A bear market, officially a decline of 20% or more from recent highs, often sparks fear and panic among investors. But for those with a plan, it represents one of the greatest wealth-building opportunities. Instead of retreating, savvy investors use downturns to acquire high-quality assets at discounted prices, setting the stage for significant long-term growth. This guide moves beyond generic advice to provide seven distinct, actionable bear market investing strategies, complete with real-world examples and practical implementation steps.

We will explore a range of tactics, from the disciplined consistency of Dollar-Cost Averaging to the strategic patience of Value Investing. You will learn how to identify defensive sectors that can weather economic storms and how to target high-quality growth companies when their valuations become attractive. We will also cover more advanced concepts, such as using short selling or inverse ETFs to potentially profit from falling prices, and the critical role of holding cash as a strategic tool for seizing opportunities.

Each strategy is designed to provide a clear framework for making informed decisions when market sentiment is at its lowest. Before diving into real-world applications of these strategies, consider utilizing tools like paper trading to practice and refine your approach risk-free and build confidence in navigating market downturns. This guide is designed to help you not only survive a downturn but to use it as a foundation for future financial success, transforming market volatility from a threat into a strategic advantage.

1. Dollar-Cost Averaging (DCA)

Dollar-cost averaging (DCA) is a disciplined and systematic investment strategy that removes emotion from the often-turbulent process of buying assets. Instead of trying to "time the market" by investing a lump sum at the perceived bottom, an investor commits to investing a fixed amount of money at regular intervals, such as weekly, bi-weekly, or monthly. This approach is one of the most effective bear market investing strategies because it reframes falling prices as an opportunity rather than a crisis.

During a bear market, your fixed investment amount automatically buys more shares of an asset when its price is low. As the market eventually recovers and prices rise, that same fixed amount buys fewer shares. This process can significantly lower your average cost per share over time, positioning your portfolio for amplified gains when the market turns bullish.

How DCA Thrives in a Downturn

The core strength of DCA lies in its ability to leverage volatility. Consider investors who consistently contributed to their 401(k) plans throughout the 2008-2009 financial crisis. While their account balances looked bleak in the short term, their regular contributions were purchasing stocks at deeply discounted prices. By 2012, those who stayed the course saw their portfolios recover and grow substantially, having built a strong foundation at the market’s low point.

Similarly, an investor who committed to a $500 monthly investment in an S&P 500 index fund during the dot-com crash (2000-2002) would have accumulated a large number of shares at depressed valuations. This disciplined approach would have resulted in powerful returns by the time the market peaked again in 2007. More recently, crypto investors who used DCA to buy Bitcoin during its 2022 downturn were well-positioned for the significant recovery in 2023.

Actionable Tips for Implementing DCA

To make this strategy work effectively, focus on automation and consistency.

- Set It and Forget It: Automate your investments. Schedule recurring transfers from your bank account to your brokerage account to invest on a specific day each month. This removes the temptation to pause contributions when fear is highest.

- Focus on Broad Market Funds: DCA works best with diversified assets like broad-market index funds (e.g., VTI, VOO) or ETFs. These assets are highly likely to recover with the overall market, reducing single-stock risk.

- Consider "Buying the Dip" Strategically: While standard DCA involves a fixed amount, some investors adopt a "DCA-plus" strategy. They might slightly increase their regular contribution amount after a significant market drop (e.g., a 10-15% decline) to capitalize further on lower prices.

- Annual Review: Revisit your DCA amount annually or after a significant change in income. Adjusting your contribution ensures your strategy aligns with your current financial situation and long-term goals.

2. Value Investing

Value investing is a time-honored philosophy centered on buying high-quality companies for less than their underlying worth. Pioneered by Benjamin Graham and famously practiced by Warren Buffett, this strategy involves identifying securities that are trading at a significant discount to their intrinsic value. A bear market is the ultimate hunting ground for value investors, as widespread fear and pessimism can cause even fundamentally sound businesses to become temporarily underpriced, creating exceptional bear market investing strategies for the patient investor.

Instead of getting caught up in market sentiment, a value investor acts like a business analyst, meticulously assessing a company's financial health, competitive position, and long-term prospects. The goal is to find durable businesses that the market has unfairly punished. By purchasing these assets at a discount, investors create a "margin of safety," which provides both downside protection and significant upside potential when the market eventually recognizes the company's true value.

How Value Investing Capitalizes on Fear

History is filled with examples of value investing shining brightest during downturns. During the 2008 financial crisis, Warren Buffett made multibillion-dollar investments in Goldman Sachs and Bank of America. While others were panicking, he saw fundamentally strong institutions trading at crisis-level prices and secured highly favorable terms. Similarly, during the sharp COVID-19 market crash in March 2020, Berkshire Hathaway deployed capital into various businesses, capitalizing on the momentary panic.

This approach isn't just for Wall Street titans. Benjamin Graham, the "father of value investing," built his fortune by patiently buying undervalued stocks during the Great Depression, a strategy that led to phenomenal long-term returns. The core principle remains the same: market downturns offer the rare chance to buy great companies "on sale." For a deeper dive into this philosophy, you can learn more about how to invest like Warren Buffett.

Actionable Tips for Implementing Value Investing

To apply this strategy effectively, you need a disciplined and analytical approach.

- Prioritize Financial Health: Focus on companies with strong balance sheets, specifically those with low debt-to-equity ratios. Financially sound businesses are better equipped to survive economic storms without diluting shareholder value.

- Identify a Durable Competitive Advantage: Look for businesses with a "moat," such as a powerful brand, network effects, or patent protection. This advantage allows them to protect their market share and profitability over the long term.

- Calculate Intrinsic Value: Don't just guess if a stock is cheap. Learn to calculate a company's intrinsic value using multiple methods, such as Discounted Cash Flow (DCF) analysis. Understanding essential financial formulas like NPV and IRR is crucial for building accurate valuation models.

- Keep Cash on the Sidelines: Maintain a cash reserve specifically for market downturns. This "dry powder" allows you to act decisively and purchase high-conviction assets when they become available at bargain prices.

3. Defensive Sector Rotation

Defensive sector rotation is a strategic portfolio adjustment that involves shifting investments toward sectors that have historically shown resilience during economic downturns. Rather than selling off assets in panic, this strategy reallocates capital to industries providing essential goods and services with stable demand. These typically include utilities, consumer staples, healthcare, and telecommunications, making this one of the most proactive bear market investing strategies for preserving capital.

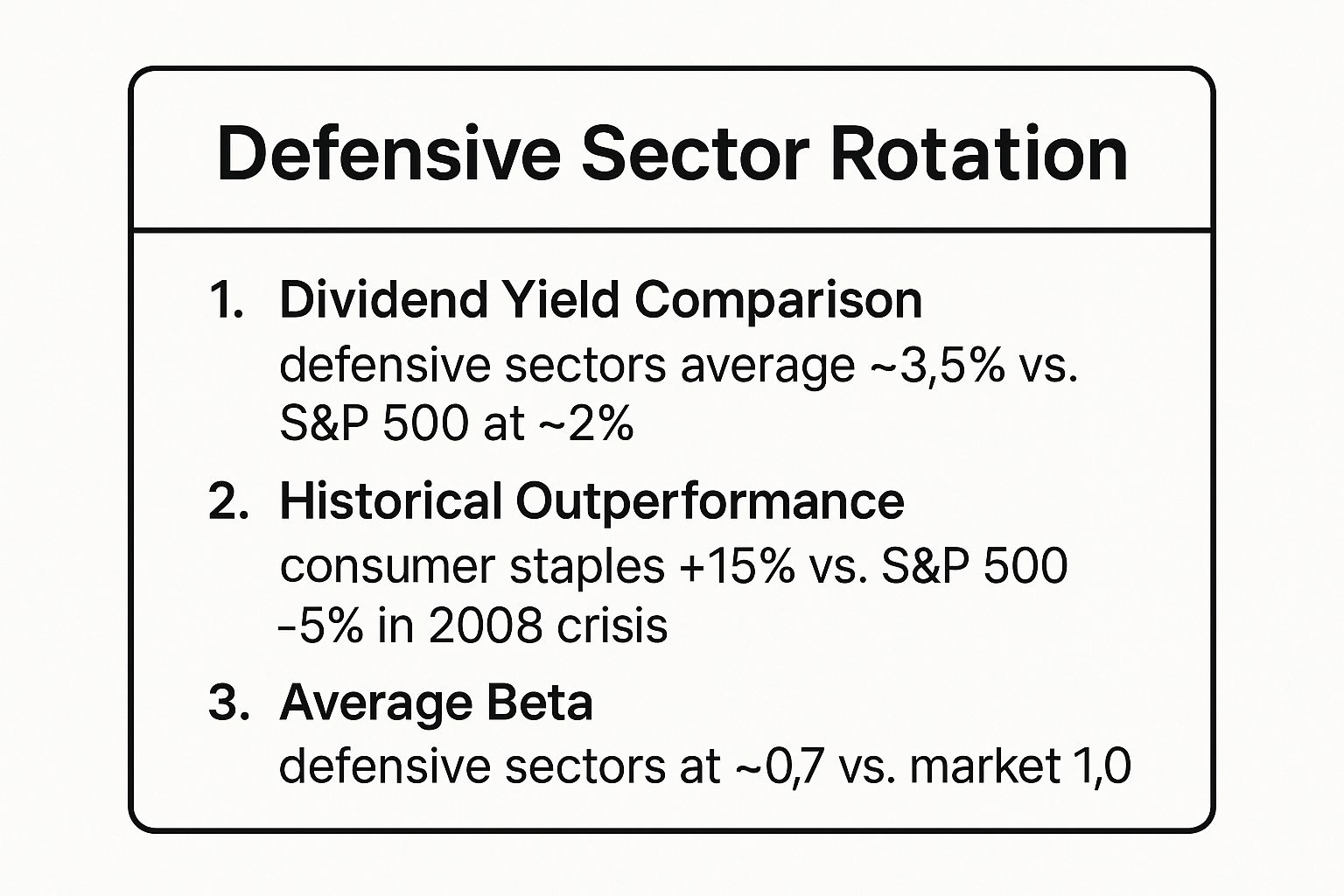

This infographic provides a quick reference on why defensive sectors can be a portfolio stabilizer during market volatility.

The data clearly illustrates that these sectors not only tend to have lower volatility (beta) but also have a history of outperformance and higher dividend yields during economic stress.

How Defensive Rotation Thrives in a Downturn

The strength of this strategy lies in its focus on non-cyclical businesses. While consumers may delay buying a new car or a luxury watch during a recession, they will continue to pay for electricity, buy groceries, and seek medical care. This inelastic demand provides a floor for the revenues and earnings of companies in defensive sectors, making their stock prices less susceptible to wild swings.

For example, during the 2008 financial crisis, the S&P 500 Consumer Staples sector outperformed the broader S&P 500 by approximately 15%, showcasing its capital preservation qualities. Similarly, during the initial COVID-19 market crash in early 2020, the healthcare sector demonstrated significant resilience as demand for its products and services surged. During the dot-com crash of 2000-2002, while technology stocks plummeted, utility stocks delivered positive returns, shielding investor portfolios from the worst of the drawdown.

Actionable Tips for Implementing Defensive Rotation

To execute this strategy effectively, focus on careful selection and timing.

- Use ETFs for Diversification: Instead of picking individual stocks, consider using defensive sector ETFs like the Consumer Staples Select Sector SPDR Fund (XLP) or the Health Care Select Sector SPDR Fund (XLV). This provides instant diversification across the industry and reduces single-company risk.

- Analyze Dividend Sustainability: Defensive stocks are often prized for their dividends. Look beyond the current yield and examine a company's dividend payout ratio and history of dividend payments to ensure they are sustainable, especially during a recession.

- Monitor the Interest Rate Environment: Utility stocks, in particular, can be sensitive to interest rate changes. In a high or rising rate environment, their steady dividends may become less attractive compared to the yields on lower-risk bonds, which can put pressure on their stock prices.

- Plan Your Re-Entry: Defensive rotation is not a permanent move. The goal is to weather the storm and then rotate back into more growth-oriented sectors as the economy shows signs of recovery. For a deeper understanding of adjusting your portfolio, you can learn more about the principles of portfolio rebalancing.

4. Short Selling and Inverse ETFs

While most investment strategies focus on profiting from rising asset prices, short selling and inverse ETFs are advanced bear market investing strategies designed to generate returns when the market is falling. Short selling involves borrowing a stock, selling it at its current price, and then buying it back later at a lower price to return to the lender, pocketing the difference. Inverse ETFs, a more accessible alternative, are funds designed to move in the opposite direction of their underlying index, such as the S&P 500.

These approaches allow savvy investors to not only hedge their long positions but also actively profit from a downturn. Instead of simply trying to preserve capital, these tools turn bear market declines into direct opportunities for growth. However, they come with significantly higher risks, as potential losses from short selling are theoretically unlimited if the stock price rises instead of falls.

How Shorting Thrives in a Downturn

The power of these strategies was famously demonstrated during the 2008 financial crisis. Michael Burry of Scion Capital used credit default swaps to effectively "short" the subprime mortgage market, leading to immense profits for his firm when the housing bubble burst. Similarly, hedge fund manager John Paulson made billions by shorting subprime mortgage-backed securities. These are extreme examples, but they highlight the potential of profiting from correctly identifying overvalued assets before a correction.

During the dot-com bubble burst (2000-2002), short sellers like Jim Chanos of Kynikos Associates earned fortunes by betting against fraudulent or wildly overvalued tech companies. More recently, during the 2022 bear market, inverse ETFs like the ProShares Short S&P500 (SH) and the ProShares Short QQQ (PSQ) delivered positive returns while their underlying indices, the S&P 500 and Nasdaq-100, saw significant declines.

Actionable Tips for Implementing Short Strategies

These are not "set it and forget it" strategies and require active management and a deep understanding of the risks involved.

- Start with Inverse ETFs: For investors new to shorting, inverse ETFs are a simpler and less risky entry point. They don't require a margin account or borrowing shares, and losses are capped at the initial investment amount.

- Use Strict Stop-Loss Orders: When short selling a stock directly, a stop-loss order is non-negotiable. This automatically buys back the stock if it rises to a predetermined price, capping your potential losses.

- Keep Position Sizes Small: Due to the high-risk nature of these strategies, allocate only a small portion of your portfolio to them. This ensures a mis-timed bet doesn't cripple your overall financial health.

- Monitor Borrowing Costs: For direct short selling, you must pay interest on the shares you borrow. These "borrow fees" can become very expensive, especially for heavily shorted stocks, and can eat into potential profits.

5. Quality Growth at Reasonable Prices (GARP)

Quality Growth at a Reasonable Price (GARP) is a sophisticated hybrid strategy that blends the best of both growth and value investing. Instead of chasing high-flying growth stocks at any price or buying deeply distressed "cigar-butt" value stocks, GARP investors seek a sweet spot: well-managed, growing companies whose stock prices have been unfairly punished. This makes it one of the most effective bear market investing strategies, as widespread pessimism often pushes excellent companies into the "reasonable price" category.

The GARP approach, famously championed by legendary investor Peter Lynch, prioritizes companies with consistent earnings growth, strong returns on equity, sustainable competitive advantages, and competent management. During a downturn, the market often fails to distinguish between high-quality businesses experiencing temporary headwinds and fundamentally flawed companies. A GARP investor uses this confusion to acquire shares in premier businesses at a significant discount to their intrinsic value.

How GARP Thrives in a Downturn

The power of GARP is its ability to find bargains among market leaders. During the 2008-2009 financial crisis, companies like Microsoft and Apple saw their stock prices plummet alongside the rest of the market, despite their fortress-like balance sheets and dominant market positions. Investors who recognized that their long-term growth stories were intact could acquire shares at price-to-earnings (P/E) ratios that were unthinkably low just a year earlier, leading to immense gains in the subsequent recovery.

More recently, the 2022 tech bear market punished nearly all growth stocks. Amazon's stock fell dramatically as growth expectations were reset post-pandemic. A GARP investor would have analyzed its enduring dominance in e-commerce and cloud computing (AWS), recognized its long-term potential, and viewed the lower valuation as a prime buying opportunity. Similarly, Peter Lynch’s success at the Fidelity Magellan Fund was built on finding companies like Dunkin' Donuts and The Home Depot during periods when the market had temporarily soured on their prospects.

Actionable Tips for Implementing GARP

To apply this strategy, you must be both a business analyst and a disciplined value investor.

- Look for Consistent Profitability: Focus on companies with a track record of high Return on Equity (ROE), ideally consistently above 15%. This indicates an efficient, well-run business that generates strong profits from its assets.

- Analyze Competitive Positioning: Identify companies with durable competitive advantages or "moats." Does the company have a powerful brand, network effects, or patents that protect it from competition? Analyze its market share trends to ensure it's a leader.

- Use the PEG Ratio: The Price/Earnings to Growth (PEG) ratio is a classic GARP metric. It compares a company's P/E ratio to its earnings growth rate. A PEG ratio around 1.0 is often considered a good indicator of a reasonably priced growth stock.

- Focus on Free Cash Flow: Beyond earnings, analyze a company's ability to generate free cash flow. This is the actual cash a business produces, which can be used to pay dividends, buy back shares, or reinvest for future growth, making it a critical sign of financial health.

6. Cash and Cash Equivalents Strategy

Holding a higher-than-normal cash position is a powerful defensive move that prioritizes capital preservation and strategic flexibility during a downturn. This approach involves keeping funds in highly liquid, low-risk instruments like high-yield savings accounts, money market funds, or short-term Treasury bills. Rather than viewing it as "sitting on the sidelines," this is an active strategy that positions you to act decisively when investment opportunities arise from market panic. This is one of the most effective bear market investing strategies for investors focused on risk management and opportunistic buying.

During a bear market, cash is king because its value doesn't fall with the market. While others are forced to sell assets at a loss to cover expenses or are too fearful to invest, your cash position gives you "dry powder." This liquidity allows you to purchase quality assets at significant discounts, effectively turning a market crisis into a generational buying opportunity.

How Holding Cash Thrives in a Downturn

The core strength of this strategy lies in its dual role as a shield and a spear: it protects your capital from drawdowns while preparing you for a future offensive. A prime example is Berkshire Hathaway, which famously maintained a cash hoard of over $120 billion leading up to the COVID-19 crash in early 2020. This massive liquidity allowed Warren Buffett to deploy capital into strategic investments when fear was at its peak.

Similarly, investors who shifted a portion of their portfolio to cash in late 2021 or early 2022 were insulated from the worst of the 2022 market decline. As high-quality stocks and funds hit multi-year lows, these investors had the capital ready to buy at deeply discounted prices, setting themselves up for a powerful rebound. During the height of the March 2020 volatility, money market funds saw record inflows as investors flocked to safety, preserving capital that could be redeployed just weeks later at the market bottom.

Actionable Tips for Implementing a Cash Strategy

To use this strategy effectively, you need a disciplined plan for both holding and deploying your cash.

- Define Your "Dry Powder" Fund: Determine a specific percentage of your portfolio to allocate to cash, separate from your standard 6-12 month emergency fund. This is your dedicated "opportunity fund."

- Use High-Yield, Secure Instruments: Park your cash in FDIC-insured high-yield savings accounts (up to $250,000) or Treasury-backed money market funds to earn some return while waiting. For inflation protection, consider short-term Treasury bills or I-bonds.

- Set Predetermined Re-entry Criteria: Don't try to time the exact bottom. Instead, establish clear rules for when you will start deploying cash. For example, you might decide to invest 25% of your cash after the S&P 500 has fallen 20%, another 25% after a 30% fall, and so on.

- Avoid "Cash Drag" Indefinitely: The biggest risk of a cash strategy is missing the recovery. Sticking to your pre-defined deployment plan is crucial to ensure your cash doesn't sit on the sidelines for too long and miss the subsequent bull run.

7. Dividend Growth Investing

Dividend growth investing is a powerful strategy focused on acquiring stocks of companies with a long and consistent history of increasing their dividend payments. This approach is not about chasing the highest yields, but rather identifying financially sound businesses that reward shareholders with a growing stream of income. This discipline makes it one of the most resilient bear market investing strategies, as it provides both a psychological and financial cushion during downturns.

While capital appreciation is a goal for any investor, dividend growth stocks offer a tangible return in the form of cash payments, regardless of the stock price's daily fluctuations. This reliable income can be a source of stability when portfolio values are declining. Furthermore, a commitment to consistently raising dividends often signals strong fundamentals, disciplined management, and confidence in future earnings, qualities that are highly attractive during periods of market uncertainty.

How Dividend Growth Thrives in a Downturn

The strength of this strategy lies in its dual benefit of income and defensive positioning. Dividend-paying companies, particularly "Dividend Aristocrats" (S&P 500 companies with 25+ consecutive years of dividend increases), often exhibit lower volatility than the broader market. Their established business models and stable cash flows allow them to weather economic storms more effectively.

For instance, during the 2008-2009 financial crisis, stalwarts like Johnson & Johnson and Coca-Cola continued their multi-decade streaks of dividend increases, providing investors with a predictable income stream even as the market crashed. Similarly, data shows that dividend-focused ETFs often outperformed the S&P 500 during the dot-com bust of 2000-2002, offering superior downside protection. This historical resilience makes the strategy a cornerstone for conservative investors.

Actionable Tips for Implementing Dividend Growth

To effectively build a dividend growth portfolio for a bear market, focus on quality and sustainability.

- Analyze the Payout Ratio: Target companies with a payout ratio below 60%. A lower ratio indicates that the dividend is well-covered by earnings and has room to grow, making it more sustainable during a recession.

- Focus on Free Cash Flow: A healthy and growing free cash flow is essential for funding future dividend increases. Analyze a company's cash flow statements to ensure it generates more than enough cash to cover its obligations and reward shareholders.

- Reinvest Dividends for Compounding: Use a Dividend Reinvestment Plan (DRIP) to automatically reinvest your dividend payments. During a bear market, this strategy acts like dollar-cost averaging, as your reinvested dividends buy more shares at lower prices, accelerating compound growth when the market recovers.

- Diversify Across Sectors: Avoid concentrating in a single industry. Build a portfolio of dividend growers across various sectors like consumer staples, healthcare, utilities, and industrials to mitigate sector-specific risks. For those just starting, learning the fundamentals is key. You can explore a complete guide to dividend investing for beginners on investogy.com to build a solid foundation.

Bear Market Investing Strategies Comparison

| Strategy | Implementation Complexity 🔄 | Resource Requirements 💡 | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Dollar-Cost Averaging (DCA) | Low 🔄 | Low (steady cash flow) 💡 | Reduced impact of volatility; steady growth 📊 | Long-term investors looking for disciplined investing | Automation reduces emotional decisions ⭐ |

| Value Investing | High 🔄 | High (research & analysis) 💡 | Potential for strong returns after recovery 📊 | Patient investors targeting undervalued stocks | Margin of safety; quality company focus ⭐ |

| Defensive Sector Rotation | Medium 🔄 | Medium (active portfolio management) 💡 | Portfolio stability during downturns 📊 | Risk-averse investors seeking defensive exposure | Stable dividends and essential services ⭐ |

| Short Selling & Inverse ETFs | Very High 🔄 | High (margin, borrowing costs) 💡 | Profits from market decline; hedging 📊 | Sophisticated investors hedging or speculating | Potential for significant gains in bear markets ⭐ |

| Quality Growth at Reasonable Prices (GARP) | High 🔄 | High (in-depth analysis) 💡 | Balanced growth and downside protection 📊 | Investors seeking growth with value discipline | Combines growth with value advantages ⭐ |

| Cash and Cash Equivalents | Low 🔄 | Low (liquid assets) 💡 | Capital preservation; liquidity for opportunities 📊 | Defensive investors prioritizing safety and flexibility | Eliminates downside risk; fast redeployment ⚡ |

| Dividend Growth Investing | Medium 🔄 | Medium (analysis of dividend stability) 💡 | Steady income with potential inflation protection 📊 | Income-focused investors during volatile markets | Consistent income; psychological benefit ⭐ |

Building a Resilient Portfolio for All Seasons

Navigating the turbulent waters of a downturn is less about finding a single, magical formula and more about assembling a robust toolkit of bear market investing strategies. The approaches we've detailed, from the systematic discipline of Dollar-Cost Averaging to the opportunistic patience of Value Investing, are not mutually exclusive. Instead, they represent a spectrum of tactics you can blend to construct a portfolio that is not just defensive but also opportunistic.

The true challenge of a bear market is psychological. Fear and panic are powerful forces that can derail even the most well-intentioned investor. By internalizing these strategies before a downturn hits, you replace emotional reactions with a pre-defined, logical plan of action. This mental shift from fear to calculated opportunism is the single most important factor in turning market adversity into a long-term advantage.

Synthesizing Your Strategy for Success

The most resilient portfolios are rarely built on one pillar alone. Consider how these strategies can complement one another to create a more dynamic and effective plan:

- Combine DCA with GARP: Use Dollar-Cost Averaging to systematically buy into high-quality companies whose growth prospects remain strong, even as their stock prices have become more reasonable. This methodical approach removes the pressure of timing the bottom perfectly.

- Pair Value Investing with Dividend Growth: Hunt for undervalued, blue-chip companies that not only offer a margin of safety but also boast a long history of increasing their dividend payments. This creates a powerful dual-engine for returns: potential capital appreciation and a reliable, growing income stream to reinvest or live on.

- Integrate Defensive Sectors with a Cash Reserve: Rotate a portion of your portfolio into non-cyclical sectors like consumer staples and healthcare for stability, while holding a strategic cash position. This cash isn't just a safety net; it's your "dry powder," ready to be deployed into high-conviction ideas when valuations become undeniably attractive.

Ultimately, the goal is not to avoid losses entirely, which is an unrealistic expectation. The goal is to mitigate downside, stay invested, and strategically position your portfolio to capture the upside of the inevitable recovery. Every bear market in history has been followed by a bull market, and the seeds of future wealth are often sown during periods of maximum pessimism.

Your Actionable Path Forward

Translating theory into action is what separates successful investors from the crowd. Your immediate next steps should be to review your current portfolio and financial plan with these concepts in mind. Ask yourself critical questions: Is my asset allocation aligned with my risk tolerance? Do I have a watchlist of quality companies I'd love to own at lower prices? Is my cash position adequate to seize opportunities without needing to sell assets at a loss?

Furthermore, as you execute these strategies, such as selling certain positions to rotate into defensive sectors or harvesting losses for tax purposes, a crucial part of long-term resilience involves understanding capital gains tax implications. Proactive tax management can significantly enhance your net returns, ensuring that more of your hard-earned gains stay in your portfolio to compound over time. By mastering these powerful bear market investing strategies, you are not just surviving the storm; you are building a stronger, more resilient foundation for all seasons to come.

Ready to see these principles in action? Follow along as we transparently manage a real-money portfolio through every market cycle at Investogy. Our newsletter provides the in-depth research and unfiltered analysis you need to build conviction and navigate the markets with confidence. Join Investogy today to transform market theory into a practical, real-world investing edge.