’s not just marketing talk; it's a real benefit that’s baked right into their structure.

So, where does this "superior" tax efficiency come from? It’s all about how ETFs handle buying and selling. When an ETF manager needs to rebalance the fund, they don't usually sell stocks for cash on the open market. Instead, they can swap shares directly with large institutions in what's called an "in-kind" transfer. This simple but brilliant process sidesteps a capital gain, which means the fund isn’t forced to pass a taxable event down to you, the individual investor.

How Capital Gains Distributions Work

Contrast that with a typical actively managed mutual fund. When investors decide to cash out, especially in large numbers, the fund manager often has no choice but to sell appreciated stocks to raise the cash. This sale triggers capital gains, and by law, the fund must distribute those gains to all remaining shareholders at the end of the year.

This can lead to a seriously frustrating situation. You might get hit with a "phantom" capital gains distribution—and a surprise tax bill that comes with it—even if you never sold a single share of your mutual fund. You're literally paying taxes because of what other investors decided to do.

The Right Account for the Right Fund

This tax benefit is a huge reason to lean towards ETFs, but there's a big asterisk here: it only matters in a taxable brokerage account.

If you're investing inside a tax-advantaged retirement account like a 401(k), Roth IRA, or traditional IRA, all the growth is already tax-deferred or completely tax-free. Since you aren't paying annual capital gains taxes within these accounts anyway, the structural tax advantage of an ETF becomes totally irrelevant.

Your choice really needs to be contextual:

- Taxable Brokerage Account: This is where the tax efficiency of an ETF really shines. It can lead to significantly higher after-tax returns over the long haul. If you're investing outside of a retirement account, this is a major point in the ETF's favor.

- Retirement Account (IRA, 401(k)): The tax difference is a moot point. Here, your decision should come down to other factors, like which funds are available, what the expense ratios are, and how easily you can set up automatic investments.

To really get a handle on how different types of investment income and gains are taxed, it’s worth diving into this guide on investment tax basics covering capital gains and dividend income tax implications. Remember, where you invest is just as critical as what you invest in.

Active vs Passive: The Real Performance Driver

The debate over ETF vs mutual funds often misses the forest for the trees. While structures, fees, and tax rules are important pieces of the puzzle, the real engine behind your long-term returns isn't the wrapper—it's the investment strategy inside.

The central decision you face isn't just about choosing a fund type. It’s about choosing a philosophy: active management or passive indexing. This choice will have a far greater impact on your portfolio's performance over time.

Active management is the classic approach. A fund manager and their team of analysts try to beat the market by hand-picking stocks, bonds, or other assets they believe will outperform. For this expertise, you pay a higher fee. This strategy is available in both mutual funds and, more and more, in ETF formats.

Passive investing, or indexing, is the complete opposite. Instead of trying to find a needle in the haystack, these funds simply aim to own the whole haystack. A passive fund just buys and holds all the stocks in a market index, like the S&P 500.

The Great Shift in Investor Money

This active vs. passive distinction has completely reshaped the investment world. For decades, investors have been pouring money into low-cost index funds, and the numbers are staggering.

The evidence is undeniable. Indexed funds recently held $16.79 trillion in assets, officially blowing past the $15.88 trillion held by their active counterparts. If you want to see the data for yourself, you can learn more about this critical shift in investor preference on ici.org.

This isn't just a blip on the radar; it's an ongoing tidal wave. Investors are voting with their wallets, and the message is loud and clear: they want cost-efficient, market-mirroring strategies.

Why Performance Favors Passive

So, what's behind this massive migration to passive? It boils down to a simple, hard truth: most active managers fail to consistently beat their benchmarks, especially after their higher fees are factored in.

Decades of performance data repeatedly show that a low-cost index fund is one of the most reliable ways to build wealth. By simply accepting the market's return, you are statistically likely to outperform the majority of professionals who are paid handsomely to try and do better.

This reality reframes the entire "ETF vs. mutual fund" discussion. The better question to ask is, "Should I be an active or passive investor?" You can find great, low-cost index funds in both structures.

While our focus here is on these pooled funds, some investors do build their portfolios with individual stocks. It's always smart to weigh all your options, and it’s worth exploring how individual stocks compare to ETFs as part of your research.

Ultimately, mastering the choice between active and passive strategies is a cornerstone of our own approach at Investogy. You can see exactly how we navigate this decision in our guide to master the investment decision-making process.

Matching the Right Fund to Your Investment Style

So, after all that, what’s the final verdict in the ETF vs. mutual fund debate? The truth is, there isn't one. The best choice is intensely personal—it all boils down to your investing personality, where you're putting the money, and what you’re trying to achieve long-term.

This isn't a step to gloss over. Getting this match right is where the rubber meets the road, and it underscores the importance of due diligence to make sure your pick actually works for you. Let's walk through a few common investor profiles to see where you might fit.

When an ETF Is Likely Your Best Bet

For the hands-on investor who lives for control, flexibility, and efficiency, ETFs are tough to beat. You’re probably an ETF person if this sounds like you:

- You're an active trader. If you want the power to react to market news the second it breaks, place limit orders to snag a specific price, or set stop-losses to protect your downside, you need the intraday tradability of an ETF. It’s non-negotiable.

- You're investing in a taxable brokerage account. This is where ETFs really shine. Their structure is just flat-out better at minimizing capital gains distributions each year. Over many years, that tax efficiency can make a huge difference in your actual, take-home returns.

- You're obsessed with low costs. While great low-cost mutual funds are out there, the biggest, most popular broad-market ETFs often have the absolute rock-bottom expense ratios you can find—sometimes just a few hundredths of a percent.

For the self-directed investor managing their own taxable portfolio, the combination of intraday liquidity, tax efficiency, and ultra-low costs makes an ETF an almost automatic choice for core holdings.

When a Mutual Fund Makes More Sense

Don't count out the old guard just yet. Mutual funds still have a solid role to play, particularly for investors who value simplicity and automation above all else. A mutual fund might be the clear winner if:

- You're just starting out. Buying mutual funds can feel much more straightforward for a beginner. You can invest an exact dollar amount—say, $100—directly with the fund company, without navigating a brokerage screen or worrying about buying whole shares.

- You're automating your retirement savings. There's a reason mutual funds are the workhorse of most 401(k) plans. They are perfect for setting up automatic, recurring investments into an IRA. You just set your monthly dollar amount and forget it.

- You prefer a "set-it-and-forget-it" strategy. The fact that mutual funds only price once per day is a feature, not a bug, for many. It removes the temptation to obsessively check your portfolio or react to every little market blip, which helps enforce disciplined, long-term behavior.

At the end of the day, both are fantastic tools for building wealth. Choosing the right vehicle is just one piece of the puzzle as you figure out how to build an investment portfolio that's built to go the distance.

Lingering Questions About ETFs And Mutual Funds

Even after laying out all the details, you might still have a few questions rattling around in your head. It's completely normal. Sometimes, tackling those last points of confusion is what really cements your understanding and helps you make the final call.

So, let's clear up some of the most common questions I hear when people are weighing ETFs against mutual funds.

Are All ETFs Just Passive Index Funds?

Nope, and this is a huge misconception. It's an easy mistake to make, though. The first ETFs to hit the market, and arguably still the most famous ones, were built to passively track big indexes like the S&P 500. They were cheap, simple, and they exploded in popularity.

But the game has changed. Today, the market is flooded with actively managed ETFs. These are funds where a real, live portfolio manager is picking stocks, trying to outperform the market, just like in an active mutual fund.

Honestly, the rise of active ETFs just muddies the waters even more. It reinforces a point I've been making all along: the wrapper—ETF or mutual fund—is becoming less important than what's inside.

The real debate isn't about the fund structure (ETF vs. mutual fund). It's about the investment philosophy driving it: are you an active or a passive investor? That's the decision that truly matters.

Which One Is Better For My Retirement Account?

Inside a tax-sheltered account like a 401(k) or an IRA, one of the ETF's biggest selling points—its tax efficiency—is completely off the table. Since you aren't paying capital gains taxes in these accounts anyway, that advantage disappears.

So, the choice really boils down to logistics and what's available to you.

- Mutual Funds: These are the bread and butter of most 401(k) plans. They're built for "set it and forget it" investing, making it dead simple to set up automatic, recurring contributions every payday.

- ETFs: You'll find these more in IRAs, where you have the freedom to buy almost anything. They work perfectly fine, but you might have to be a bit more hands-on with reinvesting dividends or making those regular investments, since it's more like buying a stock.

For retirement, my advice is simple: don't get too hung up on the structure. Focus on finding a low-cost fund that gives you the asset allocation you want. Both ETFs and mutual funds are fantastic tools for building long-term wealth in a tax-advantaged account.

Ready to see how these principles work in a real-money portfolio? Subscribe to Investogy for our free weekly newsletter. We share the "why" behind every buy and sell decision, showing you how we're building wealth one investment at a time. Join us at https://investogy.com.

Leave a Reply