We've all heard the old saying, "don't put all your eggs in one basket." But when it comes to investing, real diversification is a lot more deliberate than just owning a few different stocks. It’s about strategically building a portfolio with different kinds of assets—across various industries and even countries—to protect your wealth when the market gets choppy.

This is the bedrock of managing risk while still hunting for those consistent, long-term gains.

Building a Portfolio That Can Weather Any Storm

The core idea is simple: different investments react differently to the same economic news. It's a structured approach to make sure a hit to one part of your portfolio doesn't torpedo the whole thing.

For example, when the economy is booming, stocks tend to do great. Bonds, on the other hand, might just plod along with modest returns. But when a recession hits? Those stable government bonds can be a lifesaver, acting as a buffer while stock prices are taking a nosedive. By owning both, you create a much smoother ride for yourself.

Why This Isn't Just "Owning More Stuff"

A truly diversified portfolio isn't about owning hundreds of random assets. It’s about owning different types of assets that don’t all zig and zag in the same direction at the same time. This is what smart risk management is all about.

Think about it. If your entire portfolio was in tech stocks, you'd have felt like a genius during a tech boom. But you would have been completely wiped out during the dot-com bust. A well-constructed portfolio is designed to capture growth from different parts of the market while shielding you from those kinds of concentrated, catastrophic losses.

A well-diversified portfolio is your financial shock absorber. It’s not about avoiding all losses, but about ensuring that no single event can derail your entire long-term plan.

A Practical Blueprint for Diversification

Building this financial shield isn’t a one-and-done task; it’s a living, breathing process. It boils down to a few core stages you'll repeat over your investing life.

- Know Your Starting Point: First, you have to get honest about your own financial situation. How much time do you have? And just as important, how much volatility can your stomach actually handle?

- Pick Your Players: This is where you choose the right mix of asset classes—stocks, bonds, maybe some real estate or alternatives—that fits the risk profile you just defined.

- Stay on Top of It: Markets shift, and so do your goals. That means you need to check in on your portfolio periodically and rebalance it to make sure it hasn't drifted away from your original plan. For a deeper dive into the mechanics, it’s worth reviewing established portfolio management best practices.

As you get more comfortable, you might even bring in more sophisticated tools to help. For example, an AI finance investment analyst can offer a level of analysis that was once reserved for the pros, helping you spot trends and opportunities.

By following a structured approach like this, building a resilient, diversified portfolio moves from being a Wall Street concept to a completely achievable goal for any serious investor.

Define Your Financial Goals and Risk Tolerance

Before you even think about picking stocks or funds, the first step in building a diversified portfolio is a serious look in the mirror. A winning strategy isn't something you pull off a shelf; it's custom-built around your actual life. It needs to reflect what you want your money to do for you and, just as importantly, how much turbulence you can stomach to get there.

Your investment timeline is the absolute first thing to nail down. Are you playing the long game, saving for something decades away like retirement? Or is your goal much closer, like a down payment on a house in five years? The answer completely changes the rulebook. A long runway means you can afford to ride out the market’s inevitable roller coasters. A shorter one demands a much more cautious game plan to keep your starting capital safe.

Matching Your Timeline to Your Strategy

Let's get real for a second. Picture two investors. One is 30, socking away money for retirement in 35 years. The other is 45, saving for their kid’s college tuition that’s due in just three years. Their strategies should look nothing alike.

- The Retirement Saver: With decades ahead, this person can build a more aggressive portfolio, likely tilting heavily towards stocks. They have plenty of time to bounce back from market downturns.

- The College Saver: This investor's number one job is capital preservation. A big market drop right before that tuition bill comes would be a complete disaster. Their portfolio needs to be anchored in less volatile assets, like bonds and cash.

This isn't just a minor detail—it's everything. How you structure your portfolio has to be a direct result of when you need to cash in. If you want to see how different strategies might play out over your timeline, plugging some numbers into a good investment calculator can be incredibly eye-opening.

Honestly Assessing Your Risk Tolerance

Once you’ve got your timeline sorted, you need a frank conversation with yourself about risk. And I don’t mean just a gut feeling. I'm talking about how you would actually react—both emotionally and financially—if you logged into your account and saw its value had tanked.

A classic rookie mistake is overestimating how much risk you can handle when the market is flying high, only to freak out and sell everything when it crashes. Your true risk tolerance is measured by your ability to stick with your plan when things get ugly.

Are you an aggressive investor, willing to take big swings for a shot at bigger returns? Or are you a conservative investor who cares more about protecting your principal than anything else? Most of us land somewhere in the middle as moderate investors, looking for a mix of growth and safety.

Be honest. Nailing down your risk profile is the key to building a portfolio that you can actually live with through thick and thin. It prevents you from making those gut-wrenching, emotional decisions that can completely derail your long-term success. At the end of the day, your portfolio should let you sleep at night.

Select Your Core Asset Classes

Once you've got a handle on your goals and how much risk you're willing to take on, it's time to pick the essential building blocks for your portfolio. I like to think of asset classes as different players on a team, each with a specific job. You’re not just trying to pick the "best" player; you're building a team that works together, balancing offense (growth) with defense (stability).

Your main players will be stocks (equities), bonds (fixed income), and maybe some alternatives. Each one reacts differently to what the economy is doing, and that's precisely what makes them so powerful when you combine them for diversification.

Understanding Your Core Players

Stocks, also known as equities, represent a slice of ownership in a company. They are the growth engine of your portfolio, hands down. Over the long haul, they offer the highest potential returns, but that potential comes with a healthy dose of volatility. When the economy is humming, stocks tend to soar, but they can take a serious hit during downturns.

To really diversify your stock holdings, you need to think beyond just owning a bunch of different company names. You should spread your investments across:

- Company Size (Market Capitalization): This means mixing in large-cap (the established giants), mid-cap (companies in their growth phase), and small-cap (newer firms with high-risk, high-reward potential) stocks.

- Industry and Sector: Spreading your money across technology, healthcare, consumer staples, and industrial sectors is crucial. It keeps you from being too exposed if one part of the economy gets hammered. Just look at the 2022 market downturn—a whopping 96% of stocks in the S&P 500 experienced drawdowns of at least 15%. That shows you how widespread the pain can be, even within a supposedly diversified index.

Bonds, or fixed-income securities, are basically loans you make to a government or a corporation. In return, they promise to pay you regular interest. These are the defensive anchors of your portfolio. While the returns aren't usually as high as stocks, bonds bring stability and income to the table. They often hold their value or even go up when the stock market is tanking.

To give you a clearer picture, here's a simple breakdown of how these main asset classes stack up against each other.

Comparing Core Asset Classes

| Asset Class | Typical Risk Level | Primary Role in Portfolio |

|---|---|---|

| Stocks (Equities) | High | The primary driver of long-term growth and capital appreciation. |

| Bonds (Fixed Income) | Low to Medium | Provides stability, generates regular income, and acts as a buffer during stock market downturns. |

| Alternatives (e.g., Real Estate, Gold) | Varies | Adds further diversification with low correlation to stocks and bonds, often acting as an inflation hedge. |

This table shows the fundamental trade-offs at play. You're balancing the high-growth potential of stocks with the steadying influence of bonds and the unique characteristics of alternatives.

The real magic happens when you combine these assets. Stocks provide the horsepower for growth, while bonds act as the suspension, smoothing out the bumps along the way. This balance is fundamental to how to diversify an investment portfolio effectively.

Bringing It All Together With Funds

For most of us, buying enough individual stocks and bonds to be truly diversified is just not practical. It's time-consuming and can be expensive. This is where exchange-traded funds (ETFs) and mutual funds are a game-changer. These funds pool money from thousands of investors to buy a massive basket of assets, giving you instant diversification in a single transaction.

For instance, buying an S&P 500 ETF gives you a small piece of 500 of the biggest companies in the U.S. A total bond market fund exposes you to thousands of different government and corporate bonds. Using these tools is, by far, the most efficient way to build a diversified core for your portfolio. For a more detailed walkthrough, our complete guide on how to build an investment portfolio from scratch lays out the entire framework.

Lastly, don't forget about alternatives. These are assets that fall outside the traditional stock and bond categories, like real estate (often through REITs) or commodities like gold. They typically have a low correlation to the stock market, which means they can zig when other assets zag, adding yet another valuable layer of protection to your overall strategy.

Go Global to Grow and Protect Your Portfolio

A truly modern approach to diversification has to look beyond your home country's borders. It’s easy to get comfortable investing where you live, but concentrating all your investments in one economy—even one as massive as the U.S.—is a risk I’m not willing to take. Think of global diversification as your shield against country-specific economic slumps, political drama, or sudden market downturns.

Let me put it this way: if the U.S. market is having a rough year, booming economies elsewhere in the world could help balance out your returns. By investing globally, you're tapping into different growth cycles and insulating your portfolio from localized shocks. This isn't some advanced, risky tactic; it's a fundamental strategy for building a resilient portfolio in a world that’s more interconnected than ever.

How to Actually Invest Globally

Getting started with international investing is surprisingly straightforward these days, mostly thanks to the explosion of accessible tools like ETFs. You don't need to become an expert on the Tokyo Stock Exchange or try to navigate European markets on your own. You can just use funds that do all the heavy lifting for you.

Here’s what I look at:

- International Stock ETFs: These funds give you broad exposure to companies outside your home country. For example, an "All-World ex-US" ETF invests in thousands of companies across both developed and emerging markets, giving you instant global reach.

- Developed vs. Emerging Markets: It’s smart to distinguish between these two. Developed markets are the stable, mature economies like Japan, Germany, and the UK. Emerging markets, on the other hand, include places like Brazil, India, and China. They offer much higher growth potential but, as you'd expect, come with more volatility. I’ve found that a mix of both provides a good balance of growth and stability.

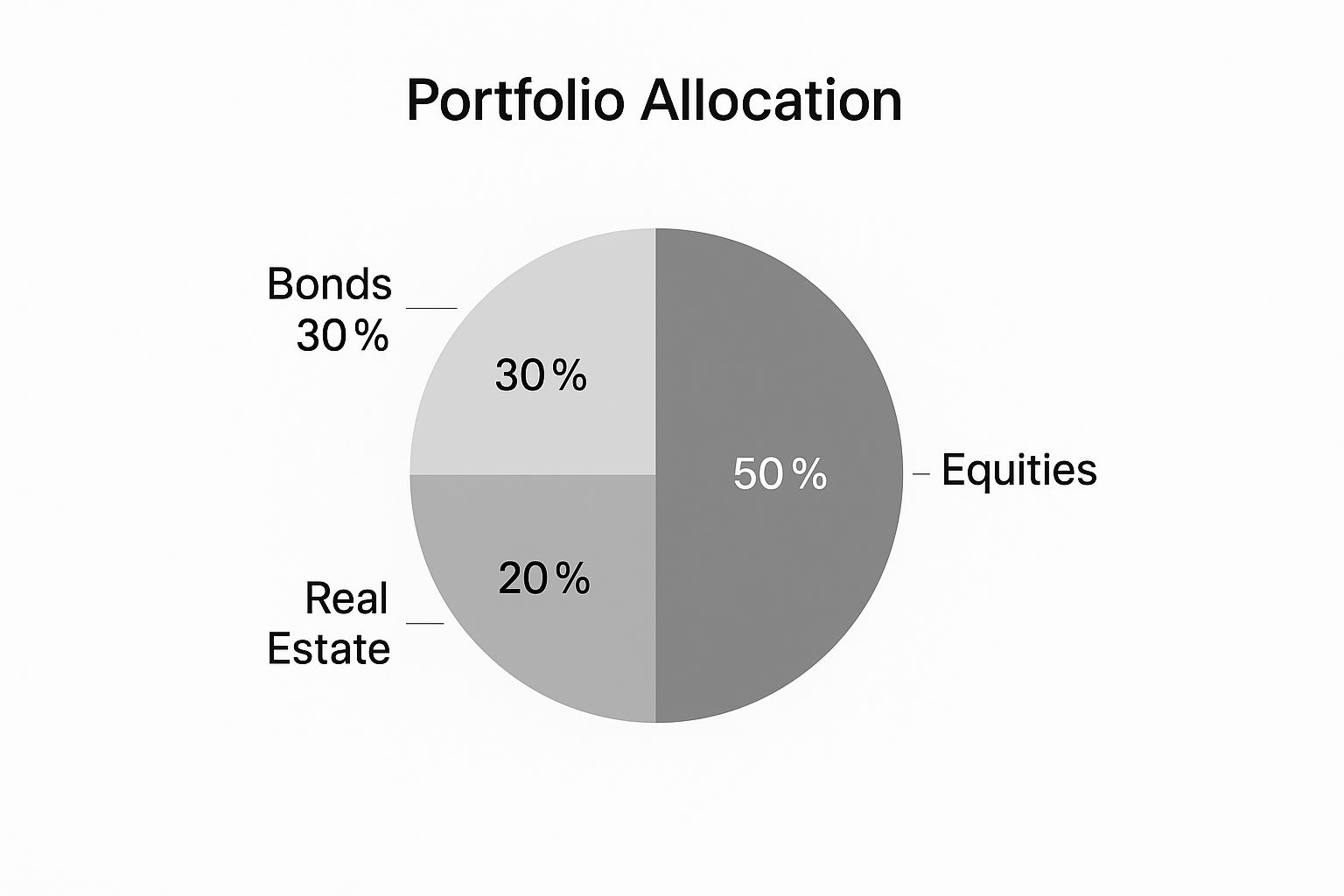

The infographic below shows how different asset classes, including those with a global reach, might fit into a balanced portfolio.

This visual gives a good starting point, but a real global strategy would take that "Equities" slice and break it down further into domestic and international holdings.

Does Global Diversification Still Work?

I hear this question a lot. Some investors wonder if global diversification is still effective, given how connected world markets have become. It's true—financial globalization has increased how closely markets move together, especially during a crisis. But the risk-reduction benefits are far from gone, particularly if you’re a long-term investor like me.

While the world’s financial markets have grown more integrated since the late 1990s, this has not erased the long-term benefits of diversifying your equity holdings globally.

Even with increased correlations for bonds, a mountain of research shows that diversifying stocks across different countries is still a powerful tool for reducing risk. This is because the underlying business profits (the cash flows) of companies in different countries don't always move in lockstep. If you want to dive into the data, you can explore the detailed findings on how global diversification benefits have evolved.

The bottom line is clear: for anyone with a long investment horizon, international equities are a critical piece of the puzzle. Ignoring the rest of the world means you're leaving a powerful diversification tool on the table.

Mastering Portfolio Rebalancing And Monitoring

Putting together a diversified portfolio is a huge step, but the job isn’t done. Far from it. An investment plan isn’t some “set it and forget it” machine. Over time, the everyday ups and downs of the market will cause your carefully chosen asset mix to drift. This process can quietly wreck your diversification efforts and saddle you with risks you never intended to take.

Let’s say you started with a target of 60% stocks and 40% bonds. After a big run-up in the stock market, those stocks might swell in value, pushing your actual allocation to 70% stocks and 30% bonds. Suddenly, your portfolio is much more aggressive than you planned and way more vulnerable if stocks take a nosedive. This is exactly why getting a handle on portfolio rebalancing and monitoring is so critical.

Choosing Your Rebalancing Trigger

Rebalancing is simply the disciplined process of buying or selling assets to get your portfolio back to its original target. It's a systematic way to force yourself to "buy low and sell high" without trying to time the market. I've seen two main ways people approach this.

- Calendar-Based Rebalancing: This is the most straightforward method. You just pick a schedule—say, every quarter, or once a year on your birthday—and you rebalance on those dates, no matter what the market is doing.

- Percentage-Based Rebalancing: This approach is triggered by market moves. You might set a rule to rebalance whenever any single asset class strays more than 5% from its target weight.

Honestly, neither method is hands-down better than the other. The real key is to pick one and stick with it. Consistency is the name of the game for long-term investing discipline. For a deeper dive on keeping your strategy consistent, check out our guide on the 10 best long-term investment strategies.

The Mechanics Of A Portfolio Review

Your portfolio review is when the rebalancing magic happens. This is your chance to compare where your assets are now to where you want them to be and then take action.

So, back to our example: if stocks have grown from 60% to 65% of your portfolio and bonds have shrunk from 40% to 35%, you'd sell off some of those winning stocks. Then, you'd take that cash and buy more bonds until you're back at your 60/40 split. This is the simple, powerful heart of maintaining your desired risk level year after year.

Rebalancing isn't about predicting what the market will do next; it's about controlling your risk. It makes you take profits from your winners and plow them into assets that are currently down, keeping your entire strategy on course.

It's also worth remembering that risk can build up even inside a single market. For instance, recent data showed that the top ten U.S. stocks made up a whopping 29% of the total U.S. market capitalization. While U.S. stocks have been a great place to be, that level of concentration is a flashing light that reminds us to stay vigilant. Global diversification is still one of the best tools we have for managing uncertainty, because what worked in the past is no guarantee for the future.

Finally, none of this works without good, clean data. You have to track your investments accurately and consistently. Sticking to established financial reporting best practices makes sure you have clear, reliable numbers to work with when making these important decisions. This kind of discipline is what turns diversification from a one-time setup into a sustainable, lifelong habit.

Of course. Here is the rewritten section, crafted to sound like an experienced human expert.

Your Top Diversification Questions Answered

Even when you feel like you have a handle on diversification, a few nagging questions always seem to surface. It’s completely normal. I've been investing for years, and these are the same questions I hear from friends, family, and new investors all the time.

Let's clear the air and tackle some of the most common ones so you can build your portfolio with real confidence.

Seriously, How Many Stocks Is Enough?

There isn’t a single magic number here, but the old rule of thumb you'll hear from finance professors is that owning 20 to 30 individual stocks across different industries can do a decent job of wiping out most company-specific risk.

But let's be real. For most of us, picking and managing that many individual stocks is a massive headache. It's practically a part-time job.

A much saner approach for the average person is to use broad-market ETFs or mutual funds. A single, well-chosen fund can give you instant ownership in hundreds, sometimes thousands, of companies. You get powerful diversification right out of the box without the endless research.

Are Target-Date Funds a "Done-for-You" Diversified Portfolio?

Yes, that’s exactly what they are. Target-date funds are built from the ground up to be a complete, all-in-one portfolio. Think of them as a "fund of funds."

Inside one, you'll find a pre-packaged mix of U.S. stocks, international stocks, and bonds. The real genius is their automatic "glide path." As your retirement date gets closer, the fund automatically shifts its holdings to become more conservative, moving from mostly stocks to mostly bonds. They are the ultimate "set it and forget it" option if you'd rather not tinker with your investments.

Is It Possible to Be Too Diversified?

It sounds counterintuitive, but absolutely. Some people call it "diworsification." This is what happens when you own so many different investments that you accidentally water down your returns to just the market average, all while adding unnecessary complexity and fees.

Owning five different S&P 500 funds isn't diversification; it's just owning the same 500 stocks five times over. True diversification is about owning assets that zig while others zag, not just owning more stuff.

The goal is a thoughtful blend of assets that behave differently under various market conditions. Adding investments that are highly correlated—meaning they all move up or down together—doesn't really help protect you.

Global market data makes this crystal clear. While a broad portfolio dramatically cuts down on the wild swings you'd see with individual stocks, you can't eliminate risk entirely. For instance, the average volatility of top global stocks was around a stomach-churning 39.80%. A diversified portfolio slashed that to under 18%. That’s a huge benefit, but as you can see, you can't diversify away all risk. You can dive deeper into how market indices impact diversification with this detailed analysis. Smart diversification isn’t about quantity; it’s about combining assets with low correlation to one another.

At Investogy, we don't just talk about diversification; we show you how it works with our own real-money portfolio. Subscribe to our free weekly newsletter to get the research and insights behind every move we make. Join us at https://investogy.com.

Leave a Reply