Deciding between picking individual stocks or just buying index funds is one of the first major crossroads every investor faces.The difference is pretty straightforward: stock picking is an active game where you try to beat the market, while investing in index funds is a passive strategy where you aim to simply match the market's performance. The right choice for you boils down to whether you want to be a hands-on analyst trying to unearth hidden gems, or if you prefer a “set-it-and-forget-it” approach that rides the market as a whole.

Understanding Your Core Investment Choices

The stock picking vs. index funds debate isn't just about what you buy; it’s about two completely different investment philosophies. One path has you playing detective, sifting through company reports and market data for undervalued treasures. The other path makes you a passenger, trusting that the entire market will move in the right direction over time.

The Active Path of Stock Picking

Stock picking is exactly what it sounds like—you analyze individual companies to decide if their stock is a smart buy. This is an active, often time-consuming, process that requires a ton of research. You're essentially betting that you can spot opportunities that other investors have overlooked.

If you go down this road, you have to be ready to commit to:

- Deep Research: This means digging into financial statements, understanding industry trends, and figuring out a company's competitive edge.

- Constant Monitoring: You can't just buy and walk away. You need to keep up with company news, quarterly earnings reports, and broader economic shifts.

- Emotional Discipline: This is a big one. You have to fight the urge to panic-sell during a downturn or chase the latest hot stock without doing your homework.

The whole point is to build a portfolio of stocks that, together, will deliver better returns than the overall market average. If you're curious about the nuts and bolts, our guide on how to build a stock portfolio breaks it down step-by-step.

The Passive Path of Index Funds

The philosophy behind index funds is simple: consistently beating the market is incredibly difficult, even for the pros. So, instead of trying to find the needle in the haystack, you just buy the whole haystack. An index fund, like one that tracks the S&P 500, simply owns all the stocks in that particular market index.

This approach comes with some major perks:

- Instant Diversification: By buying one fund, you own a tiny slice of hundreds or even thousands of companies. This spreads out your risk immediately.

- Low Effort: Once you've made your investment, the hard part is over. There's no ongoing need to research individual companies or make frequent trading decisions.

- Predictable Returns: Your performance will very closely track the underlying market index, minus a tiny management fee.

An index fund basically guarantees you'll capture the market's return. You're removing the risk of underperforming because you picked the wrong stocks. It's really a bet on the long-term growth of the entire economy.

To make things even clearer, let's break down the key differences in a simple table.

Stock Picking vs Index Funds at a Glance

This table sums up the fundamental differences between the two approaches, giving you a quick snapshot of what each path entails.

| Attribute | Stock Picking (Active) | Index Funds (Passive) |

|---|---|---|

| Primary Goal | Outperform the market average | Match the market average |

| Time Commitment | High (ongoing research required) | Low (set and forget) |

| Required Skill | High (financial analysis, market knowledge) | Low (basic investment principles) |

| Diversification | Low to moderate (depends on portfolio size) | High (built-in and immediate) |

| Typical Costs | Higher (trading fees, research tools) | Very Low (minimal expense ratios) |

As you can see, these two strategies are built for very different types of investors with different goals, time commitments, and risk tolerances.

Contrasting Core Investment Philosophies

When you get down to it, the "stock picking vs. index funds" debate is really a clash between two completely different views on how the market actually works. Your decision isn't just about what to buy; it's about picking a side and aligning with a core belief that will guide your entire investment strategy. Each path demands a totally different mindset and set of expectations.

The philosophy of stock picking is all about active pursuit and deep conviction. It’s rooted in the belief that the market isn't perfectly efficient. Stock pickers are hunters, operating on the assumption that with enough research, skill, or a unique insight, they can spot pricing mistakes and find those hidden gems—undervalued companies ready to take off.

This isn't a passive activity. It requires an analytical, often contrarian, mindset. You have to be willing to roll up your sleeves and dig deep into company financials, size up the management team, and truly understand the competitive battlefield. You’re looking for something the rest of the market has missed.

The Mindset of the Stock Picker

The active investor is confident they can get an edge. They use specific tools and playbooks to find these opportunities, often falling into distinct camps. For example, knowing the difference between growth vs value investing is fundamental to understanding the different ways pickers approach the market.

- Fundamental Analysis: This is the classic detective work. You’re poring over a company's balance sheets, income statements, and cash flow to figure out its true, or intrinsic, value. The whole point is to buy stocks for less than they’re actually worth.

- Technical Analysis: This approach is more about market psychology. It involves studying chart patterns and trading volumes to predict where a stock's price might go next, believing that history often rhymes.

"Investors vote with their dollars. They’ll buy or sell a stock if they perceive it as under- or over-valued. On average, over time, yes, we expect a stock’s price to be correlated to the company’s value. But there are periods when a stock price is disjointed from its value."

This core belief in market inefficiency is what drives the whole thing. The stock picker is betting they can exploit those temporary gaps between a stock's price and its real value, aiming to beat the market averages.

The Philosophy of the Index Fund Investor

On the other side of the aisle, the philosophy behind index funds is one of acceptance and humility. It’s tied directly to the Efficient Market Hypothesis (EMH), which basically says that stock prices already reflect all the known information out there. If that's true, then trying to consistently find a bargain is a fool's errand.

This belief leads to a simple but powerful conclusion: if you can't beat the market, just own the market. Index fund investors don't waste time trying to outsmart the collective wisdom of millions. They just aim to capture the market's overall return by buying a slice of everything, like all the companies in the S&P 500. For anyone wanting to delve deeper into passive versus active investment strategies, understanding this core principle is the place to start.

This passive approach is built on a few key pillars:

- Broad Diversification: By owning the whole haystack, you don't have to worry about one needle breaking. It minimizes the risk of a single company's collapse wrecking your portfolio.

- Low Costs: No expensive analysts, no frequent trading. This keeps fees incredibly low, which means more of your money stays invested and working for you.

- Simplicity: The strategy is dead simple. You buy, you hold, and you let the market do its thing. It doesn't require constant attention or deep expertise.

The fundamental bet here is that long-term economic growth will lift the market as a whole. The most reliable way to build wealth, then, is to simply ride that wave at the lowest possible cost. It’s a pragmatic acceptance that trying to beat the market is a game very few people win over the long haul.

Comparing Historical Performance and Real Returns

When you're weighing stock picking against index funds, theories are nice, but the real story is in the numbers. Decades of performance data tell a clear and consistent tale: the average active stock picker just doesn't keep up with a simple market index. Over the long haul, the evidence stacks up heavily in favor of the passive approach.

The problem for stock pickers isn't just about finding a winning company. It's about finding enough winners to jump two hurdles: the higher fees that come with active trading and the relentless, broad growth of the market itself. We all love the stories of legendary investors who hit it big on a single stock, but those are the exceptions—statistical outliers, not the reality for most people.

The Statistical Hurdle of Beating the Market

Long-term studies drive this point home again and again. The S&P Dow Jones Indices runs a regular report card (the SPIVA scorecard) that pits fund managers against their benchmarks, and the results are pretty brutal for the active crowd.

Over the last 15 years through 2023, a jaw-dropping 88% of large-cap active funds failed to beat the S&P 500. Let that sink in. And it's not just large-cap stocks. Across every single equity category, not one saw a majority of its active managers outperform their index over that 15-year period. You can find plenty of great market analyses and discussions that dive deeper into this active vs. passive debate.

This isn't a fluke. Year after year, the data shows that while a handful of managers might get lucky and beat the market in a given year, almost none can do it consistently over five, ten, or fifteen years.

The big takeaway from decades of market history is this: your odds of outperforming a low-cost index fund get smaller and smaller the longer you invest. Short-term luck eventually runs out, but the market's average return and the drag of high fees are forever.

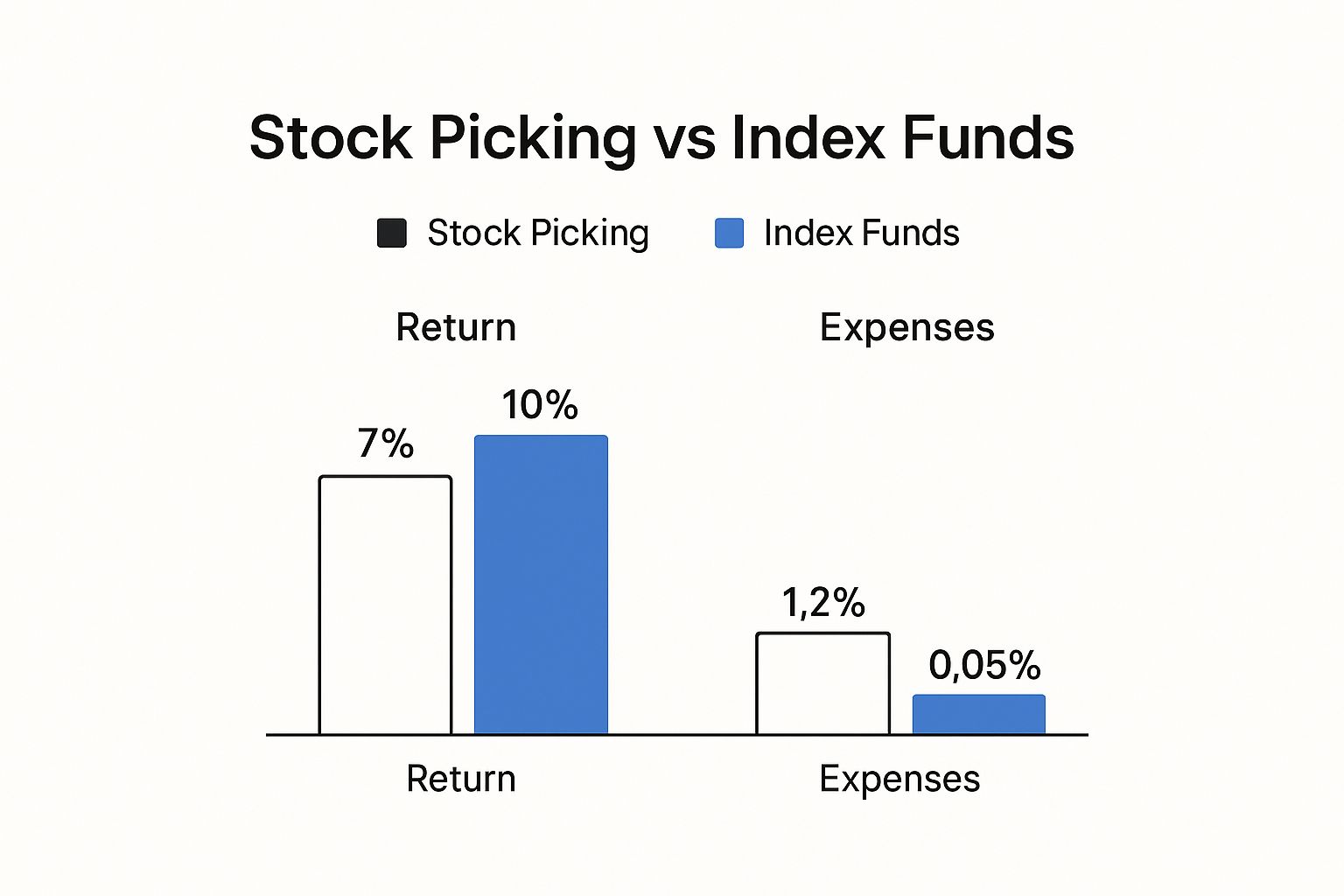

The infographic below really paints a picture of the difference in both average returns and the expenses you'll typically pay for each strategy.

As you can see, higher fees act like a direct anchor on the potential returns of an active strategy. Meanwhile, index funds get to enjoy market-level returns without that costly baggage.

The Hidden Trap of Survivorship Bias

There's another huge factor that makes stock picking look more successful than it really is: survivorship bias. This is a classic statistical illusion where the performance data we see only includes the "survivors"—the funds or stocks that are still around.

The losers? They get quietly swept under the rug. Failed funds and delisted companies are removed from the performance charts, which makes the average returns of the remaining group look a whole lot better than they should.

Think about it like this: say you start with 100 active funds. Over ten years, 30 of them perform so terribly that they shut down. When you go to analyze performance, you're only looking at the 70 that made it. The final numbers are skewed, painting an overly rosy picture of success.

This bias creates a really misleading story. It hides the true failure rate of active management and makes picking winners seem much easier than it actually is. When you factor in all the funds that started the race—not just the ones that crossed the finish line—the case for index funds becomes even more powerful. Any potential return from an active strategy has to be weighed against this very real risk of failure, a risk that passive indexing all but eliminates.

Analyzing Risk Management and Diversification

How you handle risk is every bit as important as the returns you chase. When it comes to stock picking versus index funds, the approaches to managing risk couldn't be more different. One is a game of concentrated bets, the other is all about broad market exposure. Each path comes with a completely unique risk profile that will shape your potential for big wins and painful losses.

The biggest beast you have to slay with stock picking is concentration risk. When you hand-pick individual stocks, you're tying a huge chunk of your financial future to the fate of just a few companies. If you pick a winner, the rewards can be incredible. But if just one of your core holdings gets knocked down, your entire portfolio can take a nasty hit.

The Dangers of Company-Specific Risk

History is littered with the corpses of industry giants that looked unstoppable right before they collapsed, driving home just how volatile betting on single companies can be. Think about BlackBerry, once the king of the smartphone world, or General Electric, a former blue-chip icon. Both saw their stock prices crater due to new technology and disastrous management decisions. An investor who went all-in on either of those would have watched their wealth vaporize.

This gets to the heart of the stock picking challenge: you’re not just battling broad market downturns, you’re also exposed to company-specific risk. This is all the stuff that can go wrong with just one business, like:

- A string of bad calls from the executive suite

- A major product launch that flops

- A new competitor that comes out of nowhere

- Sudden regulatory or legal nightmares

These things are brutally hard to predict, making even the most deeply researched stock pick a high-stakes gamble. The odds are stacked against you, too. Research from JP Morgan found that, on average, nearly 30% of S&P 500 stocks deliver negative returns of 5% or more each year. That really shows you how easy it is to pick a loser, even from a pool of supposedly elite companies.

The Built-In Safety Net of Index Funds

Index funds come at risk from the complete opposite direction. Instead of trying to find that one golden needle of a winning stock, an index fund just buys the entire haystack. This strategy gives you instant, powerful diversification—one of the most tried-and-true tools for managing risk.

By owning a tiny piece of hundreds, or even thousands, of companies, you dramatically shrink the impact any single company's failure can have on your money. If one stock in the S&P 500 goes bankrupt, its effect on the total index—and your investment—is practically a rounding error.

This built-in diversification is your shield against company-specific risk. Your investment’s success is no longer riding on a few CEOs or a handful of products, but on the collective growth of an entire market or the economy as a whole. You’re essentially trading the lottery-ticket potential of a massive single-stock gain for a much smoother, more predictable ride.

For anyone looking to beef up their portfolio's defenses, our guide on how to diversify an investment portfolio is a great place to start. This passive approach hitches your long-term success to the broad, persistent trends of the market, not the wild and unpredictable fortunes of individual businesses.

The True Impact of Costs, Fees, and Taxes

Beyond the flashy performance charts, there's a quiet killer of investment returns: costs and taxes. It's not the most exciting topic, I get it. But ignoring it is like trying to fill a bucket with a hole in it. These small, consistent leaks can drain a massive portion of your long-term growth, acting as a constant headwind on your portfolio.

The difference between stock picking and index funds here isn't just a minor detail; it's a massive gap that directly hits your final account balance.

When you're actively picking stocks, you're constantly doing something. And in the world of investing, every action has a cost.

- Trading Commissions: Every time you hit that buy or sell button, there's friction. Even with "zero-commission" trades, frequent activity can lead to other fees or less-than-ideal execution prices. It all adds up.

- Advisory Fees: If you've hired someone to manage your stock portfolio, their fee is a direct drag on your results. A typical fee of around 1% of your assets annually might sound small, but that's 1% you have to beat every single year just to break even with the market.

- Fund Expense Ratios: For investors who choose actively managed mutual funds, the expense ratios are in a different universe compared to passive funds. We're often talking 0.50% to over 1.5% annually. That fee pays for the research analysts and portfolio managers making those active bets.

This financial drag is a huge reason why beating the market is so incredibly tough over the long haul. A mountain of evidence shows that most active stock pickers fail to keep up with simple index funds. In fact, various studies have found that somewhere between 92% and 95% of actively managed funds fell short of their benchmarks over a 15-year period. High fees and tax inefficiency are the primary culprits. You can dig into more data on why picking stocks often falls short for the vast majority of people.

Comparing Cost and Tax Efficiency

Let's lay it out side-by-side. The contrast in the financial drag between these two approaches becomes crystal clear when you see the numbers.

| Factor | Stock Picking (Active) | Index Funds (Passive) |

|---|---|---|

| Expense Ratio | Higher (often 0.50% – 1.5%+) | Extremely Low (often 0.03% – 0.10%) |

| Trading Costs | Higher due to frequent buying/selling | Minimal due to low portfolio turnover |

| Tax Efficiency | Lower; frequent trading triggers capital gains | Higher; buy-and-hold strategy defers taxes |

| Advisory Fees | Common if using a professional manager | Typically none for self-directed investors |

The table really tells the story. On every single cost metric, the active approach starts with a significant handicap that it must overcome year after year.

The Power of Tax Efficiency

The cost battle extends deep into the world of taxes, where index funds have a massive structural advantage.

By definition, active stock pickers are buying and selling to try and time the market. Every time they sell a stock for a profit after holding it for less than a year, it triggers a short-term capital gains tax. This isn't some small fee; it's taxed at your ordinary income tax rate, which is the highest rate you pay.

Index funds, on the other hand, are the champions of tax efficiency. Their entire game plan is to simply buy and hold all the stocks in an index. This results in incredibly low portfolio turnover, meaning they almost never sell their holdings unless the index itself changes.

The low-turnover nature of index funds means you are rarely hit with unexpected capital gains distributions. This allows your investment to compound more effectively over time, as more of your money remains invested in the market rather than being siphoned off to pay taxes.

This tax deferral is a powerful, built-in benefit. By kicking the tax can down the road, index funds let your wealth grow unimpeded for years, sometimes decades. When you combine this structural tax advantage with their rock-bottom fees, you get a powerful tailwind that active strategies are constantly fighting against.

So, Which Strategy Is Right for You?

Look, choosing between picking individual stocks and buying index funds isn't about finding some magical "correct" answer that works for everyone. The right path is deeply personal. It comes down to your goals, how much time you can realistically put in, and frankly, your stomach for risk.

Let's cut to the chase: for the vast majority of people trying to build wealth over the long haul, the evidence points overwhelmingly toward index funds. If your goal is steady, reliable growth without turning investing into a second job, this is almost certainly your best bet.

The Case for Making Index Funds Your Core Strategy

Index funds are built for the investor who values their time, appreciates simplicity, and understands the power of diversification. This is the right fit for you if this sounds familiar:

- You're in it for the long game. You're investing for decades, not days. Your focus is on capturing the market's overall growth, not trying to time the next hot stock.

- You've got a life to live. You'd rather spend your free time doing literally anything else besides poring over financial statements and watching market news like a hawk.

- You prefer to sleep at night. The thought of your financial future riding on the quarterly earnings report of a handful of companies sounds more stressful than exciting.

- You're smart about costs. You get that low fees and tax efficiency are huge, often overlooked, drivers of your total returns over time.

For most people, the winning formula is simple: accept the market's return through a diversified, low-cost index fund, build your financial plan around that, and then get on with your life. It’s an incredibly powerful, drama-free path to success.

When Does Picking Stocks Actually Make Sense?

While index funds are the smart default, there is a certain type of person for whom picking individual stocks might be a reasonable consideration—usually for a small, speculative part of their overall portfolio. This path is really only for those who have a rare mix of skill, time, and temperament.

This approach might be for you if:

- You genuinely love business analysis. You enjoy the process of digging into a company's fundamentals, competitive landscape, and management team. You have the financial chops to do it right.

- You can commit serious time. This isn't a casual hobby. It demands consistent, dedicated hours for research and ongoing monitoring.

- You have a high tolerance for getting punched in the gut. You can handle the reality of watching an individual stock drop 50% or more without panicking and selling at the worst possible time.

Even for this type of investor, the data is clear: trying to consistently beat the market is an incredibly difficult game. The odds are stacked against even the most brilliant and dedicated individuals.

The Hybrid Play: The Core-Satellite Model

For many, the most pragmatic solution is the core-satellite model. It's a hybrid approach that lets you have your cake and eat it too, combining the reliability of passive indexing with the potential excitement of active stock picking.

Here’s the breakdown:

- The Core: The vast majority of your portfolio—think 80-95%—is invested in a diversified basket of low-cost index funds. This is the stable, reliable foundation of your wealth-building engine.

- The Satellites: A small, clearly defined portion—say, 5-20%—is allocated to individual stocks or other active investments you've researched to death.

This model lets you scratch that itch to find the "next big thing" without betting the farm. Your core index funds do the heavy lifting for your long-term goals like retirement, while the satellite portion is your designated space for high-conviction ideas. It’s a disciplined framework that gives you the best of both worlds.

Common Questions Answered

When you're weighing stock picking against index funds, a lot of practical "what if" scenarios pop up. Let's tackle some of the most common questions head-on to help you figure out where you land.

Can I Do Both Stock Picking and Index Funds?

Yes, you absolutely can. In fact, blending the two is a popular and pretty smart strategy.

It's often called the core-satellite model. Think of it this way: the "core" of your portfolio, maybe 80-95% of it, is built on solid, low-cost index funds. This is your foundation for steady, long-term growth—the part you don't want to mess with.

The "satellite" portion is the other 5-20%. This is your playground for picking individual stocks. It lets you chase those high-conviction ideas you believe in, aiming for bigger returns without putting your main financial goals on the line. It’s a great way to scratch the stock-picking itch while keeping the reliable engine of passive investing running.

Is Stock Picking a Better Move for Younger Investors?

There's a common argument that because younger investors have decades ahead of them, they can afford to take on the higher risks of stock picking. They have time to recover from any big losses, right?

While it's true that a long time horizon is a huge advantage, it doesn’t magically make stock picking the superior choice. The hard numbers still show that most active investors fail to beat the market over the long run, and that applies whether you're 25 or 55.

A better way to look at it is this: a young investor can use a small, non-essential slice of their portfolio to learn the ropes of stock analysis. Think of it as educational money. The key is making sure the vast majority of their savings—the serious retirement money—is parked in diversified, low-cost index funds to let compounding do its heavy lifting without taking wild swings.

The efficient market hypothesis is probably wrong. Or at least, it has clear flaws. But 99% of people should act as if it’s perfectly right.

This quote really nails it. Even if you believe you can find an edge in the market, the odds are so stacked against you that for most people, simply matching the market with an index fund is the winning move.

What if I Find a Stock Picker with an Incredible Track Record?

It's incredibly tempting. You see a fund manager who has absolutely crushed the market for years and think, "This is the one." But be careful—past performance is a notoriously poor predictor of future results.

Research has shown time and again that the few managers who outperform the market for a stretch rarely keep it up. A hot streak is often just that—a streak, driven by a mix of luck and survivorship bias (you never hear about the funds that blew up and disappeared).

When you bet on a star manager, you're not just betting they'll keep winning; you're betting they'll win by enough to overcome their high fees. That's a huge hurdle to clear, year after year, when a simple index fund is right there, chugging along with the market at a fraction of the cost.

How Many Stocks Do I Actually Need for Diversification?

If you decide to build your own portfolio from individual stocks, getting diversification right is a big deal and a lot harder than it looks.

There isn't a single magic number, but most financial pros suggest you need a bare minimum of 20-30 stocks. And not just any stocks—they need to be spread across different industries and sectors. If you hold fewer, you're exposed to massive company-specific risk. A bad earnings report or a scandal at just one or two companies could wreck your entire portfolio.

But let's be real: even with 30 well-chosen stocks, you're nowhere near as diversified as a broad market index fund. An S&P 500 index fund, for example, gives you a piece of 500 different companies instantly. That's why index funds offer such robust risk management right out of the box, without all the capital and ongoing research required to build and maintain a stock portfolio yourself.

Ready to see these ideas in action? The Investogy newsletter is a transparent, real-money portfolio where we share the "why" behind every investment. Subscribe for free and learn alongside us.

Leave a Reply