Portfolio rebalancing is just a fancy term for getting your investments back in line with your original game plan. Think of it as a disciplined tune-up for your portfolio: you systematically sell some of the assets that have done really well and use that money to buy more of the assets that have lagged behind. The goal is to bring your portfolio back to its target risk level.

Your Investing GPS: Understanding Portfolio Rebalancing

Imagine setting out on a long road trip. Before you leave, you plug your destination into your GPS. That route is your investment plan, designed to get you to your financial goals safely and on time. Rebalancing is the GPS constantly recalculating and making small course corrections to keep you on the fastest, most efficient path, especially when unexpected detours or traffic jams (market volatility) pop up.

Left untouched, your portfolio will naturally drift away from its starting point. It’s inevitable. Some investments will have a great year and grow faster than others, making them a bigger piece of your overall pie. For instance, a strong run in the stock market could easily turn your balanced 60% stocks/40% bonds portfolio into a much riskier 70/30 mix—without you ever making a single trade.

The Car Alignment Analogy

This is a lot like your car's wheel alignment. When the wheels are out of alignment, the car still drives, but it might pull to one side. You might not even notice it on a smooth, straight road. But that subtle pull makes the car less efficient, wears down your tires unevenly, and can make it much harder to control in bad weather.

An unbalanced portfolio is the same way. It might feel great during a bull market when everything is going up, but that unintended concentration in certain assets leaves you far more exposed when the market takes a downturn. Rebalancing is the routine maintenance that pulls everything back into spec, ensuring a smoother, safer financial journey.

To illustrate how this works, let's look at a simple portfolio before and after a year of market movements.

Your Portfolio Before and After Rebalancing

This table shows how a simple portfolio can drift from its intended path and how rebalancing brings it back into alignment.

| Asset Class | Initial Target | After Market Shift | After Rebalancing |

|---|---|---|---|

| Stocks | 60% | 70% | 60% |

| Bonds | 40% | 30% | 40% |

As you can see, the stock portion grew to 70% due to strong performance, increasing the portfolio's overall risk. Rebalancing involves selling 10% of the stocks and buying 10% more bonds to restore the original 60/40 split.

This process isn't about chasing the highest possible returns. It’s about sticking to your strategy and managing risk.

At its core, portfolio rebalancing is a risk-control tool. The idea isn't to time the market but to maintain your intended investment strategy and protect yourself from taking on more risk than you're comfortable with as the market moves.

This systematic approach forces you to buy low and sell high, putting discipline ahead of emotion. If you're looking to build on foundational concepts like this, resources like Vtrader's Academy offer a great way to deepen your knowledge. Ultimately, rebalancing keeps you in the driver's seat of your financial future.

Why Rebalancing Is Your Financial Safety Net

A lot of investors think rebalancing is about trying to squeeze a few extra percentage points out of the market. It’s not. In reality, its main job is far more important: it’s one of the best risk-management tools you’ll ever use.

Think of it less like chasing hot stocks and more like protecting the gains you’ve already worked so hard to make.

The real magic of rebalancing is that it yanks emotion right out of the equation. It's a system that forces you to follow the oldest, most proven rule in investing: buy low and sell high. When one of your investments shoots for the moon, rebalancing tells you to sell a bit and lock in those profits. When another one takes a dive, it nudges you to buy more while it's on sale.

Protecting Against Overconcentration

Imagine your portfolio is a garden. If you let one plant—say, a fast-growing tomato vine—go wild, it’ll eventually hog all the sunlight, water, and nutrients. Pretty soon, your other plants will start to wither. A smart gardener regularly prunes that overgrown vine, not to punish it, but to keep the whole garden healthy and balanced.

That’s exactly what rebalancing does for your investments. Without it, a single high-flying stock or a hot sector can quietly grow to dominate your portfolio. Before you know it, you're dangerously over-exposed to one volatile area. Rebalancing "prunes" those winners to restore balance and keep your entire portfolio thriving for the long haul.

This isn't just a trick for DIY investors, either. Professional fund managers are constantly doing this to keep their portfolios in line with their risk targets. One study of 6,500 international equity funds found that managers consistently tweaked their holdings to stabilize their exposure as the market moved.

Rebalancing is basically a cheat code for disciplined investing. It makes you a contrarian by default, forcing you to take profits from your winners and move that cash into assets that are temporarily unloved. This simple act prevents you from making emotional mistakes that could derail your whole strategy.

Aligning With Your Long-Term Goals

At the end of the day, the whole point is to keep your portfolio true to your personal financial plan. You picked your specific mix of stocks and bonds for a reason—it was based on your timeline, your goals, and how much risk you could stomach.

If you haven't nailed down those targets yet, our guide on recommended asset allocation based on age is a great place to start. Once you have that blueprint, rebalancing is simply the maintenance that ensures you stay on that carefully chosen path, no matter what kind of chaos the market throws at you.

Common Portfolio Rebalancing Methods Explained

Once you’re sold on the "why" of rebalancing, the next question is "how." Luckily, you don't need a Wall Street algorithm to get this right. Most investors stick to one of two straightforward, battle-tested methods to keep their portfolios on track.

Think of it as two main camps: rebalancing on a fixed schedule, or rebalancing only when things get noticeably out of whack. Each has its own rhythm and fits a different type of investor.

Calendar-Based Rebalancing

The simplest and most popular method is calendar-based rebalancing. Just like it sounds, you pick a date on the calendar and make that your rebalancing day. It could be annually (maybe on your birthday), semi-annually, or quarterly.

The biggest win here is discipline. It creates a recurring, non-negotiable appointment to check in on your portfolio. This forces you to step back from the daily market noise and focus on your long-term plan, preventing emotional, knee-jerk reactions.

This "set it and forget it" style is a perfect fit for hands-off investors who prefer a simple routine they can stick to without much fuss.

By committing to a schedule—say, every January 1st—you automate your discipline. This removes the temptation to react to short-term market noise and keeps your focus squarely on your long-term strategy.

Threshold-Based Rebalancing

On the other hand, threshold-based rebalancing is all about reacting to specific events, not the calendar. Here, your trigger is when an asset class strays too far from its target allocation by a percentage you decide on ahead of time.

For example, you could set a 5% threshold. If your target for stocks is 60% of your portfolio, you'd only step in to rebalance when that allocation hits 65% (time to sell some) or drops to 55% (time to buy more).

This approach is naturally more tuned-in to market swings. It ensures you only make a move when your portfolio's risk level has genuinely shifted, which can lead to smarter adjustments during big market rallies or downturns.

Choosing Your Rebalancing Strategy

So, which path is right for you? It really boils down to your personality and how you like to manage things. Are you a routine-oriented person who thrives on a simple, predictable schedule? Or do you prefer a more dynamic approach that calls for a bit more monitoring but responds directly to market changes?

To help you decide, here’s a quick comparison of the two main strategies.

| Strategy | Best For | Pros | Cons |

|---|---|---|---|

| Calendar-Based | Hands-off investors who value simplicity and routine. | Easy to remember and automate. Enforces discipline and prevents emotional decisions. | Can be arbitrary; you might trade unnecessarily or miss major market moves between dates. |

| Threshold-Based | Hands-on investors who want to react to market volatility. | More responsive to market shifts. Avoids trading on minor fluctuations. | Requires more frequent monitoring to spot when a threshold is crossed. |

Ultimately, there’s no single "best" answer. The most effective rebalancing plan is the one you can actually follow consistently over the long haul. Figure out which style clicks with you, and you'll be well on your way to building a resilient, goal-oriented portfolio.

How Global Events Impact Your Rebalancing Strategy

It’s easy to forget, but your portfolio doesn't live in a vacuum. It's constantly being pushed and pulled by what's happening around the world—everything from currency swings to how international markets are trending. These global currents can seriously throw your asset allocation off course, which is why a disciplined rebalancing strategy is so critical.

Professional fund managers get this. For them, rebalancing isn't just about managing risk; it's their systematic way of responding to global shifts. It also acts as a powerful antidote to a classic investor mistake known as home bias. That’s our natural tendency to keep most of our money invested right here in our own country's market.

Overcoming Home Bias With Discipline

Sticking to what's familiar feels safe, but piling too much into domestic stocks leaves your portfolio exposed. A good rebalancing plan forces you to stay globally diversified.

Let’s say your international stocks have a fantastic year. Their value balloons, and suddenly they’re a much bigger piece of your portfolio pie than you intended. Rebalancing is the trigger that tells you to trim some of those high-flying foreign assets and lock in those gains, bringing the profits back home.

Now, flip the script. What happens when international markets take a dive? Your allocation to them shrinks. This is where rebalancing shines. It nudges you to buy more of these assets while they're on sale, hardwiring the "buy low" principle into your strategy on a global scale. This disciplined process keeps you from ditching your international holdings right when it's the most opportune time to be buying.

A study of over 8,500 funds found a clear pattern: when foreign stocks did well, managers systematically moved capital back to their home turf. But when foreign stocks fell, they consistently bought more, with currency volatility making this effect even stronger. You can dive into the research on global rebalancing strategies.

By sticking to your target allocations, you’re not just reacting to market news. You're building a framework that can actually take advantage of global market cycles instead of getting swept away by them.

Your Step-by-Step Guide to Rebalancing a Portfolio

Knowing the theory is one thing, but putting portfolio rebalancing into practice is where you really take control. The good news is, this process isn't nearly as complex as it sounds. Think of it as a disciplined tune-up for your investments, designed to keep everything aligned with your long-term vision.

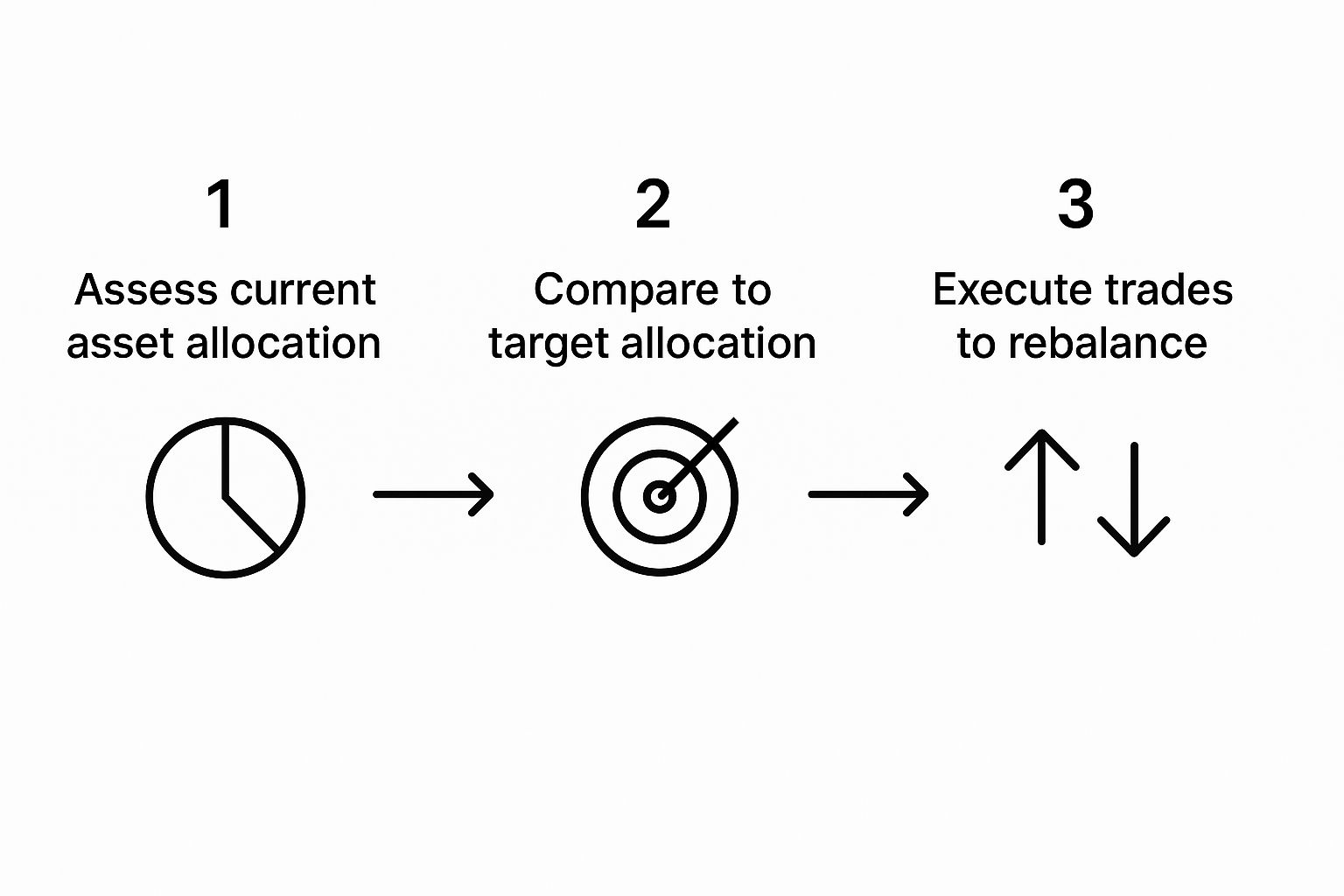

This visual below lays out the core workflow, from taking stock of where you are to making the necessary moves.

It really boils down to three simple stages: see where you stand, compare it to your blueprint, and then make the adjustments to get back on track.

A Practical Four-Step Process

Ready to roll up your sleeves? Here is a clear, actionable blueprint to bring your portfolio back into balance. Once you do it a couple of times, it becomes a simple, repeatable habit.

-

Review Your Target Allocation: Before you touch a single investment, you need to check your map. Is your original target still the right one for you? Life changes, and your strategy should, too. Does that 60% stock and 40% bond split still feel right given your goals and stomach for risk? A solid, up-to-date allocation is the foundation of everything that follows.

-

Assess Your Current Portfolio: Next, it's time for a snapshot of your portfolio right now. Tally up the current value of each of your asset classes—U.S. stocks, international stocks, bonds, etc.—and calculate what percentage each one represents of your total portfolio. This is where you'll see exactly how far the market's ups and downs have pushed you off course.

-

Calculate the Difference: This part is just simple math. With your target percentages and your current percentages in hand, subtract one from the other. This instantly shows you which assets are overweight (they've grown bigger than planned) and which are underweight (they've shrunk or been outpaced). You now have a crystal-clear roadmap for what to sell and what to buy.

-

Execute the Trades: Now for the final step: taking action. Sell just enough of your overweight assets to bring them back down to their target percentage. Then, take that cash and use it to buy more of your underweight assets until they're back up to their target.

A critical piece of the puzzle here is taxes. To sidestep a surprise bill from Uncle Sam, always try to do your rebalancing inside tax-advantaged accounts like a 401(k) or IRA first. Trades inside these accounts don't trigger capital gains taxes.

By doing the heavy lifting in your tax-sheltered accounts, you can often get your entire portfolio back in line without having to sell anything and create a taxable event in your brokerage account. Getting this process right reinforces the core principles of a smart, well-built investment plan. For a deeper dive on setting up that structure, check out our guide on how to diversify an investment portfolio.

Common Rebalancing Mistakes and How to Avoid Them

Even with a rock-solid plan, it's surprisingly easy to shoot yourself in the foot when rebalancing. One of the classic blunders is over-trading—basically, fiddling with your portfolio way too often. It might feel like you're being proactive, but all you're really doing is racking up transaction fees and possibly triggering capital gains taxes that eat into your returns.

Then there's the biggest portfolio-killer of all: letting your emotions call the shots. The whole point of a rebalancing strategy is to take your gut feelings out of the equation. It feels completely wrong to sell a stock that's on a hot streak or buy more of one that's been struggling. But the moment fear or greed starts dictating your moves, you've defeated the purpose of this disciplined approach.

Forgetting About Fees and Taxes

Ignoring the small stuff, like transaction costs, is another huge mistake. Those fees might seem minor, but they add up fast, especially if you have a smaller portfolio and rebalance aggressively. Research actually shows that these costs directly influence how and when fund managers rebalance, especially when there's a big performance gap between different assets. If you're curious about the nitty-gritty, you can check out this paper on how transaction costs impact fund rebalancing.

A successful rebalancing strategy is as much about what you don't do as what you do. Avoiding frequent, emotionally-driven trades and keeping a close eye on tax implications are just as important as the rebalancing itself.

If all this sounds like a headache you'd rather avoid, you're not alone. For investors who prefer a more hands-off approach, automated options like target-date funds or robo-advisors handle all of this for you. They keep your portfolio aligned with your targets automatically, making them a fantastic way to sidestep these common pitfalls.

Getting these details right is a massive part of smart, long-term investing. You can dive deeper into other great habits in our guide to portfolio management best practices.

Your Top Rebalancing Questions, Answered

Even when you've got the basics down, some of the finer points of rebalancing can be tricky. Let's tackle some of the most common questions that pop up.

How Often Should I Rebalance My Portfolio?

There's no single "right" answer here—it really boils down to the method you're most comfortable with.

Many investors love the simplicity of a calendar-based approach, rebalancing on a set schedule like annually or quarterly. It’s simple and keeps you disciplined. Others prefer a threshold-based method, which ignores the calendar completely and only triggers a rebalance when an asset class drifts by a certain amount, say 5% from its target.

Does Rebalancing Actually Increase My Returns?

Not really, and honestly, that’s not the point. Think of rebalancing as a risk-management tool, not a magic bullet for higher returns.

Its real job is to keep your portfolio from getting too top-heavy in one area and drifting away from your long-term goals. While it naturally forces you to "buy low and sell high," its main superpower is keeping your risk level exactly where you want it.

What Are the Tax Implications of Rebalancing?

This is a big one, and you’re smart to ask. When you sell winning investments in a regular taxable brokerage account, you’ll likely trigger capital gains, and Uncle Sam will want his cut.

To be smart about it, always try to rebalance inside your tax-advantaged accounts first, like a 401(k) or an IRA. Trades within these accounts don't create a taxable event, which is a huge advantage.

A slick way to rebalance without selling is to use your new contributions. Instead of trimming your winners, just direct your new investment dollars into the parts of your portfolio that are underweight. This nudges your allocation back into line over time without creating a tax bill.

It's a gentler, more tax-efficient way to get your portfolio back on track.

Ready to stop guessing and start building conviction? The Investogy newsletter offers a transparent look at how a real-money portfolio is managed, sharing deep research and actionable insights every week. See the strategies in action and learn from real results by subscribing for free at https://investogy.com.

Leave a Reply