A winning investment decision making process doesn't start with a hot stock tip. It starts long before you even glance at a market chart. It begins with building your own personal framework. Think of it as your internal playbook—the set of rules that dictates how you invest, making sure every move you make lines up with your real life and long-term dreams.

Building Your Personal Investment Framework

Before you get lost in market research or company financials, the most important work you'll do is looking inward. A solid investment framework is your personal constitution. It's the document that keeps you steady when markets get choppy and stops you from making emotional, knee-jerk mistakes. This foundation is what separates disciplined investors from those just chasing the latest trend.

This entire framework really boils down to three core pillars: your goals, your time horizon, and your genuine comfort level with risk. If you don't have absolute clarity on these three things, you're basically navigating the markets without a map.

Define Your Financial Goals and Time Horizon

What are you actually investing for? The answer to this question shapes your entire strategy. Saving up for a down payment on a house you want to buy in five years demands a completely different game plan than saving for a retirement that's 30 years away.

Get specific. A vague goal like "build wealth" is useless. Define what that actually looks like for you. Is it hitting a $1 million portfolio by the time you're 60? Or maybe it's generating $2,000 a month in passive income to cover your bills.

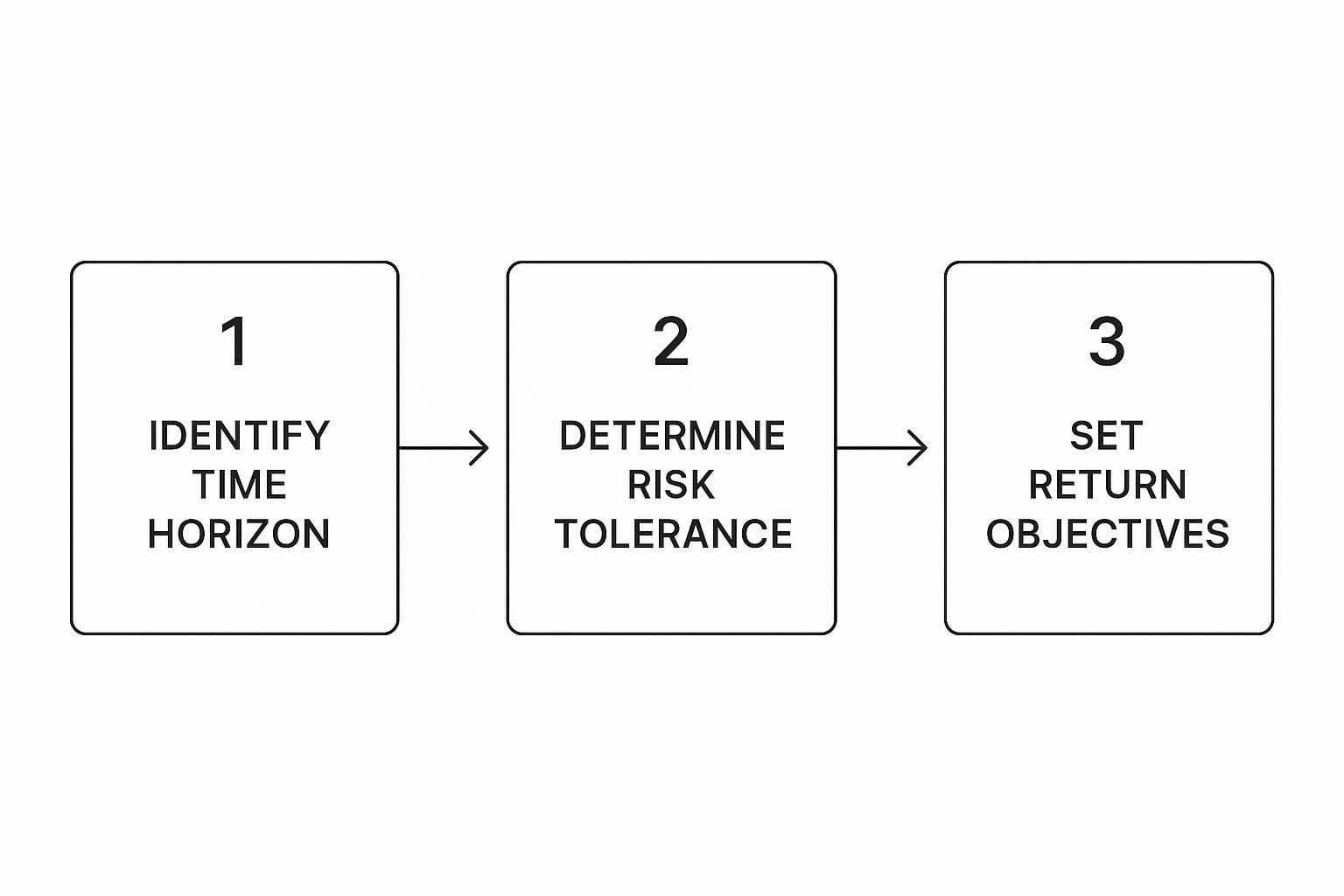

Your time horizon is the most powerful variable here.

- Short-Term Goals (Under 5 years): These goals need a capital preservation mindset. Think lower-risk investments like high-yield savings accounts or short-term bonds.

- Mid-Term Goals (5-10 years): You can afford to take on a bit more moderate risk, maybe with a balanced portfolio of stocks and bonds.

- Long-Term Goals (10+ years): A long runway like this is your green light to embrace higher-risk, higher-growth assets like stocks. You have plenty of time to ride out—and recover from—inevitable market downturns.

This process flow shows how identifying your time horizon and risk tolerance logically leads to setting your return objectives—not the other way around.

As the visual makes clear, you can't know what returns to aim for until you've figured out your timeline and how much risk you can stomach.

Honestly Assess Your Risk Tolerance

Risk tolerance isn't about how much you think you can handle on a good day. It's about how you'd actually react when your portfolio takes a 20% nosedive in a single month. Being brutally honest with yourself here is non-negotiable.

A critical mistake I see all the time is people overestimating their emotional strength. They sell everything in a panic during a market crash, locking in their losses and completely derailing their long-term plans. Your framework is designed to prevent you from doing exactly that.

Take a hard look at your financial stability, your age, and your emotional wiring. A young investor with a secure job can afford to take on more risk than someone on the verge of retirement. This self-assessment is the bedrock of a sound investment decision making process.

Before diving into the nitty-gritty of picking investments, it's crucial to formalize these core components. Many experienced investors do this by creating an Investment Policy Statement (IPS). This simple document acts as your guide, helping you maintain discipline and focus no matter what the market throws at you.

Core Components of Your Investment Framework

Here's a breakdown of the essential elements you need to define. Think of this table as the blueprint for your personal investment constitution.

| Component | Description | Real-World Example |

|---|---|---|

| Financial Goals | The specific, measurable outcomes you're investing to achieve. | "Save $50,000 for a house down payment within the next 7 years." |

| Time Horizon | The length of time you have to invest before you need to access the money. | "I have 25 years until my target retirement age of 65." |

| Risk Tolerance | Your emotional and financial capacity to handle market fluctuations and potential losses. | "I'm a moderate investor. I can handle a 15-20% drop without panicking, but a 40% loss would be too stressful." |

By taking the time to nail down these components, you're not just preparing to invest—you're setting yourself up for success by creating a powerful tool for maintaining discipline and focus over the long haul.

How Macroeconomic Trends Shape Your Investments

Okay, so you’ve got your personal framework dialed in. That's a great start, but a truly solid investment decision making process means looking beyond your own bank account and seeing the bigger picture. Companies don’t operate in a bubble; they're all swimming in the same massive, interconnected global ocean. Understanding how the major economic currents and weather patterns affect the markets is what separates investors who ride the waves from those who get swept away.

Think of the global economy as the climate system for your portfolio. A sunny day for the tech sector might be a full-blown hurricane for industrial stocks. You don't need a PhD in economics to get this, but you absolutely need to grasp how certain key indicators act as a forecast. It gives you a massive edge.

Reading the Economic Tea Leaves

A few key data points give you powerful clues about where the economy is heading. Paying attention to them is a non-negotiable part of my process.

- Gross Domestic Product (GDP): This is the big one—the broadest measure of a country's economic pulse. When GDP is climbing, it generally means the economy is healthy, which is great for corporate profits and stock prices.

- Inflation Rates: When the price of everything starts rising too fast, it eats away at everyone's purchasing power. This usually forces central banks to step in and hike interest rates, which makes it more expensive for companies to borrow money to grow.

- Interest Rate Policies: The decisions made by central banks like the Federal Reserve create huge ripple effects. Lower rates can juice the economy, while higher rates are used to pump the brakes and fight inflation.

These aren't just abstract numbers; they have real-world consequences for your money. For example, high inflation and rising rates can slam growth-heavy tech stocks. But they can also be a tailwind for value stocks in sectors like consumer staples—because people always need to buy toothpaste and toilet paper, no matter what. Recognizing these patterns is a cornerstone of smart investing.

Geopolitics and Where the Money is Flowing

Beyond the hard data, you have to watch the world stage. Geopolitical events, new trade deals, and regulatory shake-ups are constantly creating fresh risks and opportunities. A trade agreement could blow open huge new markets for an industry, while a conflict somewhere could shatter supply chains and send commodity prices soaring.

One of the most powerful, and often overlooked, signals of global confidence is foreign direct investment (FDI). This is when a company or individual in one country plows money into business interests in another. It's basically a long-term vote of confidence with real cash.

A recent trend I'm watching closely is a concerning 11% drop in global FDI, the second straight year of decline. What's driving this? Geopolitical tensions, new trade barriers, and governments getting much stricter about who invests where. It shows a global shift toward playing it safe and avoiding long-term risks. Even if some headline numbers look good, they often hide a serious drop in productive, real-world investment. You can explore the full UNCTAD report on these global investment trends to see for yourself.

This kind of data tells me that big, institutional money is getting nervous and picky. When the smart money pulls back, it’s a flashing yellow light for individual investors to be extra careful. It also underscores how economic downturns change how people invest, a topic we dive into in our guide on how to invest during a recession.

When you combine this top-down, big-picture macroeconomic view with your specific, bottom-up analysis of individual companies, you build a much more resilient investment decision making process. You’ll be in a far better position to see major shifts coming, protect your capital, and strategically place your bets for future growth.

Conducting Effective Research and Due Diligence

Alright, you've got your high-level strategy figured out. Now it's time to roll up your sleeves and get your hands dirty. This is where the real work of the investment decision making process begins: the research and due diligence phase.

Think of yourself as an investigative reporter. Your job is to move past the headlines and flashy news clips to uncover the real story behind a potential investment. This isn't about a quick Google search; it's a systematic process of gathering facts to find quality assets, spot hidden value, and—most importantly—identify any red flags before you put a single dollar at risk.

Getting Into the Weeds with Company Fundamentals

If you're looking at individual stocks, your first stop is the company's financial records. These aren't just numbers on a page; they're the vital signs that tell you about the health of the business.

- Income Statement: This is the report card. Is the company actually making money? I look for consistent revenue growth and, just as crucially, stable or expanding profit margins.

- Balance Sheet: This is a snapshot of financial resilience. It shows you what the company owns (assets) versus what it owes (liabilities). A business buried in debt is a huge red flag for me. I want to see a strong balance sheet that can weather a storm.

- Cash Flow Statement: Honestly, this might be the most important of the three. It tracks the real cash coming in and going out. A company can look profitable on paper but go bankrupt if it can't manage its cash flow to pay the bills. Cash is king for a reason.

Beyond the raw data, you need to understand the why. What gives this company a lasting edge, what Warren Buffett famously calls a "moat"? It could be a brand people trust implicitly, a patent on a game-changing technology, or a network so large that it's nearly impossible for a competitor to replicate. The quality of the management team is another huge piece of the puzzle. Are they smart, visionary, and acting in the best interests of shareholders?

Your Due Diligence Checklist Isn't Just for Stocks

These core principles of digging deep apply to any asset class, not just stocks. The specific questions you ask will just change depending on what you're analyzing.

For instance, if you're evaluating a rental property, your checklist is going to be completely different. You'll be looking at local vacancy rates, the direction of property taxes, and the physical condition of the building. A new roof and HVAC system can save you from massive headaches and expenses down the line. If you're looking at bonds, your focus shifts to the issuer's credit rating and their fundamental ability to make interest payments on time, every time.

A critical part of any smart investment process is realizing that no asset exists in a vacuum. Its potential is massively influenced by the world around it. Things like geopolitical shifts and overall investor sentiment can be powerful clues about where the smart money is heading next.

Think about how global attitudes are changing capital flows right now. A recent survey revealed a major shift in how institutional investors see the world. Only 36% now see China as a hotbed of opportunity, a massive drop from 47% just a year earlier.

Where is that interest going? It's flowing into other emerging markets in the Asia-Pacific region. You can dig into these evolving investor attitudes yourself on Adams Street Partners.

This kind of big-picture information is invaluable. It adds a crucial layer of context, helping you understand not just the specific investment, but the economic and political currents it's swimming in. When you combine that deep, fundamental analysis with a sharp awareness of these broader trends, you build an investment thesis that is far more robust and defensible.

Valuing an Investment and Finding a Good Price

You've done the high-level analysis and dug deep into the research. Now comes the moment of truth in your investment decision making process: it’s time to crunch the numbers. I can't stress this enough: finding a great company is only half the battle. The other, equally crucial half is buying its stock at a great price.

This is where the art and science of valuation come in. It’s all about figuring out what a business is truly worth, completely separate from its fluctuating price on the stock market. I’ve seen it happen time and time again—overpaying for even the world's best company can lead to years of frustratingly poor returns.

Getting a Handle on Key Valuation Metrics

You don't need a PhD in finance, but you do need to be comfortable with a few core metrics. Think of them as a quick health check on how the market is pricing a company against its actual performance.

A couple of the big ones you'll see everywhere are:

-

Price-to-Earnings (P/E) Ratio: This is the classic. It stacks up a company's stock price against its earnings per share. A high P/E might scream "expensive," while a low one could signal a bargain. But context is everything. A high-flying tech company will almost always have a higher P/E than a slow-and-steady utility company, and that's perfectly normal.

-

Dividend Yield: If you're investing for income, this metric is your best friend. It tells you how much cash the company pays out in dividends each year compared to its stock price. A solid, reliable dividend is often the hallmark of a stable, mature business.

These numbers are just the starting point, though. To really know if you're getting a good deal, you have to go deeper and estimate the company's intrinsic value. This is your best guess at what the business is actually worth, based on all the cash it's expected to generate for the rest of its life.

The real goal here is to find a big gap between the market price and your calculated intrinsic value. Legendary investors call this the "margin of safety." It’s your cushion against being wrong, bad luck, or the economy taking an unexpected nosedive.

Finding the Right Price in Today's Economy

Valuation isn’t done in a vacuum. It’s hugely influenced by the bigger economic picture. Things like interest rates and GDP growth directly affect how much a company can earn in the future, which in turn impacts its intrinsic value.

For instance, look at the current economic forecasts. With global GDP growth projected at 2.9% and 2.8% for the next couple of years, and U.S. growth slowing to 1.6%, the landscape is clearly shifting. This slowdown, fueled by economic uncertainty, changes how we should think about potential returns and risk.

This is where you might roll up your sleeves and use a more advanced (but still manageable) tool like a Discounted Cash Flow (DCF) analysis. A DCF model helps you estimate a company's future cash flows and then "discounts" them back to what they're worth today to arrive at an intrinsic value.

Getting good at these techniques is a massive step up for any serious investor. We actually take a much deeper look into the most popular stock valuation methods in our detailed guide. By combining your solid research with a disciplined approach to valuation, you can move forward with real confidence, knowing not just what to buy, but also when to pull the trigger.

You’ve done the hard work, picked a winner, and now you’re ready to see your investment grow. But hitting the “buy” button isn’t the finish line. Not even close. The real work—the part that separates a lucky one-off from a lifetime of successful investing—is the ongoing management and review of your portfolio. Your investment decision making process hasn't ended; it's just entered its most critical phase. This is the marathon, not the sprint.

The first step is actually executing your trade effectively. You have a few options here, and knowing which tool to use is key. A market order buys or sells immediately at whatever the current price is. It’s fast, but you have zero control over the price you get. I almost always use a limit order, which lets you name your price—the maximum you’ll pay or the minimum you’ll accept. It gives you control, which is something you rarely want to give up in the market.

And don't forget about protective orders. A stop-loss order, for instance, automatically sells your stock if it drops to a predetermined price. This is a lifesaver for managing downside risk, especially with more volatile stocks where you want to cap your potential losses without being glued to your screen all day.

The Power of a Disciplined Review Schedule

Once you own a stock, the temptation is to either check it compulsively every five minutes or completely forget you own it. Both are recipes for disaster. The sweet spot is a consistent, disciplined review schedule. For most of us with a long-term mindset, a quarterly or semi-annual check-in is just about right.

This isn’t about panic-selling because of a scary headline. It’s a structured time to look at two crucial things:

- Are you on track? How is your portfolio performing against the financial goals you set way back in the beginning? Are you on pace, or do you need to make some adjustments?

- Is the story the same? Is the original reason you bought each investment still true? Has something fundamentally changed with the company, its industry, or the economy that breaks your original thesis?

Having a set schedule for this takes the emotion out of it and keeps you from making impulsive moves.

Investing is a process of continuous learning and adaptation. A disciplined review isn't about finding reasons to sell; it's about confirming your reasons to continue holding. It replaces anxiety with a structured, repeatable process.

Rebalancing to Stay on Course

Over time, your portfolio is going to drift. That’s just a fact. If stocks have a killer year, that part of your portfolio might swell from 60% to 70% of your total holdings. Suddenly, you’re way more exposed to a stock market downturn than you originally intended. This is where rebalancing comes in.

Rebalancing is the simple act of selling some of the assets that have done well and using the proceeds to buy more of the ones that have lagged. It brings your portfolio back to its original target mix. It feels completely counterintuitive, but it's an incredibly powerful strategy.

It forces you to systematically sell high and buy low, which imposes a discipline that most investors lack. This one methodical move helps manage your risk and, more often than not, actually improves your long-term returns by keeping you aligned with your own goals.

Got A Few Lingering Questions?

Even with the best-laid plans, it’s completely normal to have some questions pop up. I’ve been doing this for years, and I still double-check my assumptions. The world of investing is nuanced, and asking questions is what smart, thoughtful investors do. Getting these things straight in your head builds the confidence you need to pull the trigger and stick with your strategy.

Let’s run through some of the most common questions I hear. Nailing down the answers to these will help you move forward without that nagging second-guessing that can completely derail a solid plan.

How Much Money Do I Really Need to Start?

This is probably the single biggest myth that keeps people on the sidelines. The honest-to-goodness answer is you can start with whatever you’ve got. Seriously.

Thanks to the explosion of fractional shares and zero-commission trading apps, you can get in the game with as little as $5 or $10.

The secret isn’t how much you start with; it’s the consistency of your investing. The habit of regularly putting money to work—even tiny amounts—is way more powerful over the long haul than waiting around to save up a huge chunk of cash. The real goal is to get started now and let time and compounding do the heavy lifting for you.

Should I Bother Trying to Time the Market?

Let me save you a ton of stress. In a word: no.

Trying to perfectly time the market—catching the absolute bottom and selling at the very peak—is a fool's errand. Even the pros on Wall Street fail at it consistently. A much better approach, and one that will let you sleep at night, is focusing on "time in the market, not timing the market."

Research has shown time and again that the vast majority of an investment's returns come from just being invested. Missing just a handful of the market's best days can absolutely wreck your long-term results.

Instead of gambling on short-term price swings, focus on a strategy that can withstand the ups and downs. A great way to build this mindset is by understanding the principles of building wealth over years, not days. If that sounds like your speed, our guide on what is long-term investing is a fantastic place to start.

How Do I Know When It's Time to Sell?

This is often way harder than figuring out when to buy. There isn’t one magic answer, but you can—and should—create clear rules for yourself before you ever need them.

Here are a few solid, non-emotional reasons to consider selling an investment:

- Your original thesis is broken. The fundamental reason you bought the stock or fund is no longer true. Maybe a competitor launched a killer product, or the brilliant CEO you bet on just left.

- You need to rebalance. The position has grown so much that it's completely thrown your portfolio out of whack, leaving you way too exposed to a single company or sector.

- You’ve found a much better opportunity. You've done the homework and identified a new investment with a significantly better risk-reward profile, and you need to free up the cash to make the move.

Notice what’s not on that list? Panicking because the stock dropped a few percentage points or because of some scary headline on the news. Your selling decisions should be tied to your strategy, not to the market's daily mood swings.

Frequently Asked Questions on Investment Decisions

To wrap things up, let's hit a few more common questions in a quick Q&A format. My goal is to give you clear, direct answers so you can build a strong foundation for making your own investment choices.

| Question | Answer |

|---|---|

| What's the difference between investing and trading? | Investing is typically long-term, focusing on a company's fundamental value with the goal of wealth appreciation over years. Trading is short-term, focused on profiting from price fluctuations over days, weeks, or months. |

| How often should I check my portfolio? | For long-term investors, checking once a quarter is plenty. Checking daily or weekly often leads to emotional decisions based on market noise rather than your strategy. Set it and try to forget it. |

| Is it better to invest a lump sum or use dollar-cost averaging? | Dollar-cost averaging (investing a fixed amount regularly) is often better. It reduces the risk of investing a large sum right before a market downturn and builds a disciplined habit. |

| How many stocks should I own? | For most people, owning 15-30 individual stocks provides good diversification without becoming unmanageable. If that's too much, a few low-cost index funds or ETFs can achieve the same goal much more easily. |

Hopefully, these answers clear up some of the fog. The more you learn, the less intimidating this all becomes.

At Investogy, we believe that demystifying these common questions is key to building real conviction. We don't just share what we're buying; we share the why behind every part of our process. Subscribe to our free weekly newsletter to follow our real-money portfolio and learn how we navigate these decisions firsthand at https://investogy.com.

Leave a Reply