If you've ever felt like the stock market is just one big casino, you're not alone. Prices fly up and down based on headlines, tweets, and whatever the mood is that day. But what if there was a way to figure out what a company is actually worth, completely separate from all that noise?

That’s where intrinsic value comes in.

Think of it as the price a perfectly logical, unemotional investor would pay for a business after doing all their homework. It’s an estimate of a company's true underlying worth, based on its financial health and ability to make money in the future.

Understanding Intrinsic Value in Simple Terms

Let’s use a real-world example. Imagine you’re shopping for a house. The seller has it listed for $500,000—that’s its market price. It’s what they’re asking for right now.

But you're a savvy buyer. You look at the leaky roof, the outdated kitchen, the recent sales in the neighborhood, and what you could realistically rent it for. After running the numbers, you figure the house is really only worth $450,000. That calculated number? That's its intrinsic value.

It's the exact same game in investing. A stock's market price is just what it's trading for at this very second. Intrinsic value, on the other hand, is a carefully calculated estimate of its real, fundamental worth.

This whole idea is the foundation of value investing, a philosophy pioneered back in the 1920s by the legendary Benjamin Graham and David Dodd. They taught that smart investors should ignore the market’s mood swings and focus on the business itself. You can get a great overview of their work from Columbia Business School, where it all started.

The core idea is simple: A stock has a price, and it has a value. The goal is to buy when the price is significantly below the value.

Grasping this concept helps you answer the most important question an investor can ask: "Is this stock a genuine bargain, or is it just cheap for a very good reason?" Making that distinction is what separates disciplined, long-term investing from pure speculation.

Why Intrinsic Value Is Your Investing North Star

If you get a handle on intrinsic value, you unlock the single most powerful tool in long-term investing: the margin of safety. This is the core idea Benjamin Graham built his philosophy on, and it's what made his student Warren Buffett a household name. At its heart, it’s a defense mechanism against emotional decisions and the market's craziness.

Think about it like building a bridge. If a bridge is engineered to hold 10,000 pounds, you wouldn't drive a 9,999-pound truck across it, would you? Of course not. You need a buffer for unexpected stress, and that buffer is your margin of safety.

Investing is no different. If you do your homework and calculate a stock’s intrinsic value is about $100 per share, you don't jump in and buy it at $99. Instead, you wait. You patiently watch until the market, in one of its irrational moods, offers it to you for something far lower—maybe $70 or even $60.

That gap between the true value ($100) and your purchase price ($60) is your margin of safety. It's your cushion. It protects you if your initial calculations were a bit optimistic or if the company hits a rough patch you didn't see coming.

Making Rational Decisions in an Irrational Market

This disciplined approach forces you to be patient and rely on data, not hype. It shifts your entire focus from a stock’s wild price swings to the actual health of the underlying business. Is it consistently profitable? Does it have a real, durable competitive advantage? These are the questions that truly matter.

By anchoring every decision to your own calculation of intrinsic value, you can tune out the market’s daily noise and avoid getting swept up in the latest hot stock. This isn't just theory; recent research confirms that intrinsic value is a much better predictor of stock returns than most of the common metrics people follow.

In fact, one study showed that a portfolio strategy built around this very principle delivered an annualized outperformance of about 6.7% over two decades. You can explore the full findings on intrinsic value investing here.

"The three most important words in investing are 'margin of safety.' It's the cornerstone of investment success." – Benjamin Graham

This principle is the bedrock of value investing, but honestly, it’s a lesson that serves every single investor well. You can learn more about different investing strategies in our guide. When all is said and done, intrinsic value is the compass that will help you confidently navigate the inevitable storms of the market.

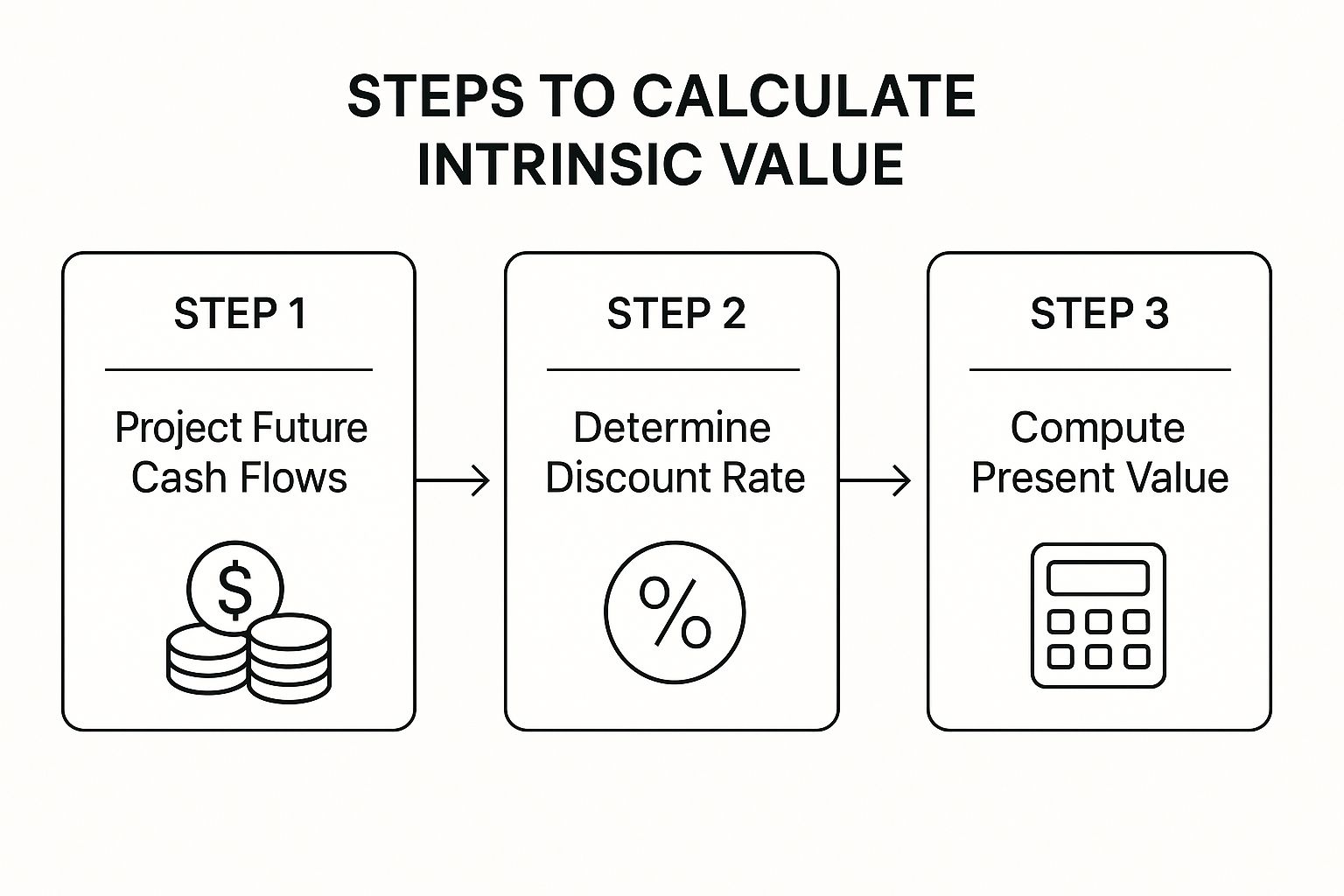

Calculating Intrinsic Value with DCF Analysis

Alright, let's move from theory to action. Of all the tools in an investor's toolkit, the Discounted Cash Flow (DCF) model is the gold standard for figuring out what a company is really worth. It might sound a little intimidating, but the idea behind it is actually pretty simple—and incredibly powerful.

Think of it like this: if you wanted to buy a local coffee shop, how would you value it? You wouldn't just look at last month's sales. You'd try to guess how much cash it will spit out over its entire lifetime, then figure out what all that future money is worth to you today. That's DCF analysis in a nutshell.

The Core Components of DCF

At its heart, the DCF model does two things: it predicts the future and then brings that future value back to the present.

- Forecasting Free Cash Flow (FCF): This is the lifeblood of a company. It’s the actual cash left over after a business pays for everything it needs to run and grow. Think of it as the money that could, in theory, be handed directly to shareholders. The first big step is to project this FCF number for the next five or ten years.

- Determining the Discount Rate: A dollar today is worth more than a dollar next year. That's because of inflation and the risk that you might not get that future dollar at all. The discount rate is simply the interest rate we use to translate those future cash flows into today's dollars. Riskier companies get a higher discount rate, which results in a lower intrinsic value.

This graphic really helps visualize how the pieces fit together.

As you can see, it's a logical flow—from predicting what's to come, to figuring out what it's worth right now.

Putting It All Together

Once you've got your cash flow forecasts and you've settled on a discount rate, the rest is just math. You take each year's projected cash flow and "discount" it back to what it's worth today.

Add up all those present values, and voilà—you have an estimate of the company's intrinsic value. It’s a quantitative way to anchor your valuation in the company's ability to generate cold, hard cash.

Key Takeaway: DCF isn’t about finding one perfect, magic number. It's an exercise in disciplined thinking. It forces you to get real about a company’s long-term prospects, its competitive moat, and all the things that could go wrong.

The final number is extremely sensitive to your assumptions. Tweak the growth rate or the discount rate just a little, and the valuation can swing wildly. This is why it’s often called more of an art than a science.

For a deeper dive into the mechanics, you can check out our detailed guide on what discounted cash flow is. Ultimately, DCF gives you a rational framework to base your decisions on, moving you away from market hype and toward financial reality.

Exploring Other Company Valuation Methods

While the DCF model is a beast for digging into a company's intrinsic value, it's definitely not the only tool in the shed. Relying on just one valuation method is a rookie mistake. Smart investors know that the real magic happens when you cross-reference your numbers using a few different techniques.

Think of it like getting a second opinion from a doctor before a big procedure. You might trust the first one, but getting confirmation from another expert gives you the confidence to move forward. Combining valuation methods helps you catch your own biases and avoid the tunnel vision that comes from staring at a single spreadsheet for too long.

Comparable Company Analysis

One of the most common-sense approaches is Comparable Company Analysis (CCA), often just called "comps." The logic is beautifully simple: a company should be worth roughly the same as other, similar companies. It’s the same way you’d price your house—you’d look at what similar homes on your street sold for recently.

With comps, you're looking at metrics like the Price-to-Earnings (P/E) ratio or Enterprise Value-to-EBITDA (EV/EBITDA) for a group of the company's direct competitors. You then take the average of those multiples and apply it to the company you're analyzing. It's a fantastic reality check that tells you what the market is willing to pay for a similar business right now.

Asset-Based Valuation

Another angle is the Asset-Based Valuation method. This one is as straightforward as it gets. You simply add up everything the company owns—cash, buildings, equipment, inventory—and then subtract everything it owes.

The core question here is: "If we had to sell off this entire company piece by piece tomorrow, what would we have left after paying all the bills?"

This approach gives you a rock-solid "floor" value for a business. It’s especially useful for heavy industrial companies, banks, or any business that’s potentially facing hard times. It strips away all the hype about future growth and focuses purely on tangible, here-and-now worth.

To get the most complete view, it's best to look at all three of these approaches—DCF, comps, and asset-based—together. Each one tells a different part of the story, and using them in tandem helps you triangulate a much more reliable estimate of what a company is truly worth.

To help you keep these straight, here’s a quick breakdown of how these three core methods stack up against each other.

Comparison of Key Valuation Methods

| Valuation Method | Best For | Pros | Cons |

|---|---|---|---|

| Discounted Cash Flow (DCF) | Stable, mature companies with predictable cash flows. | Focuses on fundamentals and long-term potential; less swayed by market moods. | Highly sensitive to assumptions about future growth and discount rates. |

| Comparable Company Analysis | Businesses in established industries with plenty of public competitors. | Grounded in current market reality; relatively quick and easy to apply. | Can be misleading if the market is overvalued or undervalued as a whole. |

| Asset-Based Valuation | Asset-heavy industries (e.g., manufacturing, real estate) or companies in distress. | Provides a conservative "floor" value; based on tangible assets. | Ignores intangible assets like brand value and future growth potential. |

As you can see, there’s no single "best" method—the right tool depends on the company you’re looking at. By combining their insights, you can build a much more nuanced and dependable valuation.

Common Mistakes to Avoid When Estimating Value

Figuring out a company's intrinsic value is definitely more art than science, and it’s shockingly easy to stumble into a few common traps. The biggest one? The classic "garbage in, garbage out" problem. Your final valuation is only as solid as the assumptions you plug into your model.

Overly optimistic growth projections are probably the most frequent offender. It’s tempting to draw a straight line up and to the right, assuming a company will keep growing at a breakneck pace forever. But the reality is, very few businesses can sustain that kind of momentum for long. Always ground your forecasts in what’s actually happened historically and what’s going on in the broader industry.

Ignoring Qualitative Factors

Another major pitfall is getting completely lost in the numbers. It's easy to do. You get so focused on the spreadsheet that you forget about the crucial elements that don't fit neatly into a cell. These are often the real drivers of long-term success.

What am I talking about? Things like:

- Management Quality: Is the leadership team experienced, honest, and smart about where they put the company's money?

- Competitive Moat: Does the company have a durable advantage—like a monster brand or a network that’s impossible to replicate—that keeps competitors at bay?

- Industry Headwinds: Are there big technological shifts or regulatory changes on the horizon that could kneecap the business model?

A purely quantitative approach misses half the story. To make sure your estimates are solid and you're not overlooking huge risks, using an essential due diligence checklist that covers financial, legal, and market factors is a must. It keeps you honest.

A great company at a fair price is superior to a fair company at a great price. A deep understanding of the business itself is non-negotiable.

Ultimately, these qualitative insights are at the heart of good valuation. The entire process is just a practical application of the ideas behind what fundamental analysis is—it’s about getting to know the whole business, not just its financial reports. By blending rigorous number-crunching with a clear-eyed view of these "softer" factors, you can sidestep the common errors and land on a much more reliable estimate of a company's true worth.

Still Have Questions About Intrinsic Value?

Even after getting the hang of the main ideas, it’s totally normal to have some questions about how all this plays out in the real world. Let's dig into some of the most common ones I hear. Getting these sorted helps bridge that gap between just knowing the theory and actually using it to make smarter investment decisions.

Can a Company Actually Have a Negative Intrinsic Value?

Believe it or not, yes. It's rare, but it's theoretically possible. If a company is just bleeding cash year after year with no end in sight, and its debts dwarf its assets, the math could absolutely spit out a negative number.

Think of it this way: a business like that isn't just unprofitable, it's actively destroying value. For an investor, seeing a negative intrinsic value is a massive red flag. It's often a sign of a company circling the drain, and it’s a stock you’d want to avoid like the plague.

How Often Should I Recalculate This Stuff?

There's no single magic number here. A good starting point is to revisit your calculations quarterly, right after a company drops its latest earnings report. That's when you get a fresh flood of data on sales, profits, and cash flow to work with.

But don't just stick to a schedule. You absolutely need to run the numbers again anytime something major happens. This could be a huge acquisition, a scary new competitor popping up, a big pivot in company strategy, or even a macro-level shift like the Fed suddenly jacking up interest rates.

Is Intrinsic Value Only for "Value Stocks"?

It’s the bread and butter of value investing, for sure, but it’s just as critical when you're looking at high-flying growth stocks. The mindset is just a little different.

- With value stocks, you're hunting for a big gap—a market price that's way cheaper than your calculated intrinsic value.

- With growth stocks, the story is all about the future. A DCF analysis is your reality check to see if that sky-high stock price is even remotely justified by plausible growth down the road.

At the end of the day, it's about not overpaying. Estimating intrinsic value keeps your feet on the ground and your decisions rooted in financial reality, not just market hype. That discipline is what separates serious long-term investors from the crowd.

At Investogy, we use these same principles to analyze every stock in our real-money portfolio. Subscribe to our free weekly newsletter to see how we apply intrinsic value to make real investment decisions. Join Investogy for free.