When you're investing during high inflation, the old playbook gets tossed out the window. Cash and so-called "safe" investments like bonds start acting like a leaky bucket, losing purchasing power with every tick of the clock. The real key is to own assets that can actually outpace rising prices. I'm talking about things like real estate, commodities, and shares in companies with strong pricing power. This isn't just about protecting what you have; it's about making sure your capital can still grow in real terms.

Why Inflation Changes the Rules for Investors

Let's be honest—the standard advice to "buy and hold" feels a lot different when the cost of everything from gas to groceries is soaring. High inflation is a sneaky threat to your financial goals because it works in the background, silently eating away at the value of your money every single day. It's the hidden tax that punishes savers and rewards debtors.

The core problem boils down to the difference between nominal returns (the number you see on your statement) and real returns (your return after you subtract inflation). If your portfolio is chugging along at a 3% gain, but inflation is raging at 5%, you’re actually losing 2% of your purchasing power that year.

Your account balance might be going up, but you can buy less with it than you could before. This is the fundamental challenge every investor has to grapple with.

The Problem with "Safe" Investments

In a low-inflation world, holding cash or government bonds is a perfectly sensible way to dial down risk. But when inflation picks up steam, these same assets can become the biggest drag on your portfolio. Their fixed returns just can't keep pace when consumer prices are on a tear.

History gives us a pretty stark warning here. Take the Great Inflation period from 1965 to 1982, when U.S. inflation averaged a jaw-dropping 6.56% a year. During that time, even 30-year U.S. Treasury bonds—long considered a pillar of safety—only delivered an average annual return of 5.23%. Investors holding them were effectively getting poorer in real terms. You can explore the historical data on how inflation impacts traditional assets to see these trends for yourself.

It really drives home a critical point: strategies that are brilliant in one economic climate can fail spectacularly in another.

A Tale of Two Portfolios

To see why you need a proactive strategy, let's look at a simple real-world scenario. Picture two investors, Alex and Ben, who each start with $10,000.

- Alex plays it safe. He puts his cash into a high-yield savings account that earns him 1% annually.

- Ben invests to hedge against inflation. He puts his money into a diversified mix of real assets and stocks with pricing power, aiming for a return that can beat whatever inflation throws at him.

Now, let's say inflation averages 4% over the next five years. Alex’s savings account will have grown on paper, sure, but its actual purchasing power will have taken a serious hit. Ben’s portfolio, on the other hand, was specifically designed to rise with or even above inflation. It's far more likely to have not just preserved but grown its real value.

This is exactly why learning how to invest during inflation isn't some advanced topic for finance geeks—it's absolutely essential for protecting your financial future.

Building a Resilient Portfolio with Real Assets

When the value of your dollar starts to shrink, owning things becomes one of the most reliable ways to protect your wealth. This is the simple, powerful idea behind investing in real assets—tangible items that have their own inherent value. They often serve as a fantastic hedge against inflation because their prices tend to climb right alongside (or even faster than) the rising cost of living.

Here’s a simple way to think about it: when it costs more to build a new apartment complex or mine an ounce of gold, the value of existing apartment buildings and gold reserves naturally goes up. This direct connection to the real, physical economy is what gives these assets their punch during inflationary periods.

Let's break down three accessible ways to add this kind of resilience to your portfolio.

Diversify with Real Estate

You don't need the hassle of becoming a landlord to get exposure to the real estate market. For most of us, the simplest and most efficient route is through Real Estate Investment Trusts (REITs). These are basically companies that own and operate income-producing properties, and you can buy and sell their shares just like any other stock.

An ETF like the Vanguard Real Estate ETF (VNQ) is a great starting point. It gives you instant diversification across a huge range of property types—from apartment buildings and warehouses to shopping centers and office towers. As landlords raise rents to keep up with inflation, the income paid out to REIT shareholders also tends to increase. It's a direct, passive way to hedge against rising prices.

Of course, if you are considering buying a physical property, make sure you crunch the numbers. Using a solid rental property ROI calculator is non-negotiable for figuring out if a potential investment actually makes sense in the current market.

Add a Layer of Commodity Protection

Commodities are the raw materials that fuel the global economy, and their prices often take off during periods of high inflation. Adding a slice of commodities to your portfolio can be a smart move, providing a source of returns that doesn't always move in lockstep with the stock market.

I tend to focus on two key areas here:

- Precious Metals: Gold is the classic inflation hedge. For centuries, it's been seen as a reliable store of value when traditional currencies start to look shaky. A straightforward way to get exposure is through an ETF like SPDR Gold Shares (GLD).

- Industrial Metals & Energy: Think copper, aluminum, and oil. These are the critical inputs for everything from construction to technology. As the economy chugs along and prices rise, the demand for these foundational materials stays strong.

Pro Tip: You don't need to go overboard. A modest allocation, maybe 5-10% of your total portfolio, is often enough. The goal is to get the diversification benefit without taking on the wild price swings that can sometimes come with commodities.

Comparing Real Asset Investments for Inflation Hedging

This table breaks down the characteristics of key real assets, helping you choose the right options based on your risk tolerance, liquidity needs, and investment goals.

| Asset Type | Primary Benefit in Inflation | How to Invest (Example) | Risk Level |

|---|---|---|---|

| Real Estate (REITs) | Rising rents lead to higher dividend income. | Buy a broad market REIT ETF like VNQ. | Medium |

| Gold | Acts as a store of value when currency devalues. | Buy a Gold ETF like GLD. | Medium-High |

| Industrial Commodities | Prices rise with increased production costs & demand. | Invest in a broad commodity ETF like DBC. | High |

| Infrastructure | Long-term contracts often include inflation-linked adjustments. | Invest in an Infrastructure Fund ETF like PAVE. | Medium |

Choosing a mix of these can create a much more robust portfolio that is better prepared to handle whatever the economy throws at it.

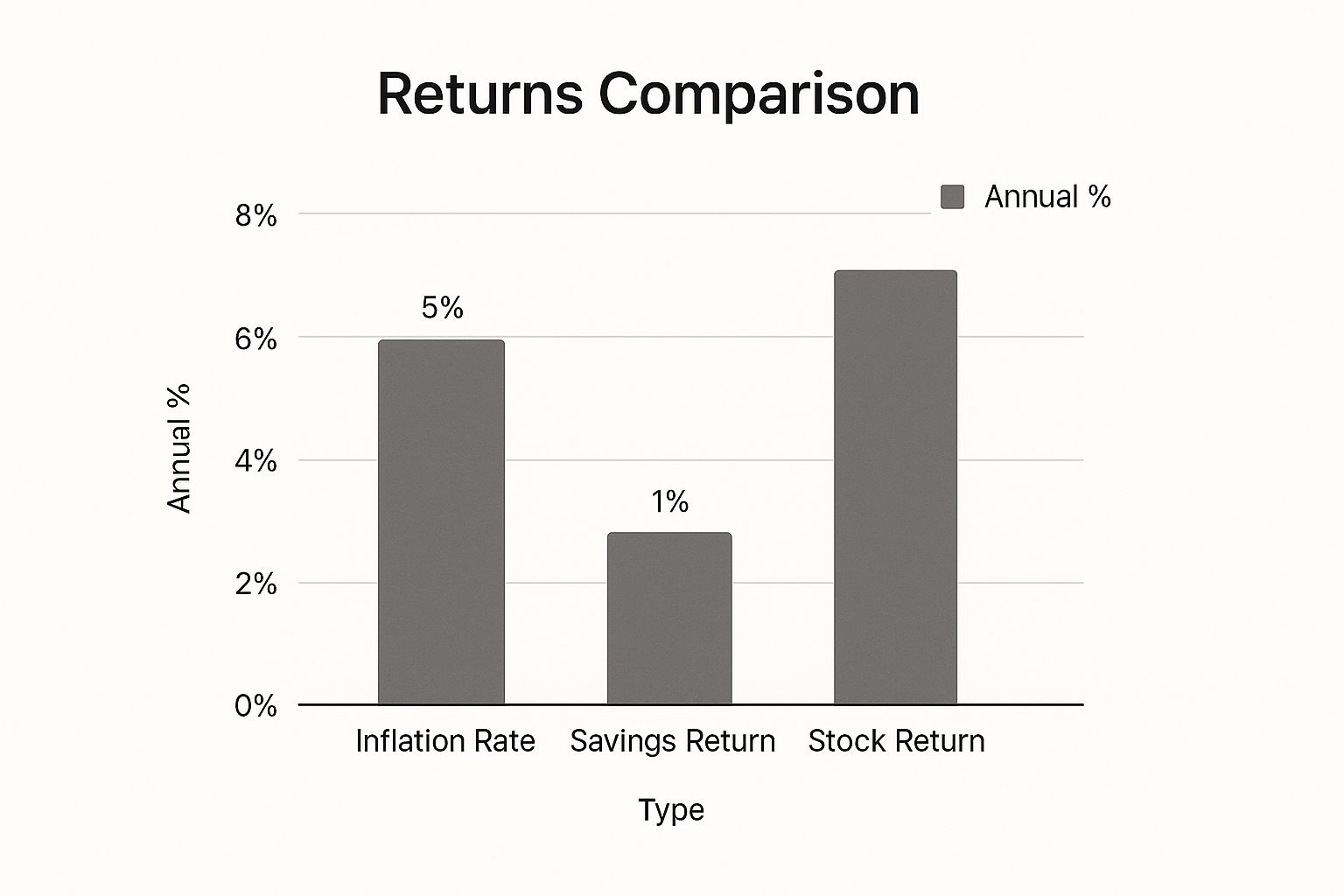

This chart is a great visual reminder of why this matters. It clearly shows that while stocks can deliver growth, those returns can be seriously eaten away by inflation. And relying on traditional savings? That's a losing game in an inflationary environment.

Invest in Essential Infrastructure

Infrastructure forms the very backbone of our society—think toll roads, energy pipelines, and cell towers. What makes these assets so appealing is that they are typically backed by long-term contracts that have inflation-adjustment clauses baked right in. In other words, their revenue streams are designed to automatically rise with inflation.

Investing in infrastructure funds can provide a steady, inflation-linked source of income. These are long-term, defensive assets that can add a lot of stability to your portfolio, especially when market uncertainty is running high.

Bringing these real assets into your portfolio is a critical step in adapting your investment strategy for the times. If you're building your portfolio from the ground up, our guide on how to build an investment portfolio provides an excellent foundation before you start layering in these specialized inflation hedges.

Hunting for Stocks That Can Weather an Inflationary Storm

When inflation starts running hot, just “owning stocks” isn’t much of a game plan. Sure, equities generally beat holding cash or bonds when prices are climbing, but the real magic is in finding specific companies that are built to handle—or even capitalize on—this kind of economic pressure. It's a whole lot more nuanced than just buying a broad market index and hoping for the best.

The single most important trait you should be hunting for is pricing power. This is just a fancy way of saying a company can jack up its prices without scaring away its customers. Businesses with iconic brands, products people can't live without, or services that are a pain to switch from usually have this in spades.

Zero In on Sectors with Built-in Advantages

In an inflationary world, some market sectors are just naturally better positioned than others. Certain industries can pass higher costs straight to their customers, while others get their profit margins squeezed dry. Over the years, a few areas have proven to be incredibly tough.

- Consumer Staples: We’re talking about companies that sell stuff we all buy no matter what the economy is doing—think toothpaste, soap, and soda. Demand is rock-solid. Giants like Procter & Gamble or Coca-Cola can usually nudge their prices up little by little without anyone really batting an eye.

- Energy: As one of the main things causing inflation, the energy sector tends to do quite well. When the price of oil and natural gas goes up, the revenue and profits for producers and service companies follow right along.

- Materials: These are the businesses that pull raw materials out of the ground and process them for everyone else. Just like energy companies, their success is directly linked to commodity prices, which often spike during inflationary periods.

Key Takeaway: You want to find businesses whose revenues rise with inflation, not just their costs. Companies with serious pricing power can defend their profit margins, which makes their stock a far better inflation hedge.

This isn't just theory. If you look at U.S. stock market data from the brutal inflation of 1980, when annual inflation shot past 13%, the S&P 500 cranked out an impressive 31.74% nominal return. But the story doesn't end there. In 1981, with inflation still a major problem, stocks actually fell by 4.7%. It's a stark reminder that while stocks can work, you need to be selective and ready for some ups and downs. You can see the historical data for yourself on NYU's Stern School of Business website.

Time to Pop the Hood and Check the Financials

Picking the right sector is a great start, but it won't save you if you bet on a weak company. You’ve got to get your hands dirty and look at the company’s financial health. Here’s what I focus on when I’m sizing up individual stocks or checking the holdings in a sector ETF.

- Healthy Profit Margins: I look for companies that consistently keep their gross and net profit margins high. This tells me they have a cushion to absorb rising costs without getting their bottom line wrecked.

- Low Debt Levels: High inflation often brings rising interest rates, and that makes carrying debt a lot more expensive. Companies with clean balance sheets and low debt-to-equity ratios are way less vulnerable when rates start to climb.

- Strong Cash Flow: A business that pumps out a steady stream of free cash flow has options. It has the financial muscle to get through tough times, keep investing in growth, and send cash back to its shareholders.

When you put all this together, you've got a powerful filter. You're not just throwing darts at a board; you're strategically screening for quality businesses that are built to survive and thrive in the current economic climate. For more tips on building a solid foundation, our guide on essential stock market investing tips can help you sharpen your stock-picking skills. This is how you shift your portfolio from being a victim of inflation to being a driver of real returns.

Using Inflation-Protected Bonds for Stability

Okay, so we've talked about using stocks and real assets for growth, but you can't just play offense when inflation is running hot. You absolutely have to shore up the defensive side of your portfolio. This is where inflation-protected bonds come into the picture. Think of them as a stabilizer specifically built to protect your money's buying power.

Unlike a regular bond that pays you a fixed interest rate, these government-backed securities have a killer feature: their principal value automatically moves up and down with the Consumer Price Index (CPI). So, if inflation jumps 5%, the face value of your bond also increases by 5%. This is a direct way to make sure your investment isn't losing ground to rising costs.

For U.S. investors, there are two main flavors of these bonds: Treasury Inflation-Protected Securities (TIPS) and Series I Savings Bonds (I Bonds). They both aim to shield you from inflation, but they work in very different ways.

Understanding TIPS and I Bonds

Treasury Inflation-Protected Securities (TIPS) are the more flexible of the two. You can buy and sell them on the open market, just like a stock or any other bond, right through your brokerage account. This liquidity makes them a breeze to work into a diversified portfolio. A lot of people, myself included, prefer to get exposure through a low-cost ETF like the iShares TIPS Bond ETF (TIP), which gives you a broad basket of these securities in one shot.

The interest you earn from TIPS has two components: a small, fixed "real" interest rate that's set when the bond is auctioned, plus that inflation adjustment. One thing to keep in mind is that you'll owe federal income tax each year on both the interest payments and the inflation-driven increase in principal—even though you won't actually see that principal bump until the bond matures.

Key Difference: TIPS are super liquid and can be bought in large amounts through any brokerage, which is great for bigger portfolios. I Bonds, on the other hand, are less liquid and come with strict annual purchase limits.

Series I Savings Bonds (I Bonds) are a different beast entirely. You buy these directly from the U.S. government through the TreasuryDirect website. Their yield is a combo of a fixed rate (set for the life of the bond when you buy it) and a variable inflation rate that resets every six months. The big draw for I Bonds is the tax treatment: your interest earnings grow tax-deferred at the federal level until you cash them out, and they are completely free from state and local income taxes. That's a huge plus.

Making the Right Choice for Your Portfolio

So, which one belongs in your portfolio? It really boils down to what you value most: liquidity, tax benefits, or the amount you plan to invest.

- For Liquidity and Scale: Go with TIPS if you need the freedom to sell at any time or if you're looking to invest a significant chunk of money. They slot right into your existing brokerage accounts without any fuss.

- For Tax Advantages: I Bonds are your best bet if you can afford to lock up your money for at least a year and want to reap those tax-deferral benefits.

I Bonds have an annual purchase limit of $10,000 per person (though you can snag an extra $5,000 by using your tax refund), so they work best for smaller, dedicated inflation-proofing slices of your portfolio.

No matter which you choose, adding one of these instruments is a smart, direct move. It ensures that at least a portion of your portfolio is explicitly built to withstand the corrosive effect of rising prices.

Avoiding Costly Investor Mistakes During Inflation

Knowing which assets to pick up is only half the battle when you're trying to figure out how to invest during inflation. Just as critical is knowing what not to do. An inflationary environment kicks up a lot of anxiety, and that anxiety often leads to expensive, emotional decisions that can completely derail a solid strategy.

The single biggest mistake I see investors make is panic-selling into volatility. The headlines get scary, the markets get choppy, and the gut reaction is to sell everything and run for the perceived safety of cash. But this usually just locks in your losses. You then end up sitting on the sidelines while the market recovers, which can happen a lot faster than anyone expects.

The Dangers of Flawed Thinking

Another common pitfall is just not getting the difference between nominal and real returns. It's easy to feel good when you see your account balance going up. But if those gains aren't beating inflation, you're actually losing purchasing power. Your money is worth less, not more.

This confusion is more widespread than you might think. A 2022 study of German investors found that about half of them wrongly expected stock market nominal returns to fall during high inflation, which is the opposite of what history shows. This knowledge gap can lead to some really poor portfolio choices and just highlights how important it is for investors to get educated.

The most successful investors during these periods aren't the ones making the most brilliant moves. They are the ones who avoid making the biggest blunders. Discipline trumps genius every time.

A Disciplined Approach to Market Noise

So, how do you stay the course when every instinct is screaming "do something"? The answer is building disciplined habits and having a concrete plan before the storm hits.

Here are a few core principles I stick to that keep me grounded:

- Stick to Your Long-Term Plan: Remember why you invested in the first place. Your goals—whether that's retirement, a down payment, or financial freedom—haven't changed, even if the economic weather has.

- Use Dollar-Cost Averaging: Consistently investing a fixed amount of money at regular intervals is an incredibly powerful tool. It forces you to buy more shares when prices are low and fewer when they are high, which smooths out your average cost over the long haul.

- Focus on What You Can Control: You can't control inflation, interest rates, or geopolitical drama. You can control your savings rate, your asset allocation, and your own reactions. Focus there.

These behavioral guardrails are just as important as the assets you pick. A volatile market can feel a lot like navigating a recession, and our guide on how to invest during a recession offers some great complementary strategies for staying disciplined.

To really shore up your portfolio's defenses, it's worth digging into effective portfolio risk management practices), which cover things like position sizing, diversification, and rebalancing. By combining a sound strategy with some psychological grit, you can sidestep the behavioral traps that snare so many investors and keep your eyes on the long-term prize.

Common Questions About Investing and Inflation

Even with a solid game plan, it’s normal for questions to pop up when you're figuring out how to invest during inflation. This is an environment that makes even the most seasoned investors pause and double-check their assumptions. Here, I'll tackle some of the most common questions we get, with straightforward answers to back up the strategies we’ve already covered.

Think of this as a quick-reference guide to clear up any lingering confusion and give you more confidence as you fine-tune your portfolio for rising prices.

How Much of My Portfolio Should Go to Inflation Hedges?

This is usually the first question on everyone's mind. How much should I really set aside for specific inflation hedges like TIPS or gold?

There's no single magic number here, but for a balanced portfolio, a common starting point is a 5-10% allocation to TIPS and another 5% to a commodity like gold. Of course, this number can shift quite a bit depending on your personal risk tolerance and how close you are to retirement.

Think of these assets as insurance for your portfolio. Their main job is to provide diversification and a buffer for your core holdings, not to completely replace your growth-oriented stocks and other assets.

If you’re a more conservative investor or you're getting close to retirement, you might lean toward the higher end of that range for that extra layer of stability.

Are International Stocks a Good Hedge?

At first glance, investing abroad seems like a logical way to sidestep a purely domestic inflation problem. But it's not always the silver bullet people hope for.

International stocks can be a decent hedge, particularly if inflation is mainly a U.S. issue. In that kind of scenario, a weaker U.S. dollar can actually juice the returns you get from your foreign assets when you convert them back.

However, inflation is often a global beast. When other major economies are also battling rising prices, their stock markets probably won't offer the safe harbor you're looking for. The fundamental rules don't change: you still need to seek out high-quality international companies with serious pricing power and durable business models, no matter where they call home.

Should I Sell All My Traditional Bonds?

I get it. It’s incredibly tempting to dump traditional fixed-rate bonds when inflation is running hot, especially since their real returns dive into negative territory. But selling them all off is probably a mistake.

While it's true they lose purchasing power, traditional bonds still have a vital job to do: providing stability and acting as a cushion against stock market volatility. Instead of abandoning them completely, a much smarter approach is to:

- Shorten the duration of your bond holdings. This makes them less sensitive to interest rate hikes.

- Reallocate a portion of your fixed-income sleeve toward inflation-protected securities like TIPS or I Bonds.

Is Cryptocurrency a Reliable Inflation Hedge?

The idea that crypto, especially Bitcoin with its fixed supply, is the ultimate inflation hedge has been a hot topic for years. The actual performance data, however, tells a very different story.

So far, cryptocurrencies have proven to be wildly volatile. They've often moved in lockstep with other high-risk growth assets, like tech stocks—the very things you're trying to hedge. They simply haven't acted as a consistent store of value during the recent inflationary bouts. For most investors, crypto should be treated as a purely speculative asset, not a core piece of a serious inflation-hedging strategy.

Ready to see these principles in action? The Investogy newsletter offers a transparent look at how we manage a real-money portfolio, sharing our research, our moves, and our reasoning every week. See how we're navigating the current market by subscribing for free at https://investogy.com.

Leave a Reply