Getting started with investing really just boils down to a few manageable decisions: what are you investing for, how much can you put in, and which account should you use? If you can get clear on these three things, you've cut through the noise. You'll have a simple, actionable plan ready to go.

Your First Practical Steps In Investing

Diving into the world of investing can feel like trying to climb a mountain. But the reality? It’s much less intimidating. Forget about specific stocks or what the market is doing for a moment. Your journey starts with a few basic questions about your own life and financial situation.

This isn’t about building complicated financial models; it’s about finding clarity and purpose. The most successful investors I know have one thing in common: they know exactly why they are investing. Your goals are the compass that will guide every single choice you make, from the type of account you open to the assets you buy.

Think about what you're trying to achieve and when you'll need the money.

- Short-Term Goals (1-5 years): Are you saving for a down payment, a new car, or that dream trip to Italy? For these goals, you'll want to be more conservative. You simply can't afford a big market drop right before you need to cash out.

- Mid-Term Goals (5-10 years): This is the territory of saving for a child’s future education or socking away capital to start a business. With a bit more time on your side, you can afford to take on more calculated risk for the chance at higher returns.

- Long-Term Goals (10+ years): Retirement is the classic example here. When you have decades to let your money work for you, you can embrace strategies with higher growth potential. You'll have plenty of time to ride out the inevitable market ups and downs.

Choosing The Right Investment Account

Once you know your destination, you can pick the right vehicle to get you there. Not all investment accounts are the same. They're designed for different purposes, especially when it comes to taxes and when you can access your money.

For example, a 401(k) through your job is a fantastic tool for retirement, especially if your employer offers a match—that’s literally free money. Don't leave it on the table. An Individual Retirement Account (IRA) is one you open on your own, giving you similar tax benefits but often a wider range of investment choices. These accounts are built for the long haul, and you'll usually face penalties if you try to withdraw funds early.

For everything else, there’s the standard taxable brokerage account. This is your all-purpose workhorse. It offers total flexibility; you can invest in just about anything and pull your money out whenever you want, for any reason. This makes it perfect for non-retirement goals, like that house down payment. The trade-off? You’ll pay taxes on your investment gains.

For a great breakdown of these options, check out this detailed how to start investing guide.

Key Takeaway: Match your account to your goal. Use tax-advantaged accounts like a 401(k) or IRA for retirement. For any goals you need to fund before you retire, a taxable brokerage account is your best bet.

Determining How Much To Invest

Let's clear up a common myth: you don't need a fortune to start. In fact, consistency beats a large initial sum every time. Thanks to fractional shares, most modern brokerage platforms let you get started with as little as $5 or $10.

The smartest thing you can do is put your contributions on autopilot. Figure out an amount you can comfortably set aside each month—whether it's $50 or $500—and schedule an automatic transfer. This "pay yourself first" strategy removes emotion from the equation and builds an incredibly powerful habit over time.

For a deeper dive into these core concepts, this comprehensive investing for beginners guide is an excellent resource.

Getting your first investments off the ground is really about making a few key decisions upfront. I've found it helps to think of it like a simple checklist.

Your Initial Investing Checklist

| Your Decision | What It Involves | A Smart First Move |

|---|---|---|

| Defining Your "Why" | Setting clear financial goals (e.g., retirement in 30 years, house down payment in 5). | Start with your biggest long-term goal: retirement. It's the one we all share. |

| Choosing Your Account | Selecting a 401(k), IRA, or taxable brokerage account based on your goals. | If your employer offers a 401(k) match, start there. It's an instant return on your money. |

| Deciding How Much | Figuring out a consistent, affordable amount to contribute regularly. | Pick a small, comfortable amount (even $50/month) and set up automatic transfers. |

Once you've worked through this checklist, you've done the heavy lifting. By defining your purpose, picking the right account, and committing to a consistent plan, you've already conquered the hardest part of learning how to invest.

Why Starting Early Is Your Secret Weapon

When you're first figuring out how to invest, it's natural to get fixated on finding the "perfect" stock or trying to time the market just right. But I'll let you in on a secret I've learned from years of experience: the most powerful tool you have isn't a complex trading strategy or a hot stock tip. It's time.

The real magic behind building wealth is putting your money to work as soon as you possibly can and just letting it grow.

This power boils down to one critical concept: compounding. I like to think of it as a snowball rolling down a huge hill. It starts off small, maybe just a handful of snow. But as it rolls, it picks up more snow, getting bigger and bigger at an ever-increasing speed. Your money works the exact same way. The returns your investments generate start earning their own returns. This creates a powerful growth cycle that can turn small, consistent contributions into a serious fortune over the long haul.

This isn't just some feel-good theory; it's a mathematical reality. Understanding this is one of the most important things for your long-term success. For instance, the U.S. stock market has a long history of strong growth over extended periods, which really highlights the benefits of getting in the game. You can dig into the numbers and see the data on historical investment returns for yourself.

The Real Cost Of Waiting

Putting off investing can be shockingly expensive. Seriously. Even waiting just a few years can create a massive gap in your final portfolio value, forcing you to sock away way more money later on just to try and catch up.

Let's walk through a real-world scenario to see why procrastination is the absolute enemy of wealth.

Imagine two friends, Alex and Ben. They both plan to retire at age 65.

- Alex starts investing at 25. She puts $300 a month into her portfolio and earns an average annual return of 8%.

- Ben waits just five years and starts at 30. He invests the same $300 per month and earns the same 8% average return.

By the time they both hit 65, the difference is staggering. Alex will have contributed a total of $144,000, and her portfolio will have ballooned to roughly $930,000. Ben, who started just a little later, will have put in $126,000, but his portfolio will only be worth around $620,000.

That five-year delay ended up costing Ben over $300,000 in potential growth.

The lesson is crystal clear: The amount of time your money is invested is often far more important than the amount you invest. Starting small but early almost always beats starting big but late.

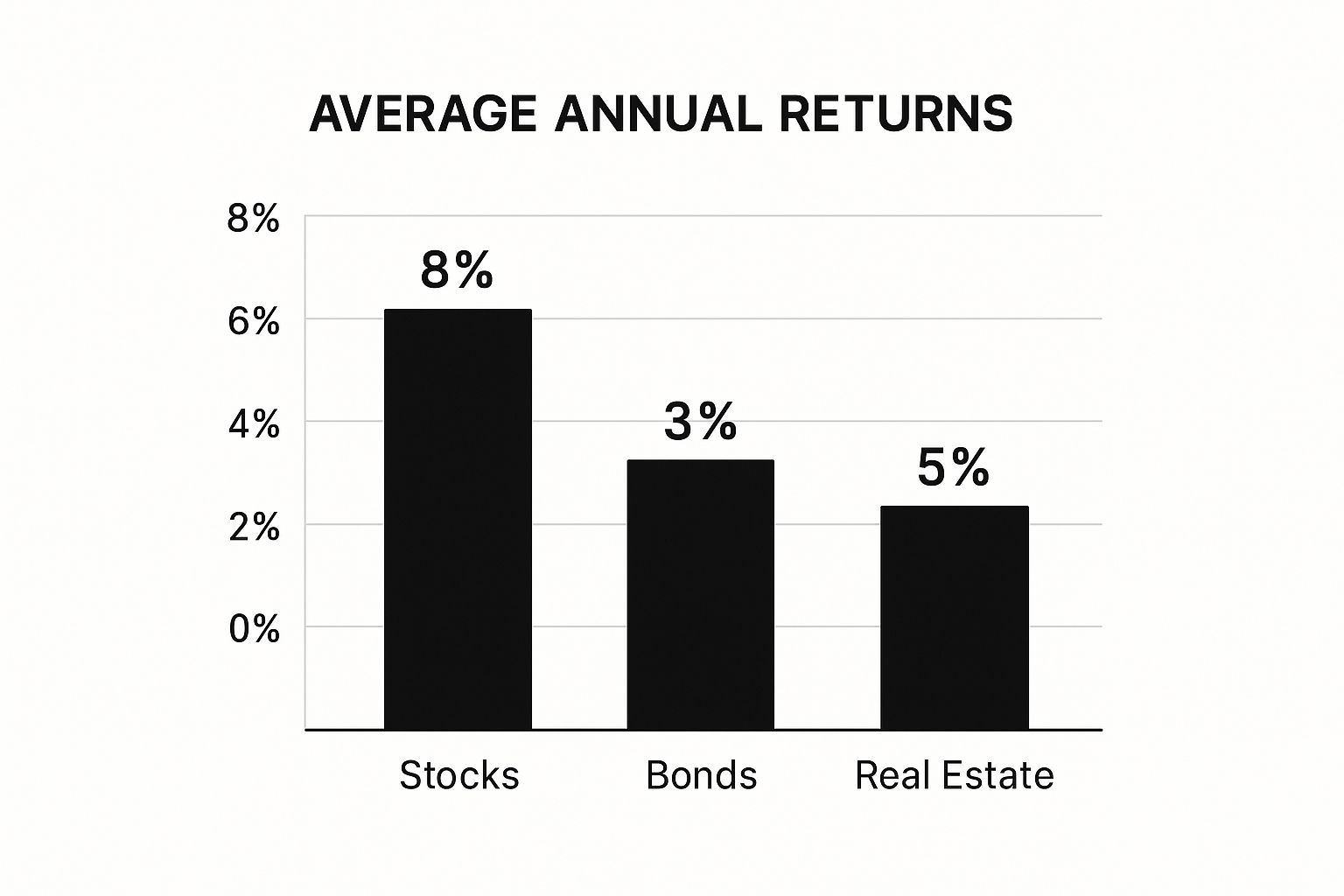

Visualizing Your Potential Returns

It helps to see where the growth actually comes from. Different types of investments, like stocks and bonds, have different levels of risk and potential reward. This chart gives you a quick look at the historical average annual returns for a few major asset types so you can get a feel for their long-term potential.

As you can see, stocks have historically delivered the highest potential for growth, which is why they're a foundational piece of most long-term investment plans.

Now, this doesn't mean you need to feel pressured to dump a huge chunk of cash into the market right away. The key takeaway is simple: the "best time" to start investing wasn't yesterday—it's right now. By putting your money to work, no matter how small the amount, you're giving it the maximum possible runway to compound and grow. This is the single greatest advantage you have as a new investor, and it’s one you can only use by taking action today.

Building Your First Investment Portfolio

Alright, your account is funded and ready to go. Now for the exciting part: deciding what to actually buy. This is the moment where a lot of new investors get analysis paralysis, picturing themselves drowning in complex charts and annual reports.

Let's ditch that stress. Building your first portfolio isn't about becoming a Wall Street guru overnight. It's more like putting together a well-balanced meal—you need a few different food groups that work together for energy, growth, and stability. An investment portfolio is no different.

Your Core Investment Options

For most folks starting out, the entire universe of investing can be boiled down to a few key building blocks. Let's break them down in plain English.

-

Stocks (Equities): When you buy a stock, you're buying a tiny slice of a public company, like Apple or Amazon. If the company thrives and its profits climb, your slice of the pie becomes more valuable. Stocks are the growth engine of your portfolio, offering the highest potential for long-term gains but also the most volatility (price swings).

-

Bonds (Fixed Income): Think of buying a bond as lending money to a government or a corporation. In exchange, they promise to pay you interest over a set period and then give you your original money back. Bonds are the shock absorbers. They're generally safer and less volatile than stocks, providing stability and predictable income to help cushion your portfolio during market downturns.

These two asset classes are the bedrock of nearly every investment strategy out there. The real challenge for a beginner isn't trying to pick the perfect stock or bond. It's finding an easy way to own a whole bunch of them at once.

Key Insight: Here's a dose of reality. Less than 10% of professional fund managers consistently beat the market's average performance over a 15-year period. This stat alone shows why trying to pick individual winners is an incredibly tall order, even for the pros.

The Beginner's Best Friend: Index Funds

Instead of searching for a needle in a haystack, what if you could just buy the entire haystack? That's the simple magic behind mutual funds and exchange-traded funds (ETFs). Both are essentially baskets that hold dozens, hundreds, or even thousands of individual stocks and bonds.

Mutual funds are professionally managed pools of money. You buy in, and a manager handles the investments. They're priced once a day after the market closes.

ETFs are similar, but they trade on stock exchanges just like individual stocks. Their prices fluctuate all day long, and they've become wildly popular for their low costs and flexibility.

For most beginners, the simplest and most powerful way to get started is with low-cost index funds, which can be either mutual funds or ETFs.

An index fund doesn't try to outsmart the market. Its only job is to match the performance of a market index, like the famous S&P 500 (which tracks 500 of the largest U.S. companies).

When you buy one share of an S&P 500 index fund, you instantly own a small piece of all 500 of those businesses. This gives you massive diversification with a single click. You're no longer betting on one company—you're betting on the long-term growth of the American economy as a whole.

This strategy strips away the guesswork and high fees. It's a proven, no-fuss approach to building wealth over time. If you want to dive deeper into spreading out your investments, our guide on how to diversify an investment portfolio has you covered.

A Simple, Practical Starter Portfolio

So, what does this look like in the real world? For a younger investor with decades to go, a classic, effective setup could be this simple:

- 70% in a U.S. Total Stock Market Index Fund: This gives you a piece of thousands of U.S. companies, from the giants down to the small guys.

- 20% in an International Stock Market Index Fund: You don't want all your eggs in one country's basket. This adds global diversification from developed and emerging markets.

- 10% in a Total Bond Market Index Fund: This small slice of bonds is your portfolio's stabilizer, helping to smooth out the inevitable bumps in the road.

This "three-fund portfolio" is famous for a reason: it's simple, incredibly low-cost, and highly effective at capturing market returns from around the globe. You can easily build it with ETFs from major players like Vanguard, Fidelity, or Charles Schwab. It's the perfect blueprint for getting started without getting overwhelmed.

So, you’ve wrapped your head around index funds. It's a huge step. It’s also tempting to stop there, maybe with a fund that tracks the US market. After all, it’s home to some of the world’s biggest and most dominant companies.

But here’s something I’ve learned over the years: a truly solid portfolio rarely stays within its own zip code. If you limit yourself to just one country's economy—even one as massive as America's—you're leaving a powerful tool on the table.

Investing internationally isn't about chasing some exotic, high-risk stock in a far-flung market. It’s a smart, strategic move to build a more stable portfolio. Different economies around the world don't always move in lockstep. When the US market is hitting a rough patch, markets in Europe or Asia might be doing just fine, and vice versa. This lack of perfect correlation is your friend.

By owning a piece of the global economy, you can seriously smooth out the bumps. Growth in one region can help cushion a temporary dip in another, leading to much more consistent returns over the long haul. It's probably the single easiest way to lower your portfolio's overall volatility without giving up on growth.

Why Global Diversification Really Matters

Imagine building a sports team. You could stack your roster with nothing but all-star quarterbacks. Sounds amazing, right? But you'd get crushed in a real game. You need players in different positions to handle whatever gets thrown at you.

International stocks are like those other players on your team. They give your portfolio more ways to win, especially when your star quarterback (the US market) is having an off day.

This isn't just some abstract theory—the numbers back it up. For new investors, global diversification is a fantastic way to manage risk, especially when the world economy gets choppy. Just look at the MSCI Emerging Markets (EM) Index, which tracks countries like China and India. It has seen long stretches where it outperformed the U.S. S&P 500, particularly during periods of economic stress. You can see how these global trends play out for yourself. It really drives home why having that global exposure is so important for long-term balance.

How to Get Global Exposure Without the Headache

Years ago, investing overseas was a real pain. It was complicated, expensive, and definitely not for beginners. Thankfully, that's ancient history. You don’t need to deal with foreign bank accounts or become an expert on the Tokyo Stock Exchange.

The simplest way is with the tools you're already getting to know: low-cost international index funds and ETFs.

Here are the main paths you can take:

- Total International Stock Index Funds: This is the "easy button." With a single fund, you instantly own thousands of stocks from developed nations (think Germany, Japan) and emerging markets (like Brazil, South Korea). It's a one-and-done solution.

- Region-Specific ETFs: If you want a bit more control, you could buy an ETF focused on a specific part of the world, like a "Europe Stock ETF" or a "Pacific Region ETF." This lets you lean into areas you think have particularly strong growth potential.

For most people just starting out, a single, total international index fund is the perfect choice. It gives you instant global diversification with zero fuss.

A Practical Tip: As you build your portfolio, a good rule of thumb is to put somewhere between 20% and 40% of your total stock allocation into international funds. This gives you meaningful diversification without making things overly complex.

A Quick Word on "Alternatives"

Beyond stocks and bonds, there's a whole other world of investing that's slowly opening up to everyday folks: alternative assets. This is a catch-all term for investments that don't fit into the usual buckets. We're talking about things like real estate, commodities (gold, oil), and even private equity—investing in companies before they're available on the stock market.

Historically, assets like private equity were a playground for the super-rich and institutional investors. But new platforms and specialized funds are changing the game, allowing regular investors to get a small slice of the pie. These investments are generally higher-risk and you can't sell them as easily, but they often move independently of the stock market, which can be great for diversification.

For now, as a beginner, just file this under "good to know for later." Your primary focus should be on building a rock-solid foundation with US and international stock and bond index funds. Once you've got that down and your portfolio has grown, you can start exploring whether a small allocation to alternatives makes sense for you.

How to Manage Your Investments Without Stress

So, you’ve built your portfolio. Now what? This is where many new investors get stuck, and they usually fall into one of two traps. They either become obsessive, checking their accounts with every market hiccup, or they completely neglect their investments for years, just hoping for the best.

The smart path, as with most things, is somewhere in the middle. Managing your investments isn't a daily grind. It's about setting up a simple, sustainable routine to make sure you're still heading toward your long-term goals. This is about building good habits that protect your money, not about reacting to every breathless news report.

Taming the Urge to Constantly Check

Your phone buzzes. The market just dropped 2%. If your first instinct is to log in and assess the damage, you're setting yourself up for a world of anxiety and bad, emotional decisions.

Let's be real: checking your portfolio every day is more likely to hurt your returns than help them. The market's short-term gyrations are mostly random noise. Acting on that noise—panic-selling during a dip or buying out of FOMO—is precisely how people sabotage their own financial progress.

So, how often should you actually look?

- For long-term investors: A quarterly check-in is plenty. Seriously. Once every three months, set aside 30 minutes to review your holdings.

- What to check for: Forget the daily performance numbers. Instead, confirm your automatic contributions are happening and see if your asset allocation has drifted too far from your original plan. That’s it.

This disciplined, hands-off method requires trusting the strategy you put in place. You built a diversified, long-term portfolio for a reason. Now, give it the time and space to do its job.

Mastering the Psychology of Market Dips

Market downturns are a matter of "when," not "if." They are a normal, even healthy, part of the investing cycle. The S&P 500, a benchmark for the U.S. market, goes through a correction—a drop of 10% or more—about once every two years, on average.

Knowing this fact is one thing. Living through it is another beast entirely. When you see your account balance shrink, your brain’s fight-or-flight response can kick in, screaming at you to sell everything and stop the pain. This is where the real work of investing is done: in managing your own behavior.

Key Insight: Your biggest enemy as an investor isn't a down market; it's your own emotional reaction to it. The most successful investors aren't market wizards who can predict the future. They are the ones who stay disciplined when things get scary.

Instead of panicking during a dip, try to reframe your thinking. When the market is down, all your favorite investments are effectively on sale. Those regular, automated contributions you set up are now buying more shares for the same amount of money. This can seriously accelerate your growth when the market inevitably recovers.

The Simple Power of Automation and Rebalancing

Discipline is a lot easier when you don't have to rely purely on willpower. Two straightforward habits can keep your portfolio on the right track with minimal effort: automating your contributions and periodically rebalancing.

Automating your investments is the single most effective way to stay consistent. Set up automatic transfers from your bank to your brokerage account every single month. This way, you're always investing, whether the market is up, down, or sideways. This strategy, called dollar-cost averaging, helps smooth out your average purchase price over time.

Rebalancing is just the fancy term for hitting the "reset" button on your portfolio to bring it back to your target asset mix. Over time, some investments will naturally grow faster than others. For instance, a great year in the stock market could turn your intended 70/30 stock-to-bond portfolio into an 80/20 mix, making it riskier than you're comfortable with.

To rebalance, you simply sell a bit of the asset that has outperformed and use that money to buy more of the one that has underperformed. This simple action forces you to buy low and sell high—the fundamental principle of smart investing. You don’t need to do this constantly; for most people, once a year is more than enough. If you want to dive deeper, you might find these 9 portfolio management best practices helpful for keeping your strategy on course.

By creating a simple management routine, you shift from being a reactive speculator to a disciplined, long-term investor. This is a critical transition for anyone learning how to start investing for beginners, as it turns your focus away from short-term fear and toward long-term success.

Alright, let's tackle those nagging questions that pop up right when you're about to dive in. It’s totally normal. You can have a solid plan, but a few lingering "what ifs" can keep you from pulling the trigger. This is where we clear the air on the practical stuff every new investor wonders about.

We'll get straight to the point on how much cash you actually need to start, what the real difference is between the most common accounts, whether your money is safe, and the simple version of how investment taxes work.

How Much Money Do I Actually Need to Start?

Let's bust a huge myth right out of the gate: you do not need a pile of cash to become an investor. The old-school idea that you need thousands of dollars to get a seat at the table is completely outdated. Today, the cost of entry is basically zero.

Thanks to a feature called fractional shares, which most modern online brokerages now offer, you can get started with whatever amount fits your life. Seriously. This lets you buy a tiny slice of any stock, even the pricey ones like Amazon or Google, for as little as $1 or $5.

The real goal isn't about how much you start with. It's about building the habit of investing consistently. Instead of asking how much you need to start, ask yourself, "How much can I comfortably invest on a regular basis?"

Even if it's just $25 or $50 a month, the act of getting started and automating those contributions is infinitely more powerful than waiting on the sidelines trying to save up a big lump sum.

A Robo-Advisor vs. a Brokerage Account: What’s the Difference?

When you're deciding where to open an account, it usually boils down to this choice. Think of it as the difference between a "do-it-for-me" service and a "do-it-yourself" toolkit.

A robo-advisor is an automated platform that builds and manages a diversified portfolio for you. You'll answer some questions about your goals, timeline, and how you feel about risk. Based on your answers, its algorithm puts together and maintains a mix of low-cost ETFs. It's designed to be completely hands-off.

A brokerage account, on the other hand, is the DIY option. It’s a platform that gives you the keys to the car. You're in total control, deciding exactly what to buy and sell, whether that's index funds, individual stocks, or other securities.

Here’s a simple way to figure out which is right for you:

- Go with a Robo-Advisor if: You want to get invested right away without the stress of making the decisions yourself. It’s a fantastic, set-it-and-forget-it way to get a balanced portfolio from day one.

- Go with a Brokerage Account if: You're genuinely curious about picking your own investments, want full control, and are excited to learn the ropes of building your own portfolio.

Is My Money Protected if My Broker Goes Bust?

Yes. This is a common and totally valid worry. In the United States, your investments have a serious safety net.

Nearly every legitimate brokerage firm is a member of the Securities Investor Protection Corporation (SIPC). If your brokerage were to fail or go bankrupt, SIPC steps in to protect the securities and cash in your account. The coverage is up to $500,000 per customer, which includes a $250,000 limit for cash held in the account.

Key Takeaway: It's critical to know what SIPC does and doesn't cover. It protects you if your brokerage firm fails. It does not protect you from market losses. If your investments go down in value, that’s just the normal risk of investing—SIPC doesn't cover that.

How Do Investment Taxes Work (The Simple Version)?

When you sell an investment for more than you paid for it, you have a profit. In the investing world, that's called a capital gain, and you might have to pay taxes on it.

There are two types of capital gains, and knowing the difference is huge for your long-term results.

- Short-Term Capital Gains: This is your profit on any investment you held for one year or less. The tax man treats this gain just like your regular salary, taxing it at your ordinary income tax rate.

- Long-Term Capital Gains: This is your profit on investments you held for more than one year. These gains are taxed at much lower, friendlier rates.

This is exactly why a long-term "buy and hold" approach is so powerful. Just by holding your investments for more than a year before selling, you can dramatically lower the tax bill on your profits.

Even better, when you use tax-advantaged accounts like a 401(k) or an IRA, your investments can grow for years without you owing any taxes on the gains or dividends along the way. You only deal with taxes much later, in retirement.

At Investogy, we believe that building conviction comes from understanding the "why" behind every investment decision. Our free weekly newsletter offers a 3-minute read that dives deep into our real-money portfolio, sharing the research and strategies we use. See how we're navigating the market by subscribing at https://investogy.com.

Leave a Reply